Turnaround-Story Banner: Muttergesellschaft der Banner Bank und der Islanders Bank - 500 Beiträge pro Seite

eröffnet am 28.07.10 00:22:40 von

neuester Beitrag 07.11.10 14:44:09 von

neuester Beitrag 07.11.10 14:44:09 von

Beiträge: 54

ID: 1.159.023

ID: 1.159.023

Aufrufe heute: 0

Gesamt: 675

Gesamt: 675

Aktive User: 0

Top-Diskussionen

| Titel | letzter Beitrag | Aufrufe |

|---|---|---|

| vor 31 Minuten | 6411 | |

| vor 51 Minuten | 5138 | |

| vor 36 Minuten | 4245 | |

| vor 1 Stunde | 3877 | |

| vor 44 Minuten | 2714 | |

| vor 42 Minuten | 1986 | |

| heute 14:53 | 1961 | |

| heute 13:07 | 1512 |

Meistdiskutierte Wertpapiere

| Platz | vorher | Wertpapier | Kurs | Perf. % | Anzahl | ||

|---|---|---|---|---|---|---|---|

| 1. | 1. | 18.183,67 | +1,42 | 237 | |||

| 2. | 2. | 1,1100 | -19,57 | 110 | |||

| 3. | 3. | 0,1855 | -1,85 | 100 | |||

| 4. | 5. | 9,3150 | +0,76 | 65 | |||

| 5. | 4. | 169,76 | -0,25 | 55 | |||

| 6. | Neu! | 0,4250 | -1,16 | 39 | |||

| 7. | Neu! | 4,7440 | +5,77 | 34 | |||

| 8. | Neu! | 11,905 | +14,97 | 32 |

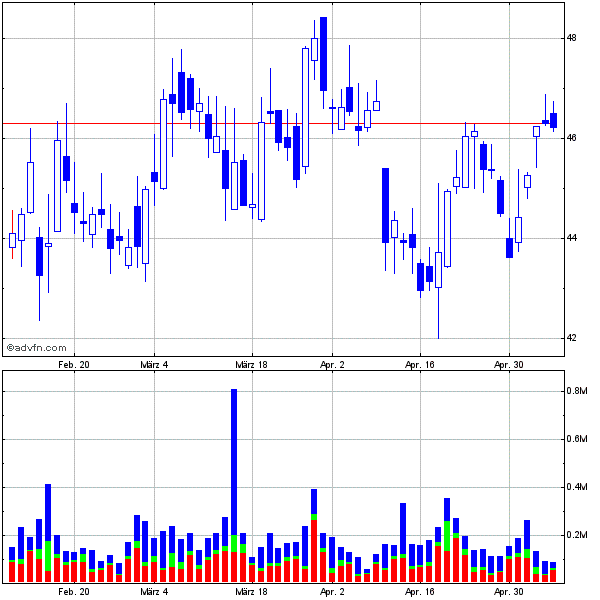

Hier zeichnet sich eine lehrbuchartige charttechnische Trendwende an. Mein persönliches kurzfristiges Kursziel (auf sicht dieser Woche) sind die 3,50 USD (GAP-Schluss):

Banner Corporation (BANR: 2.38 +0.01 +0.42%) broke out Monday on huge volume. If this chart does what is supposed to do, it will be going higher in the days to come. Technically, the stock is in a short-term Bull Market with share price above 5, 13 and 20 daily moving averages. Let’s see if Tuesday the stock will confirm the breakout. Short-term investors can buy with a stop at $2.31 and long-term investors can hold with a stop at $2.08. Let’s keep an eye on her as i think momentum will pick up.

http://www.dailymarkets.com/stock/2010/07/26/stock-picks-for…

http://www.dailymarkets.com/stock/2010/07/26/stock-picks-for…

RT-Kurs und News: http://www.google.com/finance?q=banr

RT-Daten von BANR von CNBC: http://data.cnbc.com/quotes/BANR

Trading Spotlight

After Hour Quotes: http://www.nasdaq.com/aspxcontent/ExtendedTradingTrades.aspx…

Banner Corporation Announces Webcast Details for Keefe, Bruyette & Woods Community Bank Investor Conference Presentation

WALLA WALLA, Wash., July 26, 2010 (GLOBE NEWSWIRE) -- Banner Corporation (Nasdaq:BANR), the parent company of Banner Bank and Islanders Bank, today announced that Banner's management team is scheduled to present at the Keefe, Bruyette & Woods 2010 Community Bank Investor Conference in New York.

D. Michael Jones, CEO, Mark J. Grescovich, President, and Lloyd W. Baker, CFO, are scheduled to present Wednesday, July 28, 2010, at 11:00 a.m. PDT (2:00 p.m. EDT). The live and archived presentation can be viewed at http://www.kbw.com/news/conferenceCommunity2010_Webcast.html…

About the Company

Banner Corporation is a $4.7 billion bank holding company operating two commercial banks in Washington, Oregon and Idaho. Banner serves the Pacific Northwest region with a full range of deposit services and business, commercial real estate, construction, residential, agricultural and consumer loans. Visit Banner Bank on the Web at www.bannerbank.com.

CONTACT: Banner CorporationD. Michael Jones, CEO

Mark J. Grescovich, President

Lloyd W. Baker, CFO

(509) 527-3636

Read more: http://www.nasdaq.com/aspx/company-news-story.aspx?storyid=2… &title=banner-corporation-announces-webcast-details-for-keefe-bruyette--woods-community-bank-investor-conference-presentation#ixzz0uvT2oVI5

http://www.nasdaq.com/aspx/company-news-story.aspx?storyid=2…

WALLA WALLA, Wash., July 26, 2010 (GLOBE NEWSWIRE) -- Banner Corporation (Nasdaq:BANR), the parent company of Banner Bank and Islanders Bank, today announced that Banner's management team is scheduled to present at the Keefe, Bruyette & Woods 2010 Community Bank Investor Conference in New York.

D. Michael Jones, CEO, Mark J. Grescovich, President, and Lloyd W. Baker, CFO, are scheduled to present Wednesday, July 28, 2010, at 11:00 a.m. PDT (2:00 p.m. EDT). The live and archived presentation can be viewed at http://www.kbw.com/news/conferenceCommunity2010_Webcast.html…

About the Company

Banner Corporation is a $4.7 billion bank holding company operating two commercial banks in Washington, Oregon and Idaho. Banner serves the Pacific Northwest region with a full range of deposit services and business, commercial real estate, construction, residential, agricultural and consumer loans. Visit Banner Bank on the Web at www.bannerbank.com.

CONTACT: Banner CorporationD. Michael Jones, CEO

Mark J. Grescovich, President

Lloyd W. Baker, CFO

(509) 527-3636

Read more: http://www.nasdaq.com/aspx/company-news-story.aspx?storyid=2… &title=banner-corporation-announces-webcast-details-for-keefe-bruyette--woods-community-bank-investor-conference-presentation#ixzz0uvT2oVI5

http://www.nasdaq.com/aspx/company-news-story.aspx?storyid=2…

Aus dem Yahoo-Board zu vermehrten Insider-Käufen:

▀▀▀»»»INSIDERS INCREASING»»»»▀▀▀ 27-Jul-10 12:47 am Banner Corp (BANR)

$1.47M, Form4Oracle Insider Sentiment Rating – Strong Buy:

Orrico Brent A, Director bought $650.00K, increasing his holdings by 174%

Smith Michael Marion, Director bought $50.00K, increasing his holdings by 25%

Sirmon Gary, Director bought $100.00K, increasing his holdings by 24%

Jones D Michael, Chief Executive Officer,Director bought $150.00K, increasing his holdings by 90%

Grescovich Mark J, President,Director bought $100.00K, increasing his holdings by 100%

Epstein Edward L, Director bought $50.00K, increasing his holdings by 733%

Mitchell Dean W, Director bought $40.00K, increasing his holdings by 23%

Lane Robert J, Director bought $60.00K, increasing his holdings by 1000%

Baker Lloyd W, Executive Vice President bought $60.00K, increasing his holdings by 74%

Wagers Gary W, Executive VP, Banner Bank bought $100.00K, increasing his holdings by 493% »♦ALL THESE TRANSACTIONS WERE WITHIN THE LAST 90 DAYS.... HOLD STRONG & LONG

http://messages.finance.yahoo.com/Business_%26_Finance/Inves…

▀▀▀»»»INSIDERS INCREASING»»»»▀▀▀ 27-Jul-10 12:47 am Banner Corp (BANR)

$1.47M, Form4Oracle Insider Sentiment Rating – Strong Buy:

Orrico Brent A, Director bought $650.00K, increasing his holdings by 174%

Smith Michael Marion, Director bought $50.00K, increasing his holdings by 25%

Sirmon Gary, Director bought $100.00K, increasing his holdings by 24%

Jones D Michael, Chief Executive Officer,Director bought $150.00K, increasing his holdings by 90%

Grescovich Mark J, President,Director bought $100.00K, increasing his holdings by 100%

Epstein Edward L, Director bought $50.00K, increasing his holdings by 733%

Mitchell Dean W, Director bought $40.00K, increasing his holdings by 23%

Lane Robert J, Director bought $60.00K, increasing his holdings by 1000%

Baker Lloyd W, Executive Vice President bought $60.00K, increasing his holdings by 74%

Wagers Gary W, Executive VP, Banner Bank bought $100.00K, increasing his holdings by 493% »♦ALL THESE TRANSACTIONS WERE WITHIN THE LAST 90 DAYS.... HOLD STRONG & LONG

http://messages.finance.yahoo.com/Business_%26_Finance/Inves…

Insider-Tranaktionen: http://www.form4oracle.com/company/whx-corp-wxco/company-tra…

was machen die?

Antwort auf Beitrag Nr.: 39.886.587 von MrRipley am 28.07.10 01:15:36"was machen die?"

Business Description: A bank holding company is primarily engaged in the business of planning, directing and coordinating the business activities of two wholly owned subsidiaries, Banner Bank and Islanders Bank.

Business Description: A bank holding company is primarily engaged in the business of planning, directing and coordinating the business activities of two wholly owned subsidiaries, Banner Bank and Islanders Bank.

Firmenhomepage: http://www.bannerbank.com/pages/default.aspx

Ergebnisse Q2 2010:

07/21/10 - 2nd Qtr 2010 Results

Banner Corporation Announces Second Quarter Results

Walla Walla, WA – July 21, 2010 - Banner Corporation (NASDAQ GSM: BANR), the parent company of Banner Bank and Islanders Bank, today reported that it had a net loss of $4.9 million in the second quarter ended June 30, 2010, compared to a net loss of $1.5 million in the immediately preceding quarter and a net loss of $16.5 million in the second quarter a year ago.

“Our second quarter was highlighted by a successful capital raise and a continued reduction in our deposit costs which contributed to net interest margin expansion for the fourth consecutive quarter,” said D. Michael Jones, Chief Executive Officer. “We are making a concerted effort to reduce the overall cost of the deposit portfolio, and with our improved liquidity position we are able to let higher cost funding, primarily certificates of deposit and wholesale funds, run off. Our deposit mix improvement reflects continuing growth in customer relationships as a result of the determined efforts of our staff and the further maturing of the expanded branch network we have built over the past five years. Despite the current difficult economic environment, we are optimistic that the strength of this deposit franchise and our improved capital position will provide the foundation for better operating results in future periods.”

In the second quarter, Banner paid a $1.6 million dividend on the $124 million of senior preferred stock it issued to the U.S. Treasury in the fourth quarter of 2008 in connection with its participation in the Treasury’s Capital Purchase Program. In addition, Banner accrued $399,000 for related discount accretion. Including the preferred stock dividend and related accretion, the net loss to common shareholders was $6.9 million, or $0.28 per share, for the second quarter of 2010, compared to a net loss to common shareholders of $3.5 million, or $0.16 per share, in the first quarter of 2010 and a net loss to common shareholders of $18.4 million, or $1.04 per share, for the second quarter a year ago.

For the first six months of 2010, Banner reported a net loss of $6.5 million compared to a net loss of $25.8 million for the first six months of 2009. For the most recent six month period, the net loss to common shareholders was $0.44 per share, compared to a net loss of $1.70 per share for the first six months of 2009.

Common Stock Offering

On June 30, 2010, Banner announced the completion of its offering of 75,000,000 shares of its common stock and the sale of an additional 3,500,000 shares pursuant to the partial exercise of the underwriters’ over-allotment option, at a price to the public of $2.00 per share. On July 2, 2010, Banner announced the completion of the capital raise as the underwriters had exercised their over-allotment option for an additional 7,139,000 shares, at a price to the public of $2.00 per share. Together with the 78,500,000 shares the Company issued on June 30, 2010 (including 3,500,000 shares issued pursuant to the underwriters’ initial exercise of their over-allotment option), Banner issued a total of 85,639,000 shares in the offering, resulting in net proceeds, after deducting underwriting discounts and commissions and estimated offering expenses, of approximately $161.6 million.

Banner intends to use a significant portion of the net proceeds from the offering to strengthen Banner Bank’s regulatory capital ratios and to support managed growth. To that end, at June 30, 2010, the Company had invested $50 million as additional paid-in common equity in Banner Bank. The Company expects to use the remaining net proceeds for general working capital purposes, including additional capital investments in its subsidiary banks if appropriate.

Income Statement Review

“Continued reductions in our cost of funds through changes in our deposit mix and reduced pricing pressures over the past year resulted in further expansion of our net interest margin during the second quarter of 2010 to 3.65%, an increase of four basis points compared to the immediately preceding quarter and an increase of 41 basis points compared to the same quarter a year ago,” said Jones. “While loan yields have been relatively stable for a number of quarters now, overall asset yields have declined slightly primarily as a result of the growth of our on-balance-sheet liquidity which is currently invested in short term instruments that pay very low interest rates.” Banner’s net interest margin was 3.65% for the second quarter, compared to 3.61% in the preceding quarter and 3.24% in the second quarter a year ago. For the first six months of 2010, Banner’s net interest margin was 3.62%, a 37 basis point improvement compared to the first six months of 2009.

For the second quarter of 2010, funding costs decreased 13 basis points compared to the previous quarter and 77 basis points from the second quarter a year ago. Deposit costs decreased by 15 basis points compared to the preceding quarter and 82 basis points compared to the second quarter a year earlier. Asset yields decreased eight basis points from the prior linked quarter and 28 basis points from the second quarter a year ago. Loan yields declined by two basis points compared to the preceding quarter, but increased by five basis points from the second quarter a year ago. Non-accruing loans reduced the margin by approximately 34 basis points in the second quarter of 2010 compared to approximately 34 basis points in the preceding quarter and approximately 45 basis points in the second quarter of 2009.

Net interest income before the provision for loan losses was $38.9 million in the second quarter of 2010, compared to $38.2 million in the preceding quarter and $34.9 million in the second quarter a year ago. In the first half of 2010, net interest income before the provision for loan losses increased 10% to $77.1 million, compared to $69.9 million in the first half of 2009. Revenues from core operations* (net interest income before the provision for loan losses plus total other operating income excluding fair value and other-than-temporary impairment (OTTI) adjustments) were $45.9 million in the second quarter of 2010, compared to $45.2 million in the first quarter of 2010 and $43.9 million for the second quarter a year ago. Revenues from core operations for the first half of 2010 increased 5% to $91.1 million, compared to $86.7 million in the first half of 2009.

Second quarter 2010 results included a net loss of $821,000 ($525,000 after tax, or $0.02 loss per share) for fair value adjustments as a result of changes in the valuation of financial instruments carried at fair value, compared to a net gain (net of OTTI charges) of $677,000 ($433,000 after tax, or $0.02 earnings per share) in the first quarter of 2010 and a net gain (net of OTTI charges) of $11.0 million ($7.0 million after tax, or $0.62 earnings per share) in the second quarter a year ago. There were no OTTI charges in the second quarter of 2010, compared to $1.2 million in the first quarter of 2010 and $162,000 in the second quarter of 2009.

Total other operating income, which includes the changes in the valuation of financial instruments noted above, was $6.2 million, or $0.25 per share, in the second quarter of 2010, compared to $7.7 million, or $0.35 per share, in the preceding quarter and $20.0 million, or $1.13 per share, for the second quarter a year ago. For the first half of 2010, total other operating income was $13.9 million, compared to $24.6 million in the first half of 2009. Total other operating income from core operations* (excluding fair value and OTTI adjustments) for the current quarter was $7.0 million, unchanged from the preceding quarter, and was $8.9 million for the second quarter a year ago. For the first half of 2010, total other operating income from core operations was $14.0 million, compared to $16.8 million in the first half of 2009. Income from deposit fees and other service charges improved modestly to $5.6 million in the second quarter compared to $5.2 million in the preceding quarter and $5.4 million in the second quarter a year ago. Income from mortgage banking operations decreased to $817,000 in the second quarter compared to $948,000 in the preceding quarter and $2.9 million for the second quarter a year ago.

“Our payment processing business continues to be adversely affected by the soft economy, as activity for cardholders and merchants remained lower than in periods before 2009,” said Jones. “However, we are encouraged by the improvement in deposit fees and other service charges compared to the preceding quarter, which in addition to reflecting account growth may be a sign of improving economic conditions.” By contrast, mortgage banking revenues continued to decline, reflecting decreased mortgage loan production despite the current very low level of mortgage interest rates.

“We have made progress in improving our core operating efficiency as compensation, occupancy and other manageable operating expenses have been reduced over the past year,” said Jones. “Unfortunately, collection and legal costs, including charges related to acquired real estate, continue to remain high. We expect collection expenses and costs associated with real estate to remain elevated for a number of future quarters as we work down our inventory of non-performing assets.”

Total other operating expenses, or non-interest expenses, were $38.0 million in the second quarter of 2010, compared to $35.4 million in the preceding quarter and $36.9 million in the second quarter a year ago. For the first half of the year, other operating expenses were $73.4 million compared to $70.7 million in the first half of 2009. Largely as the result of the increase in REO and collection costs, operating expenses as a percentage of average assets increased to 3.35% in the second quarter of 2010, compared to 3.16% in the preceding quarter and 3.27% in the second quarter a year ago.

*Earnings information excluding fair value adjustments (alternately referred to as total other operating income from core operation or revenues from core operations) represent non-GAAP (Generally Accepted Accounting Principles) financial measures. Management has presented these non-GAAP financial measures in this earnings release because it believes that they provide useful and comparative information to assess trends in the Company’s core operations reflected in the current quarter’s results. Where applicable, the Company has also presented comparable earnings information using GAAP financial measures.

Credit Quality

“The credit costs associated with this difficult economic environment have been a persistent challenge throughout the past several quarters and continue to drag on profitability,” said Jones. “The $16 million provision for loan losses in the second quarter of the year, while less than in the second quarter a year ago, remains high, reflecting still significant levels of non-performing loans and net charge-offs. Charge-offs and delinquencies continue to be concentrated in loans for the construction of single-family homes and residential land development projects. However, our exposure to single-family home construction and development loans has continued to decline and at June 30, 2010 was 11% of total loans outstanding. Our reserve levels are substantial and both our impairment analysis and charge-off actions reflect current appraisals and valuation estimates. We remain hopeful that credit costs will moderate during the remainder of 2010 and in 2011.”

Banner recorded a $16.0 million provision for loan losses in the second quarter, compared to $14.0 million in the preceding quarter and $45.0 million in the second quarter a year ago. For the first six months of 2010, the provision for loan losses was $30.0 million, compared to $67.0 million for the first six months of 2009. The allowance for loan losses at June 30, 2010 totaled $95.5 million, representing 2.63% of total loans outstanding and 54% of non-performing loans. Non-performing loans totaled $177.2 million at June 30, 2010, compared to $196.0 million in the preceding quarter and $225.1 million at June 30, 2009. Banner’s real estate owned and repossessed assets totaled $101.7 million at June 30, 2010, compared to $95.2 million three months earlier and $57.2 million a year ago. Net charge-offs in the quarter totaled $16.2 million, or 0.44% of average loans outstanding, compared to $13.5 million, or 0.36% of average loans outstanding for the first quarter of 2010 and $34.0 million, or 0.87% of average loans outstanding for the second quarter of last year. Non-performing assets totaled $282.4 million at June 30, 2010, compared to $294.2 million in the preceding quarter and $282.3 million at June 30, 2009. At the end of June, Banner’s non-performing assets were 6.01% of total assets, compared to 6.42% at the end of the preceding quarter and 6.23% a year ago.

The geographic distribution of construction, land and land development loans, including residential and commercial properties, was approximately $194 million, or 33%, in the greater Puget Sound market, $208 million, or 36%, in the greater Portland, Oregon market and $39 million, or 7%, in the greater Boise, Idaho market as of June 30, 2010. The remaining $140 million, or 24%, was distributed in the various eastern Washington, eastern Oregon and northern Idaho markets served by Banner Bank. The geographic distribution of non-performing construction, land and land development loans and related real estate owned included approximately $83 million, or 46%, in the greater Puget Sound market, $64 million, or 35%, in the greater Portland market and $14 million, or 8%, in the greater Boise market, with the remaining $20 million, or 11%, distributed in the various eastern Washington, eastern Oregon and northern Idaho markets served by Banner Bank.

One-to-four family residential construction, lot and land loans were $411 million, or 11% of the total loan portfolio at June 30, 2010. Non-performing residential construction, lot and land loans and related real estate owned were $155 million, or 55% of non-performing assets at June 30, 2010.

Balance Sheet Review

“As we have substantially reduced our construction and land development loans over the past year, our total loan balances declined relative to a year ago; however, we did have encouraging growth in commercial and agricultural business loans during the quarter,” said Jones. “At the end of June, our one-to-four family construction loans totaled $183 million, a $154 million reduction over the past year, including a $31 million decrease in the most recent quarter. Our one-to-four family construction loans have now declined by $472 million from their peak quarter-end balance of $655 million at June 30, 2007. Similarly, total construction, land and land development loans have declined by $654 million from their peak quarter-end balance of $1.24 billion, also at June 30, 2007.” Net loans were $3.54 billion at June 30, 2010, compared to $3.59 billion three months earlier and $3.82 billion at June 30, 2009.

Total assets were $4.70 billion at June 30, 2010, compared to $4.58 billion at the end of the preceding quarter and $4.53 billion a year ago. Deposits totaled $3.84 billion at June 30, 2010, compared to $3.85 billion at the end of the preceding quarter and $3.75 billion a year ago. Non-interest-bearing accounts were $548.3 million at June 30, 2010, compared to $549.3 million at the end of the preceding quarter and $508.3 million a year ago, a year-over-year increase of 8%. At June 30, 2010, interest-bearing transaction and savings accounts were $1.4 billion, which was unchanged from three months earlier but a $272.1 million increase compared to $1.1 billion a year ago, a year-over-year increase of 24%.

“Banner’s retail deposit franchise had another solid quarter and has allowed us to steadily build our short-term liquidity and lower our loans-to-deposits ratio, which was 95% at June 30, 2010,” said Jones. “In addition, this substantial core deposit growth has led to our improved net interest margin and increased deposit fee revenue.”

Augmented by the recent stock offering, Banner Corporation and its subsidiary banks continue to maintain capital levels significantly in excess of the requirements to be categorized as “well-capitalized” under applicable regulatory standards. Banner Corporation’s Tier 1 leverage capital to average assets ratio was 13.02% and its total capital to risk-weighted assets ratio was 17.12% at June 30, 2010. Importantly, reflecting the $50 million down-streamed capital investment, Banner Bank’s Tier 1 leverage ratio increased to 10.77% at June 30, 2010.

Tangible stockholders’ equity at June 30, 2010 was $544.1 million, including $118.2 million attributable to preferred stock, compared to $397.1 million a year ago. Tangible book value per common share was $4.15 at quarter-end. At June 30, 2010, Banner had 102.7 million shares outstanding, compared to 18.2 million shares outstanding a year ago. Tangible common stockholders’ equity was $425.9 million at June 30, 2010, or 9.08% of tangible assets, compared to $278.5 million, or 6.09% of tangible assets at March 31, 2010 and $280.4 million, or 6.20% of tangible assets at June 30, 2009.

Conference Call

Banner will host a conference call on Thursday, July 22, 2010, at 8:00 a.m. PDT, to discuss second quarter 2010 results. The conference call can be accessed live by telephone at 480-629-9772 to participate in the call. To listen to the call online, go to the Company’s website at www.bannerbank.com. A replay will be available for a week at (303) 590-3030, using access code 4326727.

About the Company

Banner Corporation is a $4.7 billion bank holding company operating two commercial banks in Washington, Oregon and Idaho. Banner serves the Pacific Northwest region with a full range of deposit services and business, commercial real estate, construction, residential, agricultural and consumer loans. Visit Banner Bank on the Web at www.bannerbank.com.

This press release contains statements that the Company believes are “forward-looking statements.” These statements relate to the Company’s financial condition, results of operations, plans, objectives, future performance or business. You should not place undue reliance on these statements, as they are subject to risks and uncertainties. When considering these forward-looking statements, you should keep in mind these risks and uncertainties, as well as any cautionary statements the Company may make. Moreover, you should treat these statements as speaking only as of the date they are made and based only on information then actually known to the Company. There are a number of important factors that could cause future results to differ materially from historical performance and these forward-looking statements. Factors which could cause actual results to differ materially include, but are not limited to, the credit risks of lending activities, including changes in the level and trend of loan delinquencies and write-offs and changes in our allowance for loan losses and provision for loan losses that may be impacted by deterioration in the housing and commercial real estate markets; changes in general economic conditions, either nationally or in our market areas; changes in the levels of general interest rates and the relative differences between short and long-term interest rates, deposit interest rates, our net interest margin and funding sources; fluctuations in the demand for loans, the number of unsold homes, land and other properties and fluctuations in real estate values in our market areas; secondary market conditions for loans and our ability to sell loans in the secondary market; results of examinations of us by the Board of Governors of the Federal Reserve System and of our bank subsidiaries by the Federal Deposit Insurance Corporation, the Washington State Department of Financial Institutions, Division of Banks or other regulatory authorities, including the possibility that any such regulatory authority may, among other things, institute a formal or informal enforcement action against us or any of the Banks which could require us to increase our reserve for loan losses, write-down assets, change our regulatory capital position or affect our ability to borrow funds or maintain or increase deposits, which could adversely affect our liquidity and earnings; our compliance with regulatory enforcement actions; the requirements and restrictions that have been imposed upon Banner and Banner Bank under the memoranda of understanding with the Federal Reserve Bank of San Francisco (in the case of Banner) and the FDIC and the Washington DFI (in the case of Banner Bank) and the possibility that Banner and Banner Bank will be unable to fully comply with the memoranda of understanding, which could result in the imposition of additional requirements or restrictions; legislative or regulatory changes that adversely affect our business including changes in regulatory policies and principles, or the interpretation of regulatory capital or other rules; our ability to attract and retain deposits; further increases in premiums for deposit insurance; our ability to control operating costs and expenses; the use of estimates in determining fair value of certain of our assets, which estimates may prove to be incorrect or result in significant declines in valuation; staffing fluctuations in response to product demand or the implementation of corporate strategies that affect our workforce and potential associated charges; the failure or security breach of computer systems on which we depend; our ability to retain key members of our senior management team; costs and effects of litigation, including settlements and judgments; our ability to implement our business strategies; our ability to successfully integrate any assets, liabilities, customers, systems, and management personnel we may acquire into our operations and our ability to realize related revenue synergies and cost savings within expected time frames and any goodwill charges related thereto; increased competitive pressures among financial services companies; changes in consumer spending, borrowing and savings habits; the availability of resources to address changes in laws, rules, or regulations or to respond to regulatory actions; our ability to pay dividends on our common and preferred stock and interest or principal payments on our junior subordinated debentures; adverse changes in the securities markets; inability of key third-party providers to perform their obligations to us; changes in accounting policies and practices, as may be adopted by the financial institution regulatory agencies or the Financial Accounting Standards Board including additional guidance and interpretation on accounting issues and details of the implementation of new accounting methods; war or terrorist activities; other economic, competitive, governmental, regulatory, and technological factors affecting our operations, pricing, products and services; future legislative changes in the United States Department of Treasury Troubled Asset Relief Program Capital Purchase Program; and other risks detailed in Banner’s reports filed with the Securities and Exchange Commission, including its Annual Report on Form 10-K for the year ended December 31, 2009. We do not undertake and specifically disclaim any obligation to revise any forward-looking statements to reflect the occurrence of anticipated or unanticipated events or circumstances after the date of such statements. These risks could cause our actual results for 2010 and beyond to differ materially from those expressed in any forward-looking statements by, or on behalf of, us, and could negatively affect our operating and stock price performance.

http://www.bannerbank.com/News/Pages/072110_2Q10_Results.asp…

07/21/10 - 2nd Qtr 2010 Results

Banner Corporation Announces Second Quarter Results

Walla Walla, WA – July 21, 2010 - Banner Corporation (NASDAQ GSM: BANR), the parent company of Banner Bank and Islanders Bank, today reported that it had a net loss of $4.9 million in the second quarter ended June 30, 2010, compared to a net loss of $1.5 million in the immediately preceding quarter and a net loss of $16.5 million in the second quarter a year ago.

“Our second quarter was highlighted by a successful capital raise and a continued reduction in our deposit costs which contributed to net interest margin expansion for the fourth consecutive quarter,” said D. Michael Jones, Chief Executive Officer. “We are making a concerted effort to reduce the overall cost of the deposit portfolio, and with our improved liquidity position we are able to let higher cost funding, primarily certificates of deposit and wholesale funds, run off. Our deposit mix improvement reflects continuing growth in customer relationships as a result of the determined efforts of our staff and the further maturing of the expanded branch network we have built over the past five years. Despite the current difficult economic environment, we are optimistic that the strength of this deposit franchise and our improved capital position will provide the foundation for better operating results in future periods.”

In the second quarter, Banner paid a $1.6 million dividend on the $124 million of senior preferred stock it issued to the U.S. Treasury in the fourth quarter of 2008 in connection with its participation in the Treasury’s Capital Purchase Program. In addition, Banner accrued $399,000 for related discount accretion. Including the preferred stock dividend and related accretion, the net loss to common shareholders was $6.9 million, or $0.28 per share, for the second quarter of 2010, compared to a net loss to common shareholders of $3.5 million, or $0.16 per share, in the first quarter of 2010 and a net loss to common shareholders of $18.4 million, or $1.04 per share, for the second quarter a year ago.

For the first six months of 2010, Banner reported a net loss of $6.5 million compared to a net loss of $25.8 million for the first six months of 2009. For the most recent six month period, the net loss to common shareholders was $0.44 per share, compared to a net loss of $1.70 per share for the first six months of 2009.

Common Stock Offering

On June 30, 2010, Banner announced the completion of its offering of 75,000,000 shares of its common stock and the sale of an additional 3,500,000 shares pursuant to the partial exercise of the underwriters’ over-allotment option, at a price to the public of $2.00 per share. On July 2, 2010, Banner announced the completion of the capital raise as the underwriters had exercised their over-allotment option for an additional 7,139,000 shares, at a price to the public of $2.00 per share. Together with the 78,500,000 shares the Company issued on June 30, 2010 (including 3,500,000 shares issued pursuant to the underwriters’ initial exercise of their over-allotment option), Banner issued a total of 85,639,000 shares in the offering, resulting in net proceeds, after deducting underwriting discounts and commissions and estimated offering expenses, of approximately $161.6 million.

Banner intends to use a significant portion of the net proceeds from the offering to strengthen Banner Bank’s regulatory capital ratios and to support managed growth. To that end, at June 30, 2010, the Company had invested $50 million as additional paid-in common equity in Banner Bank. The Company expects to use the remaining net proceeds for general working capital purposes, including additional capital investments in its subsidiary banks if appropriate.

Income Statement Review

“Continued reductions in our cost of funds through changes in our deposit mix and reduced pricing pressures over the past year resulted in further expansion of our net interest margin during the second quarter of 2010 to 3.65%, an increase of four basis points compared to the immediately preceding quarter and an increase of 41 basis points compared to the same quarter a year ago,” said Jones. “While loan yields have been relatively stable for a number of quarters now, overall asset yields have declined slightly primarily as a result of the growth of our on-balance-sheet liquidity which is currently invested in short term instruments that pay very low interest rates.” Banner’s net interest margin was 3.65% for the second quarter, compared to 3.61% in the preceding quarter and 3.24% in the second quarter a year ago. For the first six months of 2010, Banner’s net interest margin was 3.62%, a 37 basis point improvement compared to the first six months of 2009.

For the second quarter of 2010, funding costs decreased 13 basis points compared to the previous quarter and 77 basis points from the second quarter a year ago. Deposit costs decreased by 15 basis points compared to the preceding quarter and 82 basis points compared to the second quarter a year earlier. Asset yields decreased eight basis points from the prior linked quarter and 28 basis points from the second quarter a year ago. Loan yields declined by two basis points compared to the preceding quarter, but increased by five basis points from the second quarter a year ago. Non-accruing loans reduced the margin by approximately 34 basis points in the second quarter of 2010 compared to approximately 34 basis points in the preceding quarter and approximately 45 basis points in the second quarter of 2009.

Net interest income before the provision for loan losses was $38.9 million in the second quarter of 2010, compared to $38.2 million in the preceding quarter and $34.9 million in the second quarter a year ago. In the first half of 2010, net interest income before the provision for loan losses increased 10% to $77.1 million, compared to $69.9 million in the first half of 2009. Revenues from core operations* (net interest income before the provision for loan losses plus total other operating income excluding fair value and other-than-temporary impairment (OTTI) adjustments) were $45.9 million in the second quarter of 2010, compared to $45.2 million in the first quarter of 2010 and $43.9 million for the second quarter a year ago. Revenues from core operations for the first half of 2010 increased 5% to $91.1 million, compared to $86.7 million in the first half of 2009.

Second quarter 2010 results included a net loss of $821,000 ($525,000 after tax, or $0.02 loss per share) for fair value adjustments as a result of changes in the valuation of financial instruments carried at fair value, compared to a net gain (net of OTTI charges) of $677,000 ($433,000 after tax, or $0.02 earnings per share) in the first quarter of 2010 and a net gain (net of OTTI charges) of $11.0 million ($7.0 million after tax, or $0.62 earnings per share) in the second quarter a year ago. There were no OTTI charges in the second quarter of 2010, compared to $1.2 million in the first quarter of 2010 and $162,000 in the second quarter of 2009.

Total other operating income, which includes the changes in the valuation of financial instruments noted above, was $6.2 million, or $0.25 per share, in the second quarter of 2010, compared to $7.7 million, or $0.35 per share, in the preceding quarter and $20.0 million, or $1.13 per share, for the second quarter a year ago. For the first half of 2010, total other operating income was $13.9 million, compared to $24.6 million in the first half of 2009. Total other operating income from core operations* (excluding fair value and OTTI adjustments) for the current quarter was $7.0 million, unchanged from the preceding quarter, and was $8.9 million for the second quarter a year ago. For the first half of 2010, total other operating income from core operations was $14.0 million, compared to $16.8 million in the first half of 2009. Income from deposit fees and other service charges improved modestly to $5.6 million in the second quarter compared to $5.2 million in the preceding quarter and $5.4 million in the second quarter a year ago. Income from mortgage banking operations decreased to $817,000 in the second quarter compared to $948,000 in the preceding quarter and $2.9 million for the second quarter a year ago.

“Our payment processing business continues to be adversely affected by the soft economy, as activity for cardholders and merchants remained lower than in periods before 2009,” said Jones. “However, we are encouraged by the improvement in deposit fees and other service charges compared to the preceding quarter, which in addition to reflecting account growth may be a sign of improving economic conditions.” By contrast, mortgage banking revenues continued to decline, reflecting decreased mortgage loan production despite the current very low level of mortgage interest rates.

“We have made progress in improving our core operating efficiency as compensation, occupancy and other manageable operating expenses have been reduced over the past year,” said Jones. “Unfortunately, collection and legal costs, including charges related to acquired real estate, continue to remain high. We expect collection expenses and costs associated with real estate to remain elevated for a number of future quarters as we work down our inventory of non-performing assets.”

Total other operating expenses, or non-interest expenses, were $38.0 million in the second quarter of 2010, compared to $35.4 million in the preceding quarter and $36.9 million in the second quarter a year ago. For the first half of the year, other operating expenses were $73.4 million compared to $70.7 million in the first half of 2009. Largely as the result of the increase in REO and collection costs, operating expenses as a percentage of average assets increased to 3.35% in the second quarter of 2010, compared to 3.16% in the preceding quarter and 3.27% in the second quarter a year ago.

*Earnings information excluding fair value adjustments (alternately referred to as total other operating income from core operation or revenues from core operations) represent non-GAAP (Generally Accepted Accounting Principles) financial measures. Management has presented these non-GAAP financial measures in this earnings release because it believes that they provide useful and comparative information to assess trends in the Company’s core operations reflected in the current quarter’s results. Where applicable, the Company has also presented comparable earnings information using GAAP financial measures.

Credit Quality

“The credit costs associated with this difficult economic environment have been a persistent challenge throughout the past several quarters and continue to drag on profitability,” said Jones. “The $16 million provision for loan losses in the second quarter of the year, while less than in the second quarter a year ago, remains high, reflecting still significant levels of non-performing loans and net charge-offs. Charge-offs and delinquencies continue to be concentrated in loans for the construction of single-family homes and residential land development projects. However, our exposure to single-family home construction and development loans has continued to decline and at June 30, 2010 was 11% of total loans outstanding. Our reserve levels are substantial and both our impairment analysis and charge-off actions reflect current appraisals and valuation estimates. We remain hopeful that credit costs will moderate during the remainder of 2010 and in 2011.”

Banner recorded a $16.0 million provision for loan losses in the second quarter, compared to $14.0 million in the preceding quarter and $45.0 million in the second quarter a year ago. For the first six months of 2010, the provision for loan losses was $30.0 million, compared to $67.0 million for the first six months of 2009. The allowance for loan losses at June 30, 2010 totaled $95.5 million, representing 2.63% of total loans outstanding and 54% of non-performing loans. Non-performing loans totaled $177.2 million at June 30, 2010, compared to $196.0 million in the preceding quarter and $225.1 million at June 30, 2009. Banner’s real estate owned and repossessed assets totaled $101.7 million at June 30, 2010, compared to $95.2 million three months earlier and $57.2 million a year ago. Net charge-offs in the quarter totaled $16.2 million, or 0.44% of average loans outstanding, compared to $13.5 million, or 0.36% of average loans outstanding for the first quarter of 2010 and $34.0 million, or 0.87% of average loans outstanding for the second quarter of last year. Non-performing assets totaled $282.4 million at June 30, 2010, compared to $294.2 million in the preceding quarter and $282.3 million at June 30, 2009. At the end of June, Banner’s non-performing assets were 6.01% of total assets, compared to 6.42% at the end of the preceding quarter and 6.23% a year ago.

The geographic distribution of construction, land and land development loans, including residential and commercial properties, was approximately $194 million, or 33%, in the greater Puget Sound market, $208 million, or 36%, in the greater Portland, Oregon market and $39 million, or 7%, in the greater Boise, Idaho market as of June 30, 2010. The remaining $140 million, or 24%, was distributed in the various eastern Washington, eastern Oregon and northern Idaho markets served by Banner Bank. The geographic distribution of non-performing construction, land and land development loans and related real estate owned included approximately $83 million, or 46%, in the greater Puget Sound market, $64 million, or 35%, in the greater Portland market and $14 million, or 8%, in the greater Boise market, with the remaining $20 million, or 11%, distributed in the various eastern Washington, eastern Oregon and northern Idaho markets served by Banner Bank.

One-to-four family residential construction, lot and land loans were $411 million, or 11% of the total loan portfolio at June 30, 2010. Non-performing residential construction, lot and land loans and related real estate owned were $155 million, or 55% of non-performing assets at June 30, 2010.

Balance Sheet Review

“As we have substantially reduced our construction and land development loans over the past year, our total loan balances declined relative to a year ago; however, we did have encouraging growth in commercial and agricultural business loans during the quarter,” said Jones. “At the end of June, our one-to-four family construction loans totaled $183 million, a $154 million reduction over the past year, including a $31 million decrease in the most recent quarter. Our one-to-four family construction loans have now declined by $472 million from their peak quarter-end balance of $655 million at June 30, 2007. Similarly, total construction, land and land development loans have declined by $654 million from their peak quarter-end balance of $1.24 billion, also at June 30, 2007.” Net loans were $3.54 billion at June 30, 2010, compared to $3.59 billion three months earlier and $3.82 billion at June 30, 2009.

Total assets were $4.70 billion at June 30, 2010, compared to $4.58 billion at the end of the preceding quarter and $4.53 billion a year ago. Deposits totaled $3.84 billion at June 30, 2010, compared to $3.85 billion at the end of the preceding quarter and $3.75 billion a year ago. Non-interest-bearing accounts were $548.3 million at June 30, 2010, compared to $549.3 million at the end of the preceding quarter and $508.3 million a year ago, a year-over-year increase of 8%. At June 30, 2010, interest-bearing transaction and savings accounts were $1.4 billion, which was unchanged from three months earlier but a $272.1 million increase compared to $1.1 billion a year ago, a year-over-year increase of 24%.

“Banner’s retail deposit franchise had another solid quarter and has allowed us to steadily build our short-term liquidity and lower our loans-to-deposits ratio, which was 95% at June 30, 2010,” said Jones. “In addition, this substantial core deposit growth has led to our improved net interest margin and increased deposit fee revenue.”

Augmented by the recent stock offering, Banner Corporation and its subsidiary banks continue to maintain capital levels significantly in excess of the requirements to be categorized as “well-capitalized” under applicable regulatory standards. Banner Corporation’s Tier 1 leverage capital to average assets ratio was 13.02% and its total capital to risk-weighted assets ratio was 17.12% at June 30, 2010. Importantly, reflecting the $50 million down-streamed capital investment, Banner Bank’s Tier 1 leverage ratio increased to 10.77% at June 30, 2010.

Tangible stockholders’ equity at June 30, 2010 was $544.1 million, including $118.2 million attributable to preferred stock, compared to $397.1 million a year ago. Tangible book value per common share was $4.15 at quarter-end. At June 30, 2010, Banner had 102.7 million shares outstanding, compared to 18.2 million shares outstanding a year ago. Tangible common stockholders’ equity was $425.9 million at June 30, 2010, or 9.08% of tangible assets, compared to $278.5 million, or 6.09% of tangible assets at March 31, 2010 and $280.4 million, or 6.20% of tangible assets at June 30, 2009.

Conference Call

Banner will host a conference call on Thursday, July 22, 2010, at 8:00 a.m. PDT, to discuss second quarter 2010 results. The conference call can be accessed live by telephone at 480-629-9772 to participate in the call. To listen to the call online, go to the Company’s website at www.bannerbank.com. A replay will be available for a week at (303) 590-3030, using access code 4326727.

About the Company

Banner Corporation is a $4.7 billion bank holding company operating two commercial banks in Washington, Oregon and Idaho. Banner serves the Pacific Northwest region with a full range of deposit services and business, commercial real estate, construction, residential, agricultural and consumer loans. Visit Banner Bank on the Web at www.bannerbank.com.

This press release contains statements that the Company believes are “forward-looking statements.” These statements relate to the Company’s financial condition, results of operations, plans, objectives, future performance or business. You should not place undue reliance on these statements, as they are subject to risks and uncertainties. When considering these forward-looking statements, you should keep in mind these risks and uncertainties, as well as any cautionary statements the Company may make. Moreover, you should treat these statements as speaking only as of the date they are made and based only on information then actually known to the Company. There are a number of important factors that could cause future results to differ materially from historical performance and these forward-looking statements. Factors which could cause actual results to differ materially include, but are not limited to, the credit risks of lending activities, including changes in the level and trend of loan delinquencies and write-offs and changes in our allowance for loan losses and provision for loan losses that may be impacted by deterioration in the housing and commercial real estate markets; changes in general economic conditions, either nationally or in our market areas; changes in the levels of general interest rates and the relative differences between short and long-term interest rates, deposit interest rates, our net interest margin and funding sources; fluctuations in the demand for loans, the number of unsold homes, land and other properties and fluctuations in real estate values in our market areas; secondary market conditions for loans and our ability to sell loans in the secondary market; results of examinations of us by the Board of Governors of the Federal Reserve System and of our bank subsidiaries by the Federal Deposit Insurance Corporation, the Washington State Department of Financial Institutions, Division of Banks or other regulatory authorities, including the possibility that any such regulatory authority may, among other things, institute a formal or informal enforcement action against us or any of the Banks which could require us to increase our reserve for loan losses, write-down assets, change our regulatory capital position or affect our ability to borrow funds or maintain or increase deposits, which could adversely affect our liquidity and earnings; our compliance with regulatory enforcement actions; the requirements and restrictions that have been imposed upon Banner and Banner Bank under the memoranda of understanding with the Federal Reserve Bank of San Francisco (in the case of Banner) and the FDIC and the Washington DFI (in the case of Banner Bank) and the possibility that Banner and Banner Bank will be unable to fully comply with the memoranda of understanding, which could result in the imposition of additional requirements or restrictions; legislative or regulatory changes that adversely affect our business including changes in regulatory policies and principles, or the interpretation of regulatory capital or other rules; our ability to attract and retain deposits; further increases in premiums for deposit insurance; our ability to control operating costs and expenses; the use of estimates in determining fair value of certain of our assets, which estimates may prove to be incorrect or result in significant declines in valuation; staffing fluctuations in response to product demand or the implementation of corporate strategies that affect our workforce and potential associated charges; the failure or security breach of computer systems on which we depend; our ability to retain key members of our senior management team; costs and effects of litigation, including settlements and judgments; our ability to implement our business strategies; our ability to successfully integrate any assets, liabilities, customers, systems, and management personnel we may acquire into our operations and our ability to realize related revenue synergies and cost savings within expected time frames and any goodwill charges related thereto; increased competitive pressures among financial services companies; changes in consumer spending, borrowing and savings habits; the availability of resources to address changes in laws, rules, or regulations or to respond to regulatory actions; our ability to pay dividends on our common and preferred stock and interest or principal payments on our junior subordinated debentures; adverse changes in the securities markets; inability of key third-party providers to perform their obligations to us; changes in accounting policies and practices, as may be adopted by the financial institution regulatory agencies or the Financial Accounting Standards Board including additional guidance and interpretation on accounting issues and details of the implementation of new accounting methods; war or terrorist activities; other economic, competitive, governmental, regulatory, and technological factors affecting our operations, pricing, products and services; future legislative changes in the United States Department of Treasury Troubled Asset Relief Program Capital Purchase Program; and other risks detailed in Banner’s reports filed with the Securities and Exchange Commission, including its Annual Report on Form 10-K for the year ended December 31, 2009. We do not undertake and specifically disclaim any obligation to revise any forward-looking statements to reflect the occurrence of anticipated or unanticipated events or circumstances after the date of such statements. These risks could cause our actual results for 2010 and beyond to differ materially from those expressed in any forward-looking statements by, or on behalf of, us, and could negatively affect our operating and stock price performance.

http://www.bannerbank.com/News/Pages/072110_2Q10_Results.asp…

Antwort auf Beitrag Nr.: 39.888.202 von extremrelaxer am 28.07.10 10:49:39Anmerkung zu der Q2-Präsentation: Die Unterstreichungen habe ich vorgenommen.

Banner scheint seine Hausaufgaben gemacht zu haben, die Umstrukturierung könnte sich in den nächsten quartalen positiv auswirken.

Ich halte die Holding und ihre Banken für einen potentiellen Turnaround-Kandidaten. Die Q2-Zahlen lagen m.E. bereits schon deutlich über den Erwartungen.

Meine Spekulation hier ist, dass sich bei Banner eine ähnliche Turnaround-Story ergeben könnte, wie wir sie ja schon bei anderen an der Insolvenz vorbeigeschrabbten Banken gesehen haben.

Grüsse, ER

Banner scheint seine Hausaufgaben gemacht zu haben, die Umstrukturierung könnte sich in den nächsten quartalen positiv auswirken.

Ich halte die Holding und ihre Banken für einen potentiellen Turnaround-Kandidaten. Die Q2-Zahlen lagen m.E. bereits schon deutlich über den Erwartungen.

Meine Spekulation hier ist, dass sich bei Banner eine ähnliche Turnaround-Story ergeben könnte, wie wir sie ja schon bei anderen an der Insolvenz vorbeigeschrabbten Banken gesehen haben.

Grüsse, ER

Aktueller Chart:

Hier werden sehr viele Charts gezeigt, auf denen man sieht, wie die Aktie auf 8 Dollar steigt und dann wieder fällt. Daraus wird -- es wird nicht dazugesagt, aber man soll es sich scheinbar dazudenken  -- der Schluss gezogen, dass das jederzeit wieder passieren könnte, und der Anstieg der letzten Tage wäre sozusagen der Beginn von sowas.

-- der Schluss gezogen, dass das jederzeit wieder passieren könnte, und der Anstieg der letzten Tage wäre sozusagen der Beginn von sowas.

Hier sieht man mE sehr schön, dass es nicht ausreicht, nur den Chart zu betrachten. Wenn wir diesen Chart hernehmen, gibt es in ihm zwei Perioden: Die Periode vor Ende Juni, wo BANR ca. 18 Millionen Shares ausstehen hatte, und die Periode nach Ende Juni (sieht man an den nun höheren Umsätzen) wo sie über 100 Millionen Shares ausstehen haben.

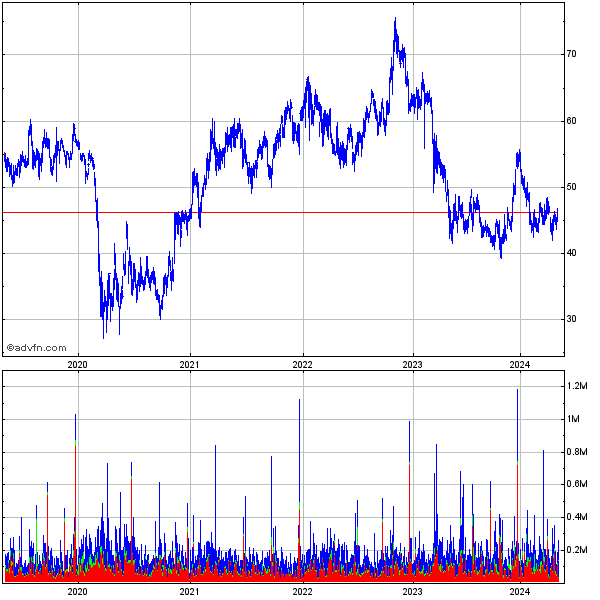

Dieses Unternehmen hat über vier Fünftel seiner gegenwärtig ausstehenden Aktien zu einem Preis von 2 Dollar pro Stück vor einem Monat ausgegeben. Dadurch wurde das Überleben erstmal gesichert, aber andererseits ist schwer argumentierbar, wie sich eine solche viel größere Manövriermasse so dramatisch bewegen soll, wie das vor der Kapitalerhöhung der Fall war, als noch nicht klar war ob die überhaupt eine KE unterbringen. Oder, um es so zu sagen: die aktuelle Marktkapitalisierung ist jetzt bereits deutlich höher als beim Gipfel Ende April.

Mir scheint, dass dieses Papier in der Zukunft deutlich weniger schwanken sollte als zuvor. Die letzten paar Tage ist der ganze Sektor gut gelaufen, deswegen steigt's. Vielleicht steigts auch noch weiter, immerhin liegt der Buchwert bei so 4 in der Gegend. Aber die alten Höhen sind nun unerreichbar geworden. Im Vergleich zu dem in was extremrelaxer sonst so investiert, ein geradezu konservativer Wert.

-- der Schluss gezogen, dass das jederzeit wieder passieren könnte, und der Anstieg der letzten Tage wäre sozusagen der Beginn von sowas.

-- der Schluss gezogen, dass das jederzeit wieder passieren könnte, und der Anstieg der letzten Tage wäre sozusagen der Beginn von sowas.Hier sieht man mE sehr schön, dass es nicht ausreicht, nur den Chart zu betrachten. Wenn wir diesen Chart hernehmen, gibt es in ihm zwei Perioden: Die Periode vor Ende Juni, wo BANR ca. 18 Millionen Shares ausstehen hatte, und die Periode nach Ende Juni (sieht man an den nun höheren Umsätzen) wo sie über 100 Millionen Shares ausstehen haben.

Dieses Unternehmen hat über vier Fünftel seiner gegenwärtig ausstehenden Aktien zu einem Preis von 2 Dollar pro Stück vor einem Monat ausgegeben. Dadurch wurde das Überleben erstmal gesichert, aber andererseits ist schwer argumentierbar, wie sich eine solche viel größere Manövriermasse so dramatisch bewegen soll, wie das vor der Kapitalerhöhung der Fall war, als noch nicht klar war ob die überhaupt eine KE unterbringen. Oder, um es so zu sagen: die aktuelle Marktkapitalisierung ist jetzt bereits deutlich höher als beim Gipfel Ende April.

Mir scheint, dass dieses Papier in der Zukunft deutlich weniger schwanken sollte als zuvor. Die letzten paar Tage ist der ganze Sektor gut gelaufen, deswegen steigt's. Vielleicht steigts auch noch weiter, immerhin liegt der Buchwert bei so 4 in der Gegend. Aber die alten Höhen sind nun unerreichbar geworden. Im Vergleich zu dem in was extremrelaxer sonst so investiert, ein geradezu konservativer Wert.

Antwort auf Beitrag Nr.: 39.888.438 von Pfandbrief am 28.07.10 11:20:21"Im Vergleich zu dem in was extremrelaxer sonst so investiert, ein geradezu konservativer Wert."

Hallo Pfandbrief,

es war abzusehen, dass Du dich hier irgendwann blicken lassen würdest, um warnend einzugreifen! Sei willkommen!

Ein konservativer Wert im Vergleich mit dem, in was ich sonst derzeit investiert bin? Das ist korrekt! YRCW ist da wesentlich spekulativer, ich habe dort aber nach über 100% in denn letzten Tagen bereits Gewinne mitgenommen. Grundsätzlich auch so eine Aktie, die schon sehr nahe an der Insolvenz war und deren niedrige Cash-Bestände noch erhebliches Gefahrenpotential in sich bergen. Und Ambac, da gebe ich Dir auch Recht ist der Inso-Zock schlechthin.

Doch einen wesentlichen Unterschied zu Banner hast Du übersehen: Die Aktie notiert noch auf historisch niedrigem Niveau, bei ca 5% des Wertes in Bezug zum Kurs Dezember 2005 und wurde im Gegensatz zu den anderen Aktien, bei welchen Du als Warner auftritst eben noch nicht gepuscht. Ich finde sie in keinen Börsenbriefchen und ich sehe auch in den US-Boards keine relevante Diskussion zu dieser Aktie. Bei W wurde sie bis gestern noch überhaupt nicht erwähnt oder diskutiert. Wie Du weisst, kann sich so etwas schnell änderen, was dann schnell zu massiven Kursexplosionen führen kann.

wurde sie bis gestern noch überhaupt nicht erwähnt oder diskutiert. Wie Du weisst, kann sich so etwas schnell änderen, was dann schnell zu massiven Kursexplosionen führen kann.

Diese Aktie wurde noch nicht mal angezockt, sie steht lediglich dazu bereit, angezockt zu werden!

LG, ER

Hallo Pfandbrief,

es war abzusehen, dass Du dich hier irgendwann blicken lassen würdest, um warnend einzugreifen!

Sei willkommen! Ein konservativer Wert im Vergleich mit dem, in was ich sonst derzeit investiert bin? Das ist korrekt! YRCW ist da wesentlich spekulativer, ich habe dort aber nach über 100% in denn letzten Tagen bereits Gewinne mitgenommen. Grundsätzlich auch so eine Aktie, die schon sehr nahe an der Insolvenz war und deren niedrige Cash-Bestände noch erhebliches Gefahrenpotential in sich bergen. Und Ambac, da gebe ich Dir auch Recht ist der Inso-Zock schlechthin.

Doch einen wesentlichen Unterschied zu Banner hast Du übersehen: Die Aktie notiert noch auf historisch niedrigem Niveau, bei ca 5% des Wertes in Bezug zum Kurs Dezember 2005 und wurde im Gegensatz zu den anderen Aktien, bei welchen Du als Warner auftritst eben noch nicht gepuscht. Ich finde sie in keinen Börsenbriefchen und ich sehe auch in den US-Boards keine relevante Diskussion zu dieser Aktie. Bei W

wurde sie bis gestern noch überhaupt nicht erwähnt oder diskutiert. Wie Du weisst, kann sich so etwas schnell änderen, was dann schnell zu massiven Kursexplosionen führen kann.

wurde sie bis gestern noch überhaupt nicht erwähnt oder diskutiert. Wie Du weisst, kann sich so etwas schnell änderen, was dann schnell zu massiven Kursexplosionen führen kann.Diese Aktie wurde noch nicht mal angezockt, sie steht lediglich dazu bereit, angezockt zu werden!

LG, ER

Zahlen und Fakten:

Income Statement (Millions)

--------------------------------------------------------------------------------

3/31/2010 12/31/2009 9/30/2009 6/30/2009

Total Revenues(Net Sales) 63.69 63.92 73.00 79.16

Cost of Goods Sold 15.80 17.66 20.82 21.64

Selling & Admin Exps 34.77 32.12 36.63 37.58

Operating Income NA NA NA -24.39

Interest Exp 2.02 2.31 2.40 2.60

Pretax Income -3.54 -7.82 -11.82 -26.99

Other Income NA NA NA NA

Net Income Bef Extraordinary ... NA NA NA NA

Net Income -1.52 -3.54 -6.45 -16.51

Wenn dieser Trend anhält, dann dürfte die Holding bald wieder Gewinne erzeielen!

Income Statement (Millions)

--------------------------------------------------------------------------------

3/31/2010 12/31/2009 9/30/2009 6/30/2009

Total Revenues(Net Sales) 63.69 63.92 73.00 79.16

Cost of Goods Sold 15.80 17.66 20.82 21.64

Selling & Admin Exps 34.77 32.12 36.63 37.58

Operating Income NA NA NA -24.39

Interest Exp 2.02 2.31 2.40 2.60

Pretax Income -3.54 -7.82 -11.82 -26.99

Other Income NA NA NA NA

Net Income Bef Extraordinary ... NA NA NA NA

Net Income -1.52 -3.54 -6.45 -16.51

Wenn dieser Trend anhält, dann dürfte die Holding bald wieder Gewinne erzeielen!

Zahlen und Fakten: EPS

Per Share Overview

--------------------------------------------------------------------------------

Date 12-mos Rolling EPS Dividend P/E Ratio

06/2010 -1.07 0.010 N/E

03/2010 -1.84 0.010 N/E

12/2009 -2.33 0.010 N/E

09/2009 -6.96 0.010 N/E

06/2009 -6.58 0.010 N/E

03/2009 -8.83 0.010 N/E

12/2008 -7.94 0.050 N/E

09/2008 -2.33 0.050 N/E

http://www.nasdaq.com/asp/quotes_reports.asp?mode=&kind=&tim…

Es ist jedem frei gestellt, die Zahlenreihe in die Zukunft fortzuschreiben. Man richt förmlich schon den Break-even!

Per Share Overview

--------------------------------------------------------------------------------

Date 12-mos Rolling EPS Dividend P/E Ratio

06/2010 -1.07 0.010 N/E

03/2010 -1.84 0.010 N/E

12/2009 -2.33 0.010 N/E

09/2009 -6.96 0.010 N/E

06/2009 -6.58 0.010 N/E

03/2009 -8.83 0.010 N/E

12/2008 -7.94 0.050 N/E

09/2008 -2.33 0.050 N/E

http://www.nasdaq.com/asp/quotes_reports.asp?mode=&kind=&tim…

Es ist jedem frei gestellt, die Zahlenreihe in die Zukunft fortzuschreiben. Man richt förmlich schon den Break-even!

Zahlen und Fakten:

Cash Flow Summary (Millions)

--------------------------------------------------------------------------------

Categories 3/31/2010 12/31/2009 9/30/2009 6/30/2009

Net Cash Provided by Operating Activities 25.56 12.87 7.73 19.80

Net Cash Provided by Investing Activities 69.51 35.66 -31.73 -56.44

Net Cash Provided by Financing Activities -140.32 -56.68 270.90 45.38

Operating Activities und Investing Activities zeigen schon einen positiven und steigenden cash-flow an. Nur die Financing Activities führten noch zu einem negativen cash-flow.

Cash Flow Summary (Millions)

--------------------------------------------------------------------------------

Categories 3/31/2010 12/31/2009 9/30/2009 6/30/2009

Net Cash Provided by Operating Activities 25.56 12.87 7.73 19.80

Net Cash Provided by Investing Activities 69.51 35.66 -31.73 -56.44

Net Cash Provided by Financing Activities -140.32 -56.68 270.90 45.38

Operating Activities und Investing Activities zeigen schon einen positiven und steigenden cash-flow an. Nur die Financing Activities führten noch zu einem negativen cash-flow.

Banner Corporation (NASDAQ:BANR) has the 2nd most analyst upgrades in the past four weeks. It was upgraded by 3 brokerage analysts in this period. It is now rated positively by 3 analysts.

http://www.cnanalyst.com/2010/07/top-10-micro-cap-stocks-wit…

http://www.cnanalyst.com/2010/07/top-10-micro-cap-stocks-wit…

Aktuelles Trading-Video: http://www.youtube.com/watch?v=HcWZKx73b5U

warum ist der wert so gafallen ? kannst du etwas auskunft geben ? mein englisch ist nicht gut und kann daher nicht recherchieren

danke

danke

Antwort auf Beitrag Nr.: 39.889.706 von gauner1 am 28.07.10 14:20:30Gauner, wie oft belästigst Du uns jetzt noch mit Deinem ENGLISCH?

Antwort auf Beitrag Nr.: 39.889.220 von extremrelaxer am 28.07.10 13:10:12Gestern gab's in dem Wert die ersten Umsätze in Deutschland (gehandelt nur an der Börse Berlin!) seit Menschengedenken. Schwer zu glauben, dass dafür nicht die Anstrengungen von @extremrelaxer verantwortlich sein sollen.

@ER, Du musst den Jungs aber noch beibringen, dass es nicht so gescheit ist, in Berlin Bestensorders aufzugeben, auch noch ausserhalb der US-Handelszeiten, weil man damit lockere 20 % zu viel zahlt. Das wär eventuell noch wichtiger als sonstige Erwägungen.

@ER, Du musst den Jungs aber noch beibringen, dass es nicht so gescheit ist, in Berlin Bestensorders aufzugeben, auch noch ausserhalb der US-Handelszeiten, weil man damit lockere 20 % zu viel zahlt. Das wär eventuell noch wichtiger als sonstige Erwägungen.

Antwort auf Beitrag Nr.: 39.889.706 von gauner1 am 28.07.10 14:20:30Hallo gauner,

Banner hatte wie andere US-Banken und Banken-Holdings unter der Finazkrise zu leiden. 4 Quartale in Folge kam es zu massiven Verlusten (pro Aktie zwischen 6,58 und 8,83 USD in den Quartalen Q4 2008 bis Q3 2009. Inzwischen hat man umstrukturiert und befindet sich schon wieder kurz vor dem Break even. Da die Aktie aber derzeit noch fast unbeachtet blieb und das sich mit den ersten positiven Quartalsergebnissen schnell ändern könnte, scheint hier m.E. sowohl fundamental als auch charttechnisch hohes Kurspotential vorhanden zu sein.

Grüsse, ER

Banner hatte wie andere US-Banken und Banken-Holdings unter der Finazkrise zu leiden. 4 Quartale in Folge kam es zu massiven Verlusten (pro Aktie zwischen 6,58 und 8,83 USD in den Quartalen Q4 2008 bis Q3 2009. Inzwischen hat man umstrukturiert und befindet sich schon wieder kurz vor dem Break even. Da die Aktie aber derzeit noch fast unbeachtet blieb und das sich mit den ersten positiven Quartalsergebnissen schnell ändern könnte, scheint hier m.E. sowohl fundamental als auch charttechnisch hohes Kurspotential vorhanden zu sein.

Grüsse, ER

Antwort auf Beitrag Nr.: 39.889.790 von Pfandbrief am 28.07.10 14:31:33Hi Pfandbrief,

sorry, ich habe nicht geahnt, dass jemand so etwas machen könnte! Hätte ich das gewußt, dann hätte ich von meinen Shares auch ein paar feilgeboten!

Hätte ich das gewußt, dann hätte ich von meinen Shares auch ein paar feilgeboten!

@ all: Ein Handel in Deutschland ist derzeit definitiv nicht zu nempfehlen! Aufgrund der BID-ASK-Differenz und den Abweichungen vom US-Kurs ist im Falle eines gewünschten Handels nur der US-Markt zu empfehlen (Nasdaq, alternativ NYSE).

sorry, ich habe nicht geahnt, dass jemand so etwas machen könnte!

Hätte ich das gewußt, dann hätte ich von meinen Shares auch ein paar feilgeboten!

Hätte ich das gewußt, dann hätte ich von meinen Shares auch ein paar feilgeboten! @ all: Ein Handel in Deutschland ist derzeit definitiv nicht zu nempfehlen! Aufgrund der BID-ASK-Differenz und den Abweichungen vom US-Kurs ist im Falle eines gewünschten Handels nur der US-Markt zu empfehlen (Nasdaq, alternativ NYSE).

Antwort auf Beitrag Nr.: 39.889.863 von extremrelaxer am 28.07.10 14:40:24Ergänzend: wenn man schon unbedingt in Berlin kaufen muss, was tatsächlich nicht der beste Weg ist, dann muss man ein LIMIT setzen. Man schaut wie es in den USA steht (deswegen ordert man auch in Berlin nur während der US-Handelszeit), rechnet in Euro um, und schlägt 2 % drauf, wenn man geizig ist auch nur 1 %. Der Auftrag wird voraussichtlich nach kurzer Verzögerung ausgeführt werden, da dies bereits ein akzeptabler Arbitragegewinn ist.

Überhaupt sollte man IMMER mit Limit ordern. Aber aus irgendeinem Grund sind die Bestenskäufer (und -verkäufer) in Deutschland nicht totzukriegen.

Überhaupt sollte man IMMER mit Limit ordern. Aber aus irgendeinem Grund sind die Bestenskäufer (und -verkäufer) in Deutschland nicht totzukriegen.

Antwort auf Beitrag Nr.: 39.889.987 von Pfandbrief am 28.07.10 14:54:38Korrekt! Und zur Ergänzung: Bei solchen Aktien mit geringem Handelsvolumen verbietet es sich auch, einen Stop-loss zu setzen, da es ein leichtes ist, einen solchen auszulösen, um billig an Shares zu kommen...

@ Pfandbrief:

Wenn Du schon hier bist, dann würde mich natürlich auch Deine Meinung zu den Zahlen interessieren. Wie interpretierst du die Q2-Zahlen und hälst Du es für möglich, dass wir in Q3 oder Q4 wieder positive EPS sehen?

Gruss, ER

Wenn Du schon hier bist, dann würde mich natürlich auch Deine Meinung zu den Zahlen interessieren. Wie interpretierst du die Q2-Zahlen und hälst Du es für möglich, dass wir in Q3 oder Q4 wieder positive EPS sehen?

Gruss, ER

Antwort auf Beitrag Nr.: 39.890.061 von extremrelaxer am 28.07.10 15:03:36Der 10-Q ist leider noch nicht da (warum eigentlich?). Generell rate ich, bei Banken nicht zu sehr auf bottom-line Quartalszahlen zu glotzen. Das ist letztlich vor allem Ausdruck der aktuellen Bewertungspolitik. Wichtiger ist es, einen Überblick über die generelle Assetqualität zu bekommen. Achte z.B. darauf wie hoch der REO-Bestand ist, das ist bei solchen Instituten, die vorwiegend Hypothekarkredite auf der Bilanz haben immer ein guter Indikator.

Antwort auf Beitrag Nr.: 39.890.103 von Pfandbrief am 28.07.10 15:09:31Hallo extremrelaxer,

ich habe deinen neuen thread über den "Ambac-Thread" beachtet und finde die "Banner-Aktie" sehr interessant.

mich würde interessieren ob du weist warum diese am Jahresanfang so gestiegen und dann gleich wieder auf 2 Dollar gefallen ist. Gabs irgendwelche news?

gruß

flo

ich habe deinen neuen thread über den "Ambac-Thread" beachtet und finde die "Banner-Aktie" sehr interessant.

mich würde interessieren ob du weist warum diese am Jahresanfang so gestiegen und dann gleich wieder auf 2 Dollar gefallen ist. Gabs irgendwelche news?

gruß

flo

Tja....

was tun...??

kaufen....oder nicht kaufen...

was tun...??

kaufen....oder nicht kaufen...

Antwort auf Beitrag Nr.: 39.892.134 von mike211 am 28.07.10 19:46:08@ mike: Hätte die Nasdaq heute mitgespielt, dann wäre sicherlich einiges drin gewesen. Deine Frage kann ich dir nicht beantworten, die entscheidung musst du selber treffen!

Grüsse, ER

Grüsse, ER

Antwort auf Beitrag Nr.: 39.892.642 von extremrelaxer am 28.07.10 21:10:04da gebe ich dir recht...!!!

das habe ich gesehen..das teil war sehr...

oder ist noch sehr stark gegen den trend..!!

DOW voll untergetaucht...da macht sogar eine RDN nen sturtzfug...!!!

"D. Michael Jones, CEO, Mark J. Grescovich, President, and Lloyd W. Baker, CFO, are scheduled to present Wednesday, July 28, 2010, at 11:00 a.m. PDT (2:00 p.m. EDT). The live and archived presentation can be viewed at http://www.kbw.com/news/conferenceCommunity2010_Webcast.html…

habe ich gerade bei yahoo gefunden..kann es nicht wirklich übersetzen..

ich glaube ich kaufe gleich mal 1K könnte was werden

l.g. aus düsseldorf

michael

das habe ich gesehen..das teil war sehr...

oder ist noch sehr stark gegen den trend..!!

DOW voll untergetaucht...da macht sogar eine RDN nen sturtzfug...!!!

"D. Michael Jones, CEO, Mark J. Grescovich, President, and Lloyd W. Baker, CFO, are scheduled to present Wednesday, July 28, 2010, at 11:00 a.m. PDT (2:00 p.m. EDT). The live and archived presentation can be viewed at http://www.kbw.com/news/conferenceCommunity2010_Webcast.html…

habe ich gerade bei yahoo gefunden..kann es nicht wirklich übersetzen..

ich glaube ich kaufe gleich mal 1K könnte was werden

l.g. aus düsseldorf

michael

also ich bin zu 2,35$ drin

Antwort auf Beitrag Nr.: 39.890.103 von Pfandbrief am 28.07.10 15:09:31"..Banner’s real estate owned and repossessed assets totaled $101.7 million at June 30, 2010, compared to $95.2 million three months earlier and $57.2 million a year ago....

..Total assets were $4.70 billion at June 30, 2010, compared to $4.58 billion at the end of the preceding quarter and $4.53 billion a year ago....."

vergleich ich die richtigen zahlen und ist das jetzt viel oder wenig?

P/B und P/C sehen zu vergleichbaren (market cap) banken im saving&loans umfeld auf jeden fall erst mal gut aus..

..Total assets were $4.70 billion at June 30, 2010, compared to $4.58 billion at the end of the preceding quarter and $4.53 billion a year ago....."

vergleich ich die richtigen zahlen und ist das jetzt viel oder wenig?

P/B und P/C sehen zu vergleichbaren (market cap) banken im saving&loans umfeld auf jeden fall erst mal gut aus..

Antwort auf Beitrag Nr.: 39.900.738 von snowdevil am 30.07.10 00:02:22Du vergleichst schon richtig...ich würde es noch nicht besorgniserregend nennen, aber der Trend geht nicht in die richtige Richtung. Es wird halt einiges davon abhängen wie sich der Immobilienmarkt in der nordwestlichen Ecke da weiter entwickelt. Wenn sich in 2, 3 Jahren rausstellt, dass da alles gut wird, ist die Bank heute günstig. Wenn nicht, nicht.

Antwort auf Beitrag Nr.: 39.900.815 von Pfandbrief am 30.07.10 00:57:25Hallo nochmal zusammen,

ich wollte nochmal auf meine Frage zurückkommen. Ich bin bestimmt nicht so gut informiert wie pfandbrief oder extremrelaxer.

aber warum war im frühjahr so ein kursanstieg und dann wieder sofort der absturz auf 2 dollar.

kann mir das jemand erklären?

gruß

flo

ich wollte nochmal auf meine Frage zurückkommen. Ich bin bestimmt nicht so gut informiert wie pfandbrief oder extremrelaxer.

aber warum war im frühjahr so ein kursanstieg und dann wieder sofort der absturz auf 2 dollar.

kann mir das jemand erklären?

gruß

flo

Antwort auf Beitrag Nr.: 39.902.227 von flo83 am 30.07.10 10:56:13Weil extrem verwaessert wurde, aber dass kann dir Pfandbrief wohl besser erklaeren...

Antwort auf Beitrag Nr.: 39.902.227 von flo83 am 30.07.10 10:56:13aber warum war im frühjahr so ein kursanstieg und dann wieder sofort der absturz auf 2 dollar.

Ich habe das damals nicht verfolgt. Meine Vermutung ist folgende: zuerst war hier eingepreist dass die Banken, oder wenigstens eine der Banken, geseizt wird. Dann kamen vermutlich Gerüchte auf, dass ein Geldgeber gefunden ist, der eine Kapitalerhöhung zeichnen würde. Denk daran, damals stand nur ein Fünftel der heutigen Aktienzahl aus, da bewegt sich ein Kurs schnell.

Dann kam die Kapitalerhöhung, aber eben nur zu einem Preis von 2 Dollar pro Aktie. Damit musste der Preis zwangsläufig in die Gegend von 2 zurückfallen.

Es ist durchaus typisch, dass solche "Rettungen" völlig überspekuliert werden. Oft ist die Rettung (z.B. in Form einer Kapitalerhöhung) dann sehr enttäuschend für die Momentumzocker. Wahrscheinlich war es hier ähnlich.