UTS Energy - der Star unter den Ölsandaktien - 500 Beiträge pro Seite

eröffnet am 22.07.05 21:27:11 von

neuester Beitrag 28.01.09 15:52:49 von

neuester Beitrag 28.01.09 15:52:49 von

Beiträge: 176

ID: 995.132

ID: 995.132

Aufrufe heute: 0

Gesamt: 20.632

Gesamt: 20.632

Aktive User: 0

Top-Diskussionen

| Titel | letzter Beitrag | Aufrufe |

|---|---|---|

| vor 28 Minuten | 5673 | |

| vor 20 Minuten | 4609 | |

| vor 32 Minuten | 3870 | |

| vor 1 Stunde | 3321 | |

| vor 1 Stunde | 2383 | |

| heute 14:53 | 1926 | |

| vor 1 Stunde | 1767 | |

| heute 13:07 | 1416 |

Meistdiskutierte Wertpapiere

| Platz | vorher | Wertpapier | Kurs | Perf. % | Anzahl | ||

|---|---|---|---|---|---|---|---|

| 1. | 1. | 18.163,88 | +1,30 | 226 | |||

| 2. | 2. | 1,1300 | -18,12 | 126 | |||

| 3. | 3. | 0,1905 | +0,79 | 105 | |||

| 4. | 5. | 9,3000 | +0,59 | 68 | |||

| 5. | 4. | 168,78 | -0,82 | 56 | |||

| 6. | Neu! | 11,905 | +14,97 | 39 | |||

| 7. | Neu! | 0,4250 | -1,16 | 38 | |||

| 8. | Neu! | 4,7590 | +6,11 | 35 |

Diese Aktie hat bei weiter steigendem Ölpreis ein immenses Potential !

Der Börsenbrief Wealth Daily stellte die Aktie kürzlich vor mit einem berechneten Kurspotential von 533% !

Die obigen Aktien sind:

UTS Energy 1 Mrd. (schwarz)

Canadian Natural Resources 18 Mrd (orange)

Deer Creek Energy (Mk unbek) (braun)

Suncor Energy 18 Mrd. (blau)

Western Oil Sands 3 Mrd. (rot)

Alle diese Aktien laufen durch den steigenden Ölpreis ausgezeichnet, die Königin der Ölsandaktien ist ohne Zweifel UTS Energy, die alleine heute 10,7% zulegen konnten.

Einige Basisinformationen bitte folgendem Thread entnehmen:

http://www.wallstreet-online.de/ws/community/board/threadpag…

Der Börsenbrief Wealth Daily stellte die Aktie kürzlich vor mit einem berechneten Kurspotential von 533% !

Die obigen Aktien sind:

UTS Energy 1 Mrd. (schwarz)

Canadian Natural Resources 18 Mrd (orange)

Deer Creek Energy (Mk unbek) (braun)

Suncor Energy 18 Mrd. (blau)

Western Oil Sands 3 Mrd. (rot)

Alle diese Aktien laufen durch den steigenden Ölpreis ausgezeichnet, die Königin der Ölsandaktien ist ohne Zweifel UTS Energy, die alleine heute 10,7% zulegen konnten.

Einige Basisinformationen bitte folgendem Thread entnehmen:

http://www.wallstreet-online.de/ws/community/board/threadpag…

Tip zum Handel mit der Aktie:

in Berlin-Bremen gehandelt unter WKN 396109, aber mit riesigem Spread von 1,99: 2,43 ! Völlig uninteressant!

in Toronto mit engem Spread sehr liquide gehandelt (3,29/3,30).

Empfehle die Aktie nur in Toronto zu handeln. Die Ausführung dauert z.B. bei Consors nur wenige Sekunden.

in Berlin-Bremen gehandelt unter WKN 396109, aber mit riesigem Spread von 1,99: 2,43 ! Völlig uninteressant!

in Toronto mit engem Spread sehr liquide gehandelt (3,29/3,30).

Empfehle die Aktie nur in Toronto zu handeln. Die Ausführung dauert z.B. bei Consors nur wenige Sekunden.

Auch ich melde mich hiermit für den offiziellen UTS Energy Thread an. Möge unsere Aktie hohe Höhen erklimmen!

Nun gleich zum Börsenplatz Berlin-Bremen. Der Schlusskurs war am Dienstag 3,00/zu 3,01 (bei 3,01 geschlossen). Am folgenden Tag bin ich mit Limit 2,09 hineingegangen und prompt ausgeführt. 2% Aufschlag konnte ich gerade noch verschmerzen, angesichts dem sehr guten heutigen Tage.

Gleich eine Frage an Kostolany: Braucht man um in Toronto zu ordern ein in Canadischen Dollar geführtes Konto bei Consors oder geht das ganz normal mit normalem Euro Konto??

Gruss Punicamelon

Nun gleich zum Börsenplatz Berlin-Bremen. Der Schlusskurs war am Dienstag 3,00/zu 3,01 (bei 3,01 geschlossen). Am folgenden Tag bin ich mit Limit 2,09 hineingegangen und prompt ausgeführt. 2% Aufschlag konnte ich gerade noch verschmerzen, angesichts dem sehr guten heutigen Tage.

Gleich eine Frage an Kostolany: Braucht man um in Toronto zu ordern ein in Canadischen Dollar geführtes Konto bei Consors oder geht das ganz normal mit normalem Euro Konto??

Gruss Punicamelon

Normalerweise geht sowas mit Eurokonto, nur das der Kaufpreis in Kanadischen Dollars verrechnet wird, hier fallen bei Kauf und Verkauf der Aktie also auch noch die Spreads des Währungstausches an. Ich würde der Meinung Kostos unbedingt zustimmen den Börsenplatz Berlin zu meiden.

Ansonsten: ein Hoch auf meinen neuen Burner UTS

Ansonsten: ein Hoch auf meinen neuen Burner UTS

Das Ordern in Kanada über Consors würde ich mir aber vorher mal gut durchrechnen. TOR gehöhrt nicht mehr zu den Welthandelsplätzen, die pauschal abgerechnet werden. Ich habe vor kurzem für einen Kauf i.H.v. 8.400 Can$ Ordergebühren i.H.v. 144 Euro abgedrückt.

79,99 für den Makler in Toronto

49,99 Grundgebühr Consors für Totonto

und nochmal ca. 15,- für eigene Spesen (Consors)

79,99 für den Makler in Toronto

49,99 Grundgebühr Consors für Totonto

und nochmal ca. 15,- für eigene Spesen (Consors)

Trading Spotlight

Hallo Ihr Ölsandprofis,

was haltet Ihr von einer Canwest.

Die Ressourcen die hier vorhanden sein sollen sehen ja prächtig aus und die Aktie ist erst mit ca. 35Mio USD bewertet.

Mich würde mal eine Meinung von einem Experten dazu interessieren.

Danke im vorraus.

was haltet Ihr von einer Canwest.

Die Ressourcen die hier vorhanden sein sollen sehen ja prächtig aus und die Aktie ist erst mit ca. 35Mio USD bewertet.

Mich würde mal eine Meinung von einem Experten dazu interessieren.

Danke im vorraus.

Tach, zumindestens geizen sie nicht mit Infos auf ihren Seiten.

Interessant, aber mehr auch nicht.

Bin ja kein Profi, sondern nur interessierter Amateur;-).

Im Gegensatz zu UTS-Energy sind Canwest in einem weit früheren Stadium. Einige Manager, keine Mitarbeiter, kein Cash, jede Menge Optionen und Visionen.

Visionen von Uranabbau gescheitert bzw. was besseres entdeckt?

Wie sollen diese Projekte finanziert werden?

Profitabel abzubauen?

Management zu schlecht, zu alt?

Mini-Aktie im Gegensatz zu UTS.

UTS hat Finanzierungsfragen schon beantwortet.

Partner nehmen das Projekt ernst (Pedro-Canada).

Bei Canwest stehen noch 1000 Fragen offen, kann man ja in den Sec Filings nachschauen.

Interessant, aber ich kenne die Leute nicht. Sind ja wohl auch nur 3 Personen auf die es ankommt, und der eine wird auf Tagesbasis bezahlt. In einem Büro (2500$p.M.) mit Untermieter (zahlt 1150$p.M.).

Glaube ich kann nicht investieren, weil ich zu wenig Infos kriege. Ist wahrscheinlich zu aufwändig für mich.

Oder weiß jemand mehr?

Also UTS ist ja auch schon heiß mit den ganzen Hoffnungen und Unsicherheiten etc., aber vielleicht in den Griff zu bekommen.

grüße

Interessant, aber mehr auch nicht.

Bin ja kein Profi, sondern nur interessierter Amateur;-).

Im Gegensatz zu UTS-Energy sind Canwest in einem weit früheren Stadium. Einige Manager, keine Mitarbeiter, kein Cash, jede Menge Optionen und Visionen.

Visionen von Uranabbau gescheitert bzw. was besseres entdeckt?

Wie sollen diese Projekte finanziert werden?

Profitabel abzubauen?

Management zu schlecht, zu alt?

Mini-Aktie im Gegensatz zu UTS.

UTS hat Finanzierungsfragen schon beantwortet.

Partner nehmen das Projekt ernst (Pedro-Canada).

Bei Canwest stehen noch 1000 Fragen offen, kann man ja in den Sec Filings nachschauen.

Interessant, aber ich kenne die Leute nicht. Sind ja wohl auch nur 3 Personen auf die es ankommt, und der eine wird auf Tagesbasis bezahlt. In einem Büro (2500$p.M.) mit Untermieter (zahlt 1150$p.M.).

Glaube ich kann nicht investieren, weil ich zu wenig Infos kriege. Ist wahrscheinlich zu aufwändig für mich.

Oder weiß jemand mehr?

Also UTS ist ja auch schon heiß mit den ganzen Hoffnungen und Unsicherheiten etc., aber vielleicht in den Griff zu bekommen.

grüße

[b[5-Tage-Chart von UTS[/b]

Schlußkurs Kanada 3,48

PLUS 6,10% - mehr sog i net

Schlußkurs Kanada 3,48

PLUS 6,10% - mehr sog i net

*Wow, schade, dass ich nicht mehr gekauft habe!

*Uff, das sind jetzt +20% in den letzten 3Handelstagen und der heutige ist noch nicht vorbei. Ich könnte mich wirklich in den Hintern fassen, dass ich nicht mehr gekauft habe. Wirklich ärgerlich. Wenigstens reicht es für 4x Essen gehen.

Gruss Punicamelon

Gruss Punicamelon

4x döner ?

hier kostet nen döner 2,50 euro

hier kostet nen döner 2,50 euro

RTQ 3,71 CAD - PLUS 5%

Punicamelon

Die Rallye ist doch noch längst nicht vorbei. Habe heute auch wieder nachgekauft. Zu anfang 3,53 und jetzt schon 3,71. Das geht noch längere Zeit so weiter, das kann ich dir auch ohne prophetische Gaben versichern.

Punicamelon

Die Rallye ist doch noch längst nicht vorbei. Habe heute auch wieder nachgekauft. Zu anfang 3,53 und jetzt schon 3,71. Das geht noch längere Zeit so weiter, das kann ich dir auch ohne prophetische Gaben versichern.

ANOTHER 52-WEEK HIGH!

My new oil sands giant just made a fresh 52-week high today.

The stock, now trading for $3.40, is up 57% in the Pure Energy portfolio.

I believe the stock is going to $19 a share. And maybe even higher-- as the

company is sitting on $57 billion worth of oil.

Petroleum News said the company `wants to be an oil sands Goliath.` And I agree.

Get my report, The New Oil Sands GIANT!

[aus Wealth Daily von heute)

My new oil sands giant just made a fresh 52-week high today.

The stock, now trading for $3.40, is up 57% in the Pure Energy portfolio.

I believe the stock is going to $19 a share. And maybe even higher-- as the

company is sitting on $57 billion worth of oil.

Petroleum News said the company `wants to be an oil sands Goliath.` And I agree.

Get my report, The New Oil Sands GIANT!

[aus Wealth Daily von heute)

und das wäre die Gegenansicht zu obigem Posting

(kopiert aus einem kanadischen Board)

Nice post Ivan. Though I`ve been trying to keep expectations on this post based in reality, so I have a few things to point out about your estimated valuations. First off, by 2009 they only plan on having a 50k b/d bitumen producing plant. Without upgrading to synthetic crude bitumen sells for about half the value of the value of sweet crude. Company announcements have estimated extraction costs at $30 a barrel (consistent with other oil sands extraction plants). You need roughly $55 oil prices just to break even selling bitumen. And the cost of outsourcing the upgrade from bitumen to synthetic crude isn`t that much better. Basically they will make a very small amount between the time they open their 50k b/d plant and the time they open their 190k b/d plant with an upgrader. A typical 50k b/d plant without an upgrader can be done for their $1B budget making UTS`s share of the costs low; however, the 190k b/d plant with the upgrader will cost them about $5B-$6B. Also, it won`t be until 2016 at best before that 190k b/d plant is actually producing. That gives them 11 more years to pull 40% of $5B (or $2B) out of their azz... or should I say your azz since they will have to get this money by diluting the stock or building debt.

I can’t tell you what will happen in between, but technically the stock will be trading in 2009 based on the estimated valuation of what it will be producing in 2016 and at that point, given current oil prices, it should be trading for $12. If oil goes to $120 per barrel then the stock will be worth $20 in 2016. Going to $100 ever will require a lot of saps.

IMHO

(kopiert aus einem kanadischen Board)

Nice post Ivan. Though I`ve been trying to keep expectations on this post based in reality, so I have a few things to point out about your estimated valuations. First off, by 2009 they only plan on having a 50k b/d bitumen producing plant. Without upgrading to synthetic crude bitumen sells for about half the value of the value of sweet crude. Company announcements have estimated extraction costs at $30 a barrel (consistent with other oil sands extraction plants). You need roughly $55 oil prices just to break even selling bitumen. And the cost of outsourcing the upgrade from bitumen to synthetic crude isn`t that much better. Basically they will make a very small amount between the time they open their 50k b/d plant and the time they open their 190k b/d plant with an upgrader. A typical 50k b/d plant without an upgrader can be done for their $1B budget making UTS`s share of the costs low; however, the 190k b/d plant with the upgrader will cost them about $5B-$6B. Also, it won`t be until 2016 at best before that 190k b/d plant is actually producing. That gives them 11 more years to pull 40% of $5B (or $2B) out of their azz... or should I say your azz since they will have to get this money by diluting the stock or building debt.

I can’t tell you what will happen in between, but technically the stock will be trading in 2009 based on the estimated valuation of what it will be producing in 2016 and at that point, given current oil prices, it should be trading for $12. If oil goes to $120 per barrel then the stock will be worth $20 in 2016. Going to $100 ever will require a lot of saps.

IMHO

I can’t tell you what will happen in between, but technically the stock will be trading in 2009 based on the estimated valuation of what it will be producing in 2016 and at that point, given current oil prices, it should be trading for $12.

In 4 Jahren 300%, damit kann ich leben.

If oil goes to $120 per barrel then the stock will be worth $20 in 2016.

Mal sehn obs nicht schneller auch geht.

Going to $100 ever will require a lot of saps. sap=Trottel

An saps ist an der Börse in aller Regel kein Mangel.

In 4 Jahren 300%, damit kann ich leben.

If oil goes to $120 per barrel then the stock will be worth $20 in 2016.

Mal sehn obs nicht schneller auch geht.

Going to $100 ever will require a lot of saps. sap=Trottel

An saps ist an der Börse in aller Regel kein Mangel.

Im übrigen gibt die Börse selbst die Antwort auf offene Fragen.

heute wieder +0,22 (+6,45%) und Anlauf auf neues ATH.

http://tsx.com/HttpController?GetPage=QuotesViewPage&Detaile…

Was bedeuten denn 4 shares um 15:42 verkauft?

Zwischen RBC und Hampton, zwei Investmentfirmen.

Das geht eine ganze Weile so, mit Mini-Beträgen.

Ansonsten wären natürlich 12$ nicht schlecht.

Warum denn nur 20 bei Ölpreis von 120?

Gruß

Was bedeuten denn 4 shares um 15:42 verkauft?

Zwischen RBC und Hampton, zwei Investmentfirmen.

Das geht eine ganze Weile so, mit Mini-Beträgen.

Ansonsten wären natürlich 12$ nicht schlecht.

Warum denn nur 20 bei Ölpreis von 120?

Gruß

Wird in Toronto heute nicht gehandelt?? Die Charts aktualisieren sich nicht mehr, ausserdem erscheint auf Finanztreff immer noch der Kurs von Freitag.

Nunu?? Was ist denn hier los???

Was ist denn hier los???

Was ist denn hier los???

Was ist denn hier los???

das ist die Antwort auf den heutigen Anstieg:

Deer Creek! Hab ich mir auch vor ein paar Tagen überlegt aber ich finde UTS ein Portion besser.

CALGARY, Aug. 2, 2005 (Canada NewsWire via COMTEX) --

Deer Creek Energy Limited ("Deer Creek") announced today that it has entered into an agreement (the "Agreement") pursuant to which Total E&P Canada Ltd. ("Total"), a wholly owned direct subsidiary of Total S.A., will make an all-cash offer (the "Offer") to acquire all of the issued and outstanding common shares on a fully diluted basis (the "Shares") of Deer Creek by way of a take-over bid. Under the Offer, Total will acquire the Shares at a price of $25.00 per share, valuing the proposed transaction at approximately Cdn. $1.35 billion. The Offer represents a 45% premium to Deer Creek`s shareholders based on the weighted average closing price of Deer Creek`s common shares on the TSX for the 20 previous days ending July 29, 2005 and a 39% premium over Friday`s closing price of $18.00. The Offer will be subject to certain conditions, including acceptance of the Offer by holders of at least 66 2/3% of the outstanding common shares of Deer Creek calculated on a fully diluted basis, and receipt of all required regulatory approvals.

The Board of Directors of Deer Creek has unanimously approved the proposed transaction and has concluded the transaction is in the best interest of its shareholders and will recommend that its shareholders accept the Offer. Goldman, Sachs & Co. and Peters & Co. Limited, acted as financial advisors for Deer Creek and have provided the Board of Directors of Deer Creek with their opinions that the consideration under the Offer is fair from a financial point of view to the holders of Deer Creek common shares.

Deer Creek has agreed to pay Total a non-completion fee of Cdn. $40 million in certain circumstances if the transaction is not completed. The Agreement includes customary non-solicitation covenants. Full details of the Offer will be included in the formal take-over bid circular and related documents, which will be mailed to all shareholders of Deer Creek on or about August 5, 2005 and in any event no later than August 17, 2005. The Offer, unless extended, will expire 35 days thereafter with anticipated closing in September 2005. The directors and certain major shareholders, representing approximately 32.3% of the issued and outstanding shares of Deer Creek on a fully diluted basis, have agreed to tender their shares, subject to certain exceptions, and have entered into lock-up agreements with Total evidencing such commitment.

Deer Creek is a publicly traded, Calgary-based oil sands company engaged in the development of its Athabasca oil sands deposits through SAGD and mining extraction methods. The Company plans to develop the Joslyn Project by way of four phases of SAGD recovery and four phases of oil sands mining recovery, which is designed to produce more than 200,000 barrels of bitumen per day for more than 30 years. Deer Creek has an 84% working interest in and is operator of the Joslyn Project.

Certain statements contained in this document are "forward-looking statements". The projections, estimates and beliefs contained in such forward- looking statements involve known and unknown risks, uncertainties and other factors which may cause actual results or events to differ materially from those anticipated in any forward-looking statements. Deer Creek believes the expectations reflected in those forward-looking statements are reasonable; however Deer Creek cannot provide any assurance that these expectations will prove to be correct.

Deer Creek! Hab ich mir auch vor ein paar Tagen überlegt aber ich finde UTS ein Portion besser.

CALGARY, Aug. 2, 2005 (Canada NewsWire via COMTEX) --

Deer Creek Energy Limited ("Deer Creek") announced today that it has entered into an agreement (the "Agreement") pursuant to which Total E&P Canada Ltd. ("Total"), a wholly owned direct subsidiary of Total S.A., will make an all-cash offer (the "Offer") to acquire all of the issued and outstanding common shares on a fully diluted basis (the "Shares") of Deer Creek by way of a take-over bid. Under the Offer, Total will acquire the Shares at a price of $25.00 per share, valuing the proposed transaction at approximately Cdn. $1.35 billion. The Offer represents a 45% premium to Deer Creek`s shareholders based on the weighted average closing price of Deer Creek`s common shares on the TSX for the 20 previous days ending July 29, 2005 and a 39% premium over Friday`s closing price of $18.00. The Offer will be subject to certain conditions, including acceptance of the Offer by holders of at least 66 2/3% of the outstanding common shares of Deer Creek calculated on a fully diluted basis, and receipt of all required regulatory approvals.

The Board of Directors of Deer Creek has unanimously approved the proposed transaction and has concluded the transaction is in the best interest of its shareholders and will recommend that its shareholders accept the Offer. Goldman, Sachs & Co. and Peters & Co. Limited, acted as financial advisors for Deer Creek and have provided the Board of Directors of Deer Creek with their opinions that the consideration under the Offer is fair from a financial point of view to the holders of Deer Creek common shares.

Deer Creek has agreed to pay Total a non-completion fee of Cdn. $40 million in certain circumstances if the transaction is not completed. The Agreement includes customary non-solicitation covenants. Full details of the Offer will be included in the formal take-over bid circular and related documents, which will be mailed to all shareholders of Deer Creek on or about August 5, 2005 and in any event no later than August 17, 2005. The Offer, unless extended, will expire 35 days thereafter with anticipated closing in September 2005. The directors and certain major shareholders, representing approximately 32.3% of the issued and outstanding shares of Deer Creek on a fully diluted basis, have agreed to tender their shares, subject to certain exceptions, and have entered into lock-up agreements with Total evidencing such commitment.

Deer Creek is a publicly traded, Calgary-based oil sands company engaged in the development of its Athabasca oil sands deposits through SAGD and mining extraction methods. The Company plans to develop the Joslyn Project by way of four phases of SAGD recovery and four phases of oil sands mining recovery, which is designed to produce more than 200,000 barrels of bitumen per day for more than 30 years. Deer Creek has an 84% working interest in and is operator of the Joslyn Project.

Certain statements contained in this document are "forward-looking statements". The projections, estimates and beliefs contained in such forward- looking statements involve known and unknown risks, uncertainties and other factors which may cause actual results or events to differ materially from those anticipated in any forward-looking statements. Deer Creek believes the expectations reflected in those forward-looking statements are reasonable; however Deer Creek cannot provide any assurance that these expectations will prove to be correct.

Neues aus WealthDaily

"Production from the Oil Sands is expected to exceed all OPEC

producers, except for Saudi Arabia, by mid-next decade. This

will make the Oil Sands the third largest oil producer in the

world, after only Saudi Arabia and Russia."

The report highlighted 12 oil sands stocks that`ll experience

significant long-term appreciation.

One of those companies is my #1 oil sands stock for the rest of the

decade.

At just $4 a share, it`s the cheapest of the 12... but has the most

upside potential. My members are already up +93% in the

stock... and I think it`s worth $19 right now!

-Every time oil moves up 50¢ per barrel, the value of the oil in this company`s oil sands

property increases $480 million...

-That`s because the company is sitting on an oil property twice the size of Miami, Florida

and worth more than the entire GDP of the city of San Francisco.

-The $4.00 company just inked a billion dollar deal with one of the largest oil companies in

Canada to get the crude flowing asap.

-Once on-line, it`ll pump 190,000 barrels every single day for 40 years straight!

"Production from the Oil Sands is expected to exceed all OPEC

producers, except for Saudi Arabia, by mid-next decade. This

will make the Oil Sands the third largest oil producer in the

world, after only Saudi Arabia and Russia."

The report highlighted 12 oil sands stocks that`ll experience

significant long-term appreciation.

One of those companies is my #1 oil sands stock for the rest of the

decade.

At just $4 a share, it`s the cheapest of the 12... but has the most

upside potential. My members are already up +93% in the

stock... and I think it`s worth $19 right now!

-Every time oil moves up 50¢ per barrel, the value of the oil in this company`s oil sands

property increases $480 million...

-That`s because the company is sitting on an oil property twice the size of Miami, Florida

and worth more than the entire GDP of the city of San Francisco.

-The $4.00 company just inked a billion dollar deal with one of the largest oil companies in

Canada to get the crude flowing asap.

-Once on-line, it`ll pump 190,000 barrels every single day for 40 years straight!

Auch hier: volle Kraft Vorraus!

Toronto +10,72% auf 4,65CAD (Tageshoch 4,75)

Der 2-Jahres Chart ist wirklich übel!

Toronto +10,72% auf 4,65CAD (Tageshoch 4,75)

Der 2-Jahres Chart ist wirklich übel!

Wer hier nicht kauft, ist einfach selbst Schuld!

Hi Punica

Wieviel hast Du denn heute gekauft.

Geh mal mit gutem Beispiel voran.

Oder suchst Du wen zum abladen?+

Gute Geschäfte

Maulesel

Wieviel hast Du denn heute gekauft.

Geh mal mit gutem Beispiel voran.

Oder suchst Du wen zum abladen?+

Gute Geschäfte

Maulesel

Seit Threaderöffnung sind 18 Tage vergangen und wir sind von 3,30 auf 4,55 (+38%) hochmarschiert - das kann sich wirklich sehen lassen (pro Börsentag 2,7%)

Der Ölpreis ist in derselben Zeit um 9% gestiegen.

Der Hebel auf den Ölpreis war also 4,22

Ganz nett, ich finde immer mehr Gefallen an der Aktie und tausche nach und nach meine lahmeren Krücken in UTS um.

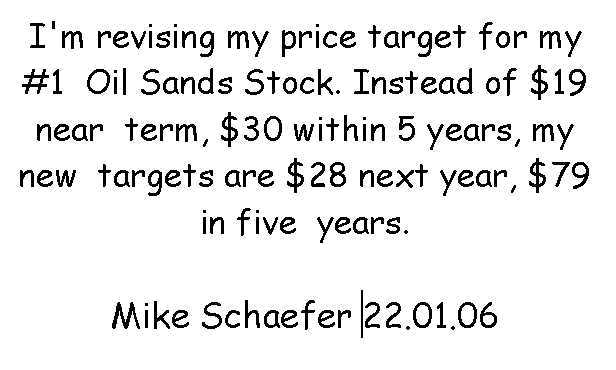

Ich glaube, daß man Mike Schäfers Kursziel von 19 Can-Dollar durchaus bejahen kann.

Das sind vom derzeitigen Kurs aus noch +317% - damit kann ich leben!

Bei gleichen Anstiegs-Verhältnissen wie bisher entspräche das einem Ölpreis von 112 Dollar. Die könnten wir schneller sehen als uns lieb ist.

Der Ölpreis ist in derselben Zeit um 9% gestiegen.

Der Hebel auf den Ölpreis war also 4,22

Ganz nett, ich finde immer mehr Gefallen an der Aktie und tausche nach und nach meine lahmeren Krücken in UTS um.

Ich glaube, daß man Mike Schäfers Kursziel von 19 Can-Dollar durchaus bejahen kann.

Das sind vom derzeitigen Kurs aus noch +317%

- damit kann ich leben! Bei gleichen Anstiegs-Verhältnissen wie bisher entspräche das einem Ölpreis von 112 Dollar. Die könnten wir schneller sehen als uns lieb ist.

UTS läuft super !

Aber Canwest ( CWPC.OB ) läuft zur Zeit einfach noch besser! Schaut euch das Ding unbedingt an! Ist auch ne Ölsand Aktie - ich bin seit ein paar Wochen dabei und kaufe täglich nach.

Aber Canwest ( CWPC.OB ) läuft zur Zeit einfach noch besser! Schaut euch das Ding unbedingt an! Ist auch ne Ölsand Aktie - ich bin seit ein paar Wochen dabei und kaufe täglich nach.

Die Korrektur ist anscheinend beendet !

Derzeit günstiger Einstiegskurs !

(3.90 Can-Dollar)

Hi Jungs

Bin neu hier. Verfolge aber mit großem Interresse die Kommentare über UTS. Gestern sind in Toronto 6,6 Mill Aktien gehandelt worden. Dürfte der Ausverkauf damit beendet sein. ?

Was mich stuzig machtist, daß bei diesen Stückzahlen der Kurs wesentlich mehr steigen müßte. Denn da wo ein Käufer ist, ist auch ein Verkäufer. Was ist eure Meinung. ?

Gruß Sunray

Bin neu hier. Verfolge aber mit großem Interresse die Kommentare über UTS. Gestern sind in Toronto 6,6 Mill Aktien gehandelt worden. Dürfte der Ausverkauf damit beendet sein. ?

Was mich stuzig machtist, daß bei diesen Stückzahlen der Kurs wesentlich mehr steigen müßte. Denn da wo ein Käufer ist, ist auch ein Verkäufer. Was ist eure Meinung. ?

Gruß Sunray

[posting]17.510.551 von relativity am 10.08.05 19:54:42[/posting]@ relativity

Den Mutigen gehört die Welt.

Diese Minis sausen nach oben und unten, mir ist immer noch schwindelig.

Und ob die Ölsande wirklich so nach Osten laufen?

Also ganz schön hot, aber kannst ruhig mal neues posten,

spannend ist es ja.

Lexi

Den Mutigen gehört die Welt.

Diese Minis sausen nach oben und unten, mir ist immer noch schwindelig.

Und ob die Ölsande wirklich so nach Osten laufen?

Also ganz schön hot, aber kannst ruhig mal neues posten,

spannend ist es ja.

Lexi

@sunray

Kostolany4 meint ja schon Korrektur ist vorbei.

Könnte nach Technik so sein.

Aber bei so kleinem Wert ist Technik schwierig. Für mich zumindestens.

Ich wollte bei 3 Can-$ ja nicht rein und abwarten.

War nicht so gut, gebe ich zu,

aber Ausschläge sind ganz schön heftig,

das war ja vorherzusehen. Und das wird auch so bleiben.

Und da fällt mir doch zu oft die Kaffeetasse aus der Hand;-).

UTS verfolgt mich allerdings tagsüber. Muß ich zugeben.

Sieht mir aus den Oderbüchern der Tsx aber schon merkwürdig aus. Sind so Mini-Orders.

Oder muss das so sein?

Lexi

Kostolany4 meint ja schon Korrektur ist vorbei.

Könnte nach Technik so sein.

Aber bei so kleinem Wert ist Technik schwierig. Für mich zumindestens.

Ich wollte bei 3 Can-$ ja nicht rein und abwarten.

War nicht so gut, gebe ich zu,

aber Ausschläge sind ganz schön heftig,

das war ja vorherzusehen. Und das wird auch so bleiben.

Und da fällt mir doch zu oft die Kaffeetasse aus der Hand;-).

UTS verfolgt mich allerdings tagsüber. Muß ich zugeben.

Sieht mir aus den Oderbüchern der Tsx aber schon merkwürdig aus. Sind so Mini-Orders.

Oder muss das so sein?

Lexi

@Sunray

Am Auf und Ab sieht man doch schön, sie die Börse "atmet". Dieselben Leute, die gestern verkauft haben, werden in ein paar Tagen wieder kaufen. Mit dem Hin- und Hertreiben der Kurse macht sich das Big Money ein schönes Zusatzbrot. Es geht dabei ja nicht nur um die Aktien, sondern auch um viele Optionen. Es ist doch kein Zufall, daß am 17.8.05 viele Öl-Optionen auslaufen und ausgerechnet an diesem Tag der Ölpreis heruntermanipuliert wird. Am 19.8.05 ist der 3.Freitag des Monats, ein ebenfalls wichtiger Optionstermin. Vielleicht schaffen es die Big Boys ja noch, den Ölpreis in die Nähe von 60 zu kriegen, damit alle 60-er-Calls verbilligt werden oder verfallen.

Um das Geschäft noch lukrativer zu machen, wurden schon Tage zuvor bei den Ölaktien Gewinne mitgenommen. Man steigt aber dann sehr schnell wieder ein, denn man will ja im Geschäft bleiben.

Bei UTS finde ich Kurse um 3.88 schon wieder einsteigenswert. Klar kann es auch nochmal auf 3.60 gehen oder etwas tiefer. "Am Tief kaufen, am Hoch verkaufen, das können an der Börse nur zwei: der liebe Gott und der Lügner", sagte schon Aktien-Altmeister André Kostolany. .....

So wichtig finde ich die paar Cent unterschied nicht bei einer Aktie mit einem so riesigen Potential. Ich schätze mal, daß ich unter 19 Can-Dollar keine Aktie verkaufen werde. Dazu kommt, daß der Can-Dollar Aufwertungspotential besitzt aufgrund des Rohstoffreichtums und Außenhandelsüberschusses von Kanada.

Am Auf und Ab sieht man doch schön, sie die Börse "atmet". Dieselben Leute, die gestern verkauft haben, werden in ein paar Tagen wieder kaufen. Mit dem Hin- und Hertreiben der Kurse macht sich das Big Money ein schönes Zusatzbrot. Es geht dabei ja nicht nur um die Aktien, sondern auch um viele Optionen. Es ist doch kein Zufall, daß am 17.8.05 viele Öl-Optionen auslaufen und ausgerechnet an diesem Tag der Ölpreis heruntermanipuliert wird. Am 19.8.05 ist der 3.Freitag des Monats, ein ebenfalls wichtiger Optionstermin. Vielleicht schaffen es die Big Boys ja noch, den Ölpreis in die Nähe von 60 zu kriegen, damit alle 60-er-Calls verbilligt werden oder verfallen.

Um das Geschäft noch lukrativer zu machen, wurden schon Tage zuvor bei den Ölaktien Gewinne mitgenommen. Man steigt aber dann sehr schnell wieder ein, denn man will ja im Geschäft bleiben.

Bei UTS finde ich Kurse um 3.88 schon wieder einsteigenswert. Klar kann es auch nochmal auf 3.60 gehen oder etwas tiefer. "Am Tief kaufen, am Hoch verkaufen, das können an der Börse nur zwei: der liebe Gott und der Lügner", sagte schon Aktien-Altmeister André Kostolany. .....

So wichtig finde ich die paar Cent unterschied nicht bei einer Aktie mit einem so riesigen Potential. Ich schätze mal, daß ich unter 19 Can-Dollar keine Aktie verkaufen werde. Dazu kommt, daß der Can-Dollar Aufwertungspotential besitzt aufgrund des Rohstoffreichtums und Außenhandelsüberschusses von Kanada.

Hi Kosti

Danke für deine umfassende Antwort. Wir sind jetzt über 20 %

vom Top entfernt, das ist schon ein Wort. Es sieht wirklich so aus, als sollten die 60 $ erreicht werden. Ich denke ab Montag werde ich langsam Positionen aufbauen, wie hat ein schlauer Broker nach jahrelanger Börsentätigkeit gesagt: Ich weis das ich nichts weis.

Gruß Sunray

Danke für deine umfassende Antwort. Wir sind jetzt über 20 %

vom Top entfernt, das ist schon ein Wort. Es sieht wirklich so aus, als sollten die 60 $ erreicht werden. Ich denke ab Montag werde ich langsam Positionen aufbauen, wie hat ein schlauer Broker nach jahrelanger Börsentätigkeit gesagt: Ich weis das ich nichts weis.

Gruß Sunray

Langsam nimmt UTS wieder an Fahrt auf!

Sorry, hat nichts mit UTS zu tun, aber mit Oel. Wollte keinen eigenen Tread aufmachen ...

Eine interessante Seite mit wöchentlichen Bewertungen von verschiedenen Oelfirmen ist zu finden bei: http://www.mcdep.com.

Ebenfalls interessant zu sein scheint mir der Canadian Oil Sands Trust --> http://www.cos-trust.com/asset/Glossary.aspx

Eine interessante Seite mit wöchentlichen Bewertungen von verschiedenen Oelfirmen ist zu finden bei: http://www.mcdep.com.

Ebenfalls interessant zu sein scheint mir der Canadian Oil Sands Trust --> http://www.cos-trust.com/asset/Glossary.aspx

Mußte mich doch einen Tag eher entschließen einzusteigen

Gruß Sunray

Gruß Sunray

Na mit dem Schwung nach oben will wohl nicht so richtig. Sieht erst danach aus, als sollte die nochmals richtig abtauchen. Sind viele Verkäufer auf der Matte. Kasse machen ist angesagt.

Gruß Sunray

Gruß Sunray

Öl-Aktien sind seit Jahresanfang sehr sehr gut gelaufen. Dementsprechend ist momentan ein wenig die Luft draussen. Der August hat unter dem Strich ca.20% gebracht, das Öl ist um ca.10% gelaufen.

Die kleine Pause sollten wir unserer UTS wirklich redlich gönnen.

Die grosse Frage ist: Konsolidiert UTS mit einem fallenden Ölpreis? Wo steht UTS, wenn wir im Januar beim Öl vielleicht die 45-50$ sehen??

Ich verkaufe UTS in spätestens 4Wochen, das steht fest!

Gruss Punicamelon

Die kleine Pause sollten wir unserer UTS wirklich redlich gönnen.

Die grosse Frage ist: Konsolidiert UTS mit einem fallenden Ölpreis? Wo steht UTS, wenn wir im Januar beim Öl vielleicht die 45-50$ sehen??

Ich verkaufe UTS in spätestens 4Wochen, das steht fest!

Gruss Punicamelon

Hm, Konkurrent CNR läuft wieder richtig gut. Seit wochenanfang fast +20%.

Bei UTS tut sich Nix. 20% seit monatsanfang ist aber okay!

Das ganze Speko-Kapital geht wohl momentan eher nach Norwegen und in die Kaspi Region!

Norske Olijessel, Statoil, Dragon, Transmeridian läuft auch wieder rasant, Petrokasakstan ja sowieso.

Schätze mal, dass es hier auch bald wieder läuft!

Bei UTS tut sich Nix. 20% seit monatsanfang ist aber okay!

Das ganze Speko-Kapital geht wohl momentan eher nach Norwegen und in die Kaspi Region!

Norske Olijessel, Statoil, Dragon, Transmeridian läuft auch wieder rasant, Petrokasakstan ja sowieso.

Schätze mal, dass es hier auch bald wieder läuft!

Hier tanzt die Party!!

http://today.reuters.com/investing/financeArticle.aspx?type=…

Teck Cominco + Petro Canada + UTS

Teck Cominco + Petro Canada + UTS

24.000.000 gehandelte Aktien, daß ist schon ein Wort. Hier sind starke Hände am Werke.

Gruß Sunray

Gruß Sunray

Das ist die Erklärung für den Kurssprung vom Dienstag, 6.9.05.

Hi Kostolany

Schöne Info. Darf man wissen wie du zu dieser Zeitung bzw. Info kommst. ?

Gruß Sunray

Schöne Info. Darf man wissen wie du zu dieser Zeitung bzw. Info kommst. ?

Gruß Sunray

@Sunray01

Das war auf www.wealthdaily.net !

Rechte Maustaste aufs Bild und dann auf Eigenschaften klicken, klärt die Herkunft auf!

Gruss Punicamelon

Das war auf www.wealthdaily.net !

Rechte Maustaste aufs Bild und dann auf Eigenschaften klicken, klärt die Herkunft auf!

Gruss Punicamelon

Danke für die Antwort

Gruß Sunray

Gruß Sunray

UTS Aktionäre erfreuen sich ständig neuer Höchststände, und das trotz aktuell fallender Ölpreise, schon erstaunlich.

Wo geht die Reise hin? Denke mal, langfristig auf 10Euro.

Wo geht UTS kurzfristig hin? Wo geht das Öl hin? Auf seine 58$ Unterstützung? Wird diese geknackt? Ich gehe davon aus,ja. Wo steht UTS dann? *Hm, schwierige Frage. Einerseits ist der Ölsandsektor von guten Ölpreisen abhängig, andererseits ist UTS auf sehr niedrigen Bewertungsniveau. So richtige Unterstützungen gibt es im Chart nicht.

Gruss Punicamelon

Wo geht die Reise hin? Denke mal, langfristig auf 10Euro.

Wo geht UTS kurzfristig hin? Wo geht das Öl hin? Auf seine 58$ Unterstützung? Wird diese geknackt? Ich gehe davon aus,ja. Wo steht UTS dann? *Hm, schwierige Frage. Einerseits ist der Ölsandsektor von guten Ölpreisen abhängig, andererseits ist UTS auf sehr niedrigen Bewertungsniveau. So richtige Unterstützungen gibt es im Chart nicht.

Gruss Punicamelon

Hi Punicamelon ( geht es nicht einfacher )

Das ist richtig mit der Unterstützung. Die Technik ist hier aussen vor. Der Ölpreis ist die alleinige Unterstützung. Alles über 60 $ bewirkt steigende Kurse. Zwischen 55 und 60

gehts seitwärts. Alles unter 55 bringt Stress. Also wie auch immer, Augen auf und hoffen auf den Trend.

Gruß Sunray

Das ist richtig mit der Unterstützung. Die Technik ist hier aussen vor. Der Ölpreis ist die alleinige Unterstützung. Alles über 60 $ bewirkt steigende Kurse. Zwischen 55 und 60

gehts seitwärts. Alles unter 55 bringt Stress. Also wie auch immer, Augen auf und hoffen auf den Trend.

Gruß Sunray

GOLDINVEST-Kolumne: Teck Cominco erwirbt Anteil an Fort Hills Ölsandprojekt

14.09.2005 10:52:00

Ausschnitt:

Nach Abschluss des Geschäfts im Oktober wird Petro-Canada an dem Projekt einen 55 Prozent-Anteil besitzen und 1,55 Mrd. C-Dollar der Projektfinanzierung in Höhe von bis zu 2,5 Mrd. C-Dollar übernehmen, Teck wird 15 Prozent besitzen und 850 Mio. C-Dollar beitragen und UTS wird mit seinem 30 Prozent-Anteil 100 Millionen beitragen.

http://www.finanzen.net/news/news_detail.asp?NewsNr=334594

Petro-C + Teck zahlen den Löwenanteil bei der Projektfinanzierung

14.09.2005 10:52:00

Ausschnitt:

Nach Abschluss des Geschäfts im Oktober wird Petro-Canada an dem Projekt einen 55 Prozent-Anteil besitzen und 1,55 Mrd. C-Dollar der Projektfinanzierung in Höhe von bis zu 2,5 Mrd. C-Dollar übernehmen, Teck wird 15 Prozent besitzen und 850 Mio. C-Dollar beitragen und UTS wird mit seinem 30 Prozent-Anteil 100 Millionen beitragen.

http://www.finanzen.net/news/news_detail.asp?NewsNr=334594

Petro-C + Teck zahlen den Löwenanteil bei der Projektfinanzierung

Neues ATH bei 4,93 (+7,4%)

Angenehmer Nebeneffekt: Der Can.-Dollar steigt auf 0,69 Euro, sodaß der Kurs schon 3,40 Euro entspricht.

Damit schon +70% seit der Erstempfehlung von Mike Schäfer vor 2 Monaten!

Mithalten kann nur noch Canwest Petroleum (rot)

Angenehmer Nebeneffekt: Der Can.-Dollar steigt auf 0,69 Euro, sodaß der Kurs schon 3,40 Euro entspricht.

Damit schon +70% seit der Erstempfehlung von Mike Schäfer vor 2 Monaten!

Mithalten kann nur noch Canwest Petroleum (rot)

@Kotolany4

Ist Canwest nicht etwas winzig im Vergleich.

Sollte man nicht so gegenüberstellen.

Da könnteste ja auch mich mit Dir vergleichen.

Würde meine Wenigkeit auch fürchterlich aufwerten, wäre aber

ungerecht:-).

Grüße

Ist Canwest nicht etwas winzig im Vergleich.

Sollte man nicht so gegenüberstellen.

Da könnteste ja auch mich mit Dir vergleichen.

Würde meine Wenigkeit auch fürchterlich aufwerten, wäre aber

ungerecht:-).

Grüße

Fast 10% Zugewinn auf 5,42 Can-Dollar

Zum Schluß kamen größere Kauforders, Tagesumsatz 9,8 Mio. Stück (etwa das doppelte wie normal)

Auch der Candollar ist heute wieder ein halbes Prozent gestiegen: 1 Candollar = 0,6931 Euro

Kurs in Euro: 3,75

Zum Schluß kamen größere Kauforders, Tagesumsatz 9,8 Mio. Stück (etwa das doppelte wie normal)

Auch der Candollar ist heute wieder ein halbes Prozent gestiegen: 1 Candollar = 0,6931 Euro

Kurs in Euro: 3,75

Supersache, geht doch nach diesm Amibrief auf etwas 20 - 40$ (empohlen bei 4 $)

Hi hasi22

Darf man wissen um welchen Amibrief es sich handelt

Gruß Sunray

Darf man wissen um welchen Amibrief es sich handelt

Gruß Sunray

Durch den Anstieg des Can-Dollar um 1,14% steigt UTS heute auf 4,05 Euro und damit +8% am heutigen Tag.

Die letzten 3 Börsentage zusammen +29,5%

Die letzten 3 Börsentage zusammen +29,5%

Teck Cominco announces acquisition of 15% interest in Fort Hills oil sands project

Tuesday September 6

VANCOUVER, Sept. 6 /CNW/ - Teck Cominco Limited today announced that it has entered into an agreement with UTS Energy Corporation and Petro-Canada to subscribe for a 15% interest in the Fort Hills Energy Limited Partnership (the "Partnership"), which is developing the Fort Hills oil sands project in Alberta, Canada.

ADVERTISEMENT

The aggregate subscription price is $475 million. Teck Cominco will earn a 10% interest in the Partnership by funding $250 million of Petro-Canada and UTS expenditures. In a separate transaction, Teck Cominco will earn a further 5% interest from UTS by funding an additional $225 million of UTS expenditures. On closing of the transactions, expected to occur in October, Teck Cominco will be issued a 15% interest and the interests of UTS and Petro-Canada in the Partnership will be adjusted to 30% and 55%, respectively. The subscription price will be satisfied by Teck Cominco contributing 34% of project expenditures until project spending reaches $2.5 billion and its 15% share thereafter. Closing of the transactions is subject to due diligence, definitive documentation and receipt of regulatory approvals.

Teck Cominco President and CEO Don Lindsay said: "Fort Hills is an ideal opportunity to further diversify our production base in a commodity which will be increasingly important in a world concerned about security of energy supply, and in which Canadians can be expected to play a major role. It is consistent with our strategy of emphasizing the development of quality, long life assets in a variety of significant products in favourable jurisdictions.

Teck Cominco`s proven open pit mining expertise should make a significant contribution to the success of Fort Hills, which will involve mining and extraction as well as upgrading to a final petroleum product. We look forward to working with UTS and project operator Petro-Canada to add value to this project, and view this transaction as the foundation for potential further opportunities in the oil sands business."

Fort Hills, located approximately 90 kilometres north of Fort McMurray, is a long-life asset with 2.8 billion barrels of bitumen resource. Regulatory approvals are in place for up to 190,000 barrels per day of bitumen production, with initial start-up by the end of the decade. Plans include an integrated upgrader. The project partners are currently evaluating the best location for the upgrader and the technology to be employed.

In a separate transaction, UTS has agreed in principle to grant to Teck Cominco the right to acquire at fair market value a 50% working interest in "Lease 14", an oil sands property contiguous to the Fort Hills property. The option would be exercisable following delineation by UTS of the resource on Lease 14 in the event that UTS determines that Lease 14 should be developed as a satellite mine to Fort Hills, subject to agreement of the Partnership.

Tuesday September 6

VANCOUVER, Sept. 6 /CNW/ - Teck Cominco Limited today announced that it has entered into an agreement with UTS Energy Corporation and Petro-Canada to subscribe for a 15% interest in the Fort Hills Energy Limited Partnership (the "Partnership"), which is developing the Fort Hills oil sands project in Alberta, Canada.

ADVERTISEMENT

The aggregate subscription price is $475 million. Teck Cominco will earn a 10% interest in the Partnership by funding $250 million of Petro-Canada and UTS expenditures. In a separate transaction, Teck Cominco will earn a further 5% interest from UTS by funding an additional $225 million of UTS expenditures. On closing of the transactions, expected to occur in October, Teck Cominco will be issued a 15% interest and the interests of UTS and Petro-Canada in the Partnership will be adjusted to 30% and 55%, respectively. The subscription price will be satisfied by Teck Cominco contributing 34% of project expenditures until project spending reaches $2.5 billion and its 15% share thereafter. Closing of the transactions is subject to due diligence, definitive documentation and receipt of regulatory approvals.

Teck Cominco President and CEO Don Lindsay said: "Fort Hills is an ideal opportunity to further diversify our production base in a commodity which will be increasingly important in a world concerned about security of energy supply, and in which Canadians can be expected to play a major role. It is consistent with our strategy of emphasizing the development of quality, long life assets in a variety of significant products in favourable jurisdictions.

Teck Cominco`s proven open pit mining expertise should make a significant contribution to the success of Fort Hills, which will involve mining and extraction as well as upgrading to a final petroleum product. We look forward to working with UTS and project operator Petro-Canada to add value to this project, and view this transaction as the foundation for potential further opportunities in the oil sands business."

Fort Hills, located approximately 90 kilometres north of Fort McMurray, is a long-life asset with 2.8 billion barrels of bitumen resource. Regulatory approvals are in place for up to 190,000 barrels per day of bitumen production, with initial start-up by the end of the decade. Plans include an integrated upgrader. The project partners are currently evaluating the best location for the upgrader and the technology to be employed.

In a separate transaction, UTS has agreed in principle to grant to Teck Cominco the right to acquire at fair market value a 50% working interest in "Lease 14", an oil sands property contiguous to the Fort Hills property. The option would be exercisable following delineation by UTS of the resource on Lease 14 in the event that UTS determines that Lease 14 should be developed as a satellite mine to Fort Hills, subject to agreement of the Partnership.

Kosto , du solltest mit dieser Aktie in diesem Board bleiben- oder TMY kaufen- da kannst du mehr gewinnen!!

@viena

So sehen die Vergleiche über verschiedene Zeiträume aus:

Erst kommt UTS, und dann kommt lang lang nichts.

So sehen die Vergleiche über verschiedene Zeiträume aus:

Erst kommt UTS, und dann kommt lang lang nichts.

Kommt auf deinen Start an- ich bin seit 0,26 USD in TMY drin!

War am 12.05.03....

Gratuliere dir trotzdem zur Performance

Anlagen in Ölsand haben weiterhin hohe Priorität !

Neben UTS, welche momentan ein bisschen korrigieren, auch Canwest Petroleum beachten, diese machten in meinem Depot in 4 Wochen über 60% Gewinn ! (An dieser Stelle ein herzliches Dankeschön an relativity für den Klasse-Tip!

Neben UTS, welche momentan ein bisschen korrigieren, auch Canwest Petroleum beachten, diese machten in meinem Depot in 4 Wochen über 60% Gewinn ! (An dieser Stelle ein herzliches Dankeschön an relativity für den Klasse-Tip!

Ist der Durchhänger bei UTS beendet ?

Eröffnung heute bei 4,81

derzeit 5,23

Can-Dollar erklimmt neues ATH: 1 Can-$ = 0,709 Euro

UTS wird weiter steigen (Kursziel 19 C$)

Can-$ wird weiter steigen.

Weiterhin STRONG BUY

Eröffnung heute bei 4,81

derzeit 5,23

Can-Dollar erklimmt neues ATH: 1 Can-$ = 0,709 Euro

UTS wird weiter steigen (Kursziel 19 C$)

Can-$ wird weiter steigen.

Weiterhin STRONG BUY

News bei UTS Energy:

1. Mike Schaefer erneuert seine Empfehlung:

It`s not too late to jump on this train. I see an energy-based bull market lasting another 7 years at minimal. And I

believe you will get the most bang for your buck with leverage... buying small stocks with huge upside production.

My tiny oil sands stock is an excellent example. It trades for $5.36 a share... yet is sitting on $156 billion worth of oil.

2. UTS heute unverändert bei 5,36, aber der Can-Dollar legte ein weiteres halbes Prozent gegenüber dem Euro zu!

1. Mike Schaefer erneuert seine Empfehlung:

It`s not too late to jump on this train. I see an energy-based bull market lasting another 7 years at minimal. And I

believe you will get the most bang for your buck with leverage... buying small stocks with huge upside production.

My tiny oil sands stock is an excellent example. It trades for $5.36 a share... yet is sitting on $156 billion worth of oil.

2. UTS heute unverändert bei 5,36, aber der Can-Dollar legte ein weiteres halbes Prozent gegenüber dem Euro zu!

***Juhuuuuu,

Ich habe mir geschworen, niemals zu verkaufen. Bei 10-15Euro werde ich vielleicht schwach!

Gruss Punicamelon

Ich habe mir geschworen, niemals zu verkaufen. Bei 10-15Euro werde ich vielleicht schwach!

Gruss Punicamelon

Kann mal jemand die geplanten Produktionraten, Reserven und die MCap reinstellen?

Die 156MD Wert an Reserven scheinen mir etwas zu euphorisch. (Hat man da etwa 3MD Barrel mit den derzeitigen Ölpreis mal genommen )Schätze mal 20 % Brutto-Marge wären Okay. Dann kommt noch hinzu: lange Lebensdauer der Reserven! Das ist natürlich ein Vorteil. Andererseits fallen dann 90 % der Erträge erst in 10 Jahren und später an. D.H. es muss/müsste bei der Bewertung saftig abgezinst werden.

)Schätze mal 20 % Brutto-Marge wären Okay. Dann kommt noch hinzu: lange Lebensdauer der Reserven! Das ist natürlich ein Vorteil. Andererseits fallen dann 90 % der Erträge erst in 10 Jahren und später an. D.H. es muss/müsste bei der Bewertung saftig abgezinst werden.

Die 156MD Wert an Reserven scheinen mir etwas zu euphorisch. (Hat man da etwa 3MD Barrel mit den derzeitigen Ölpreis mal genommen

)Schätze mal 20 % Brutto-Marge wären Okay. Dann kommt noch hinzu: lange Lebensdauer der Reserven! Das ist natürlich ein Vorteil. Andererseits fallen dann 90 % der Erträge erst in 10 Jahren und später an. D.H. es muss/müsste bei der Bewertung saftig abgezinst werden.

)Schätze mal 20 % Brutto-Marge wären Okay. Dann kommt noch hinzu: lange Lebensdauer der Reserven! Das ist natürlich ein Vorteil. Andererseits fallen dann 90 % der Erträge erst in 10 Jahren und später an. D.H. es muss/müsste bei der Bewertung saftig abgezinst werden.

Ok, hab selber mal geschaut.

Die derzeitige MCap liegt bei ca. 2 MD US-$ . Es sind 422 Mio Shares im Umlauf.

Die Reserven betragen 2,8 Md. Barrel. In etwa das was man aufgrund der vorangegangen Beiträge vermuten konnte.

2009 sollen 50.000 Barrel, ab 2010 dann 100.000 Barrel am Tag abgebaut werden. Unterstellt man mal das am Barrel 10 $ (wie bei jetztigen Preisen) verdient werden, würde 2010 ein Gewinn von 350 Mio , also ein KGV von etwa 7 anfallen. Das ist nicht besonders günstig.

Andere Unternehmen haben jetzt schon diese Bewertung, und werden bis zum Jahr 2010 ihre MCap bereits verdient haben.

Die derzeitige MCap liegt bei ca. 2 MD US-$ . Es sind 422 Mio Shares im Umlauf.

Die Reserven betragen 2,8 Md. Barrel. In etwa das was man aufgrund der vorangegangen Beiträge vermuten konnte.

2009 sollen 50.000 Barrel, ab 2010 dann 100.000 Barrel am Tag abgebaut werden. Unterstellt man mal das am Barrel 10 $ (wie bei jetztigen Preisen) verdient werden, würde 2010 ein Gewinn von 350 Mio , also ein KGV von etwa 7 anfallen. Das ist nicht besonders günstig.

Andere Unternehmen haben jetzt schon diese Bewertung, und werden bis zum Jahr 2010 ihre MCap bereits verdient haben.

Genauer gesagt, betragen die Reserven 35% am Fort Hills

Projekt, das 2,8 Mrd. Barrel umfaßt. Hinzu kommen noch

4k Hektar unerschlossenes Land (lease 14).

Das macht ungefähr 2$/barrel.

Suncor und CNR haben ähnliche Relationen, obwohl sie

angesichts ihrer Größe und der bereits laufenden Produktion

mit einem deutlichen Aufschlag gegenüber UTS gehandelt

werden müßten.

Projekt, das 2,8 Mrd. Barrel umfaßt. Hinzu kommen noch

4k Hektar unerschlossenes Land (lease 14).

Das macht ungefähr 2$/barrel.

Suncor und CNR haben ähnliche Relationen, obwohl sie

angesichts ihrer Größe und der bereits laufenden Produktion

mit einem deutlichen Aufschlag gegenüber UTS gehandelt

werden müßten.

Na da wird ja richtig die Luft aus UTS herausgelassen. Mal sehen wie weit es noch abwärts geht.

Gruß Sunray

Gruß Sunray

Was denn für 2$ pro Barrel?

Ich sitze gerade auf der Leitung.

Wenn man ein wenig Pulverdampf von dem momentanen Ölpreishype verzogen ist, dann könnte man wieder nüchterner über UTS nachdenken.

Der KGV von 7 errechnet sich nach 10$ Gewinn pro Barrel,

wenn aber Gewinn höher ist? Wie hoch ist denn Gewinn pro Barrel bei Konkurrenten?

Grüße

Ich sitze gerade auf der Leitung.

Wenn man ein wenig Pulverdampf von dem momentanen Ölpreishype verzogen ist, dann könnte man wieder nüchterner über UTS nachdenken.

Der KGV von 7 errechnet sich nach 10$ Gewinn pro Barrel,

wenn aber Gewinn höher ist? Wie hoch ist denn Gewinn pro Barrel bei Konkurrenten?

Grüße

@Sunray

Der momentane Kurs von 4,67 C$ = 3,25 Euro ist eine Einladung. Nicht nur der Kurs ist 15% zurückgekommen, auch der Can$ steht derzeit etwa 1,5% tiefer.

[posting]18.172.396 von Lexi750 am 07.10.05 00:52:03[/posting]Die Reserven sind schön und gut. Aber diese Sande müssen ausgebaggert werden. Und das dauert. Deshalb ist m.E. die Förderrate wichtiger.

Bei UTS zahle ich für 100.000 Barrel minderweriges Riverbow -Öl im Jahr 2010, das mit 20$ Dicount gehandelt wird, 2 Md. $.

Bei Vaalco zahle ich für 20.000 Barrel hochwertiges Öl, das zu viel niedrigeren Kosten jetzt (!) gefördert wird 200 Mio. Bis ins Jahr 2010 wird Vaalco sein MCap länst verdient haben. Und Wachstumspotential gibts auch hier. Von 5 potentiellen Feldern ist erst eines erschlossen. ich will damit nur sagen, dass UTS nicht sooo übertrieben günstig ist, das sich ein Invest aufzwingt.

Bei UTS zahle ich für 100.000 Barrel minderweriges Riverbow -Öl im Jahr 2010, das mit 20$ Dicount gehandelt wird, 2 Md. $.

Bei Vaalco zahle ich für 20.000 Barrel hochwertiges Öl, das zu viel niedrigeren Kosten jetzt (!) gefördert wird 200 Mio. Bis ins Jahr 2010 wird Vaalco sein MCap länst verdient haben. Und Wachstumspotential gibts auch hier. Von 5 potentiellen Feldern ist erst eines erschlossen. ich will damit nur sagen, dass UTS nicht sooo übertrieben günstig ist, das sich ein Invest aufzwingt.

@Steigerwälder

Deine Rechnung stimmt nicht. Bei UTS bezahlt man für ca. 1 Mrd. Barrel Öl (ausschließlich Ölsände) derzeit 1,67 Mrd. Dollar.

Aus Ölsänden wird ein synthetisches Öl gemacht, das mit WTI-Qualität vergleichbar ist. Jedenfalls steht das so im Geschäftsbericht von CNQ. Wird bei UTS auch so sein.

Gefördert wird zwar erst in Jahren, d.h. UTS ist eine Langfristinvestition mit dem Kursziel 19 Can = 13 Euro.(gestern 3,25 Euro)

Auch für Trader mag sich manche interessante Chance eröffnen. Auf jeden Fall finde ich den Rückgang von 5,97 (Höchstkurs) auf 4,67 (Schlußkurs gestern) ein Geschenk des Himmels an die, die am Anfang nicht dabei waren.

Im Hinterkopf bei allen Ölinvestments muß man sowieso haben, daß nach dem bevorstehenden PEAK OIL eine völlige Neueinschätzung und Neueinpreisung von Öl bevorsteht. (Matt Simmons Prognose 250 Dollar in den nächsten 3-4 Jahren).

Deine Rechnung stimmt nicht. Bei UTS bezahlt man für ca. 1 Mrd. Barrel Öl (ausschließlich Ölsände) derzeit 1,67 Mrd. Dollar.

Aus Ölsänden wird ein synthetisches Öl gemacht, das mit WTI-Qualität vergleichbar ist. Jedenfalls steht das so im Geschäftsbericht von CNQ. Wird bei UTS auch so sein.

Gefördert wird zwar erst in Jahren, d.h. UTS ist eine Langfristinvestition mit dem Kursziel 19 Can = 13 Euro.(gestern 3,25 Euro)

Auch für Trader mag sich manche interessante Chance eröffnen. Auf jeden Fall finde ich den Rückgang von 5,97 (Höchstkurs) auf 4,67 (Schlußkurs gestern) ein Geschenk des Himmels an die, die am Anfang nicht dabei waren.

Im Hinterkopf bei allen Ölinvestments muß man sowieso haben, daß nach dem bevorstehenden PEAK OIL eine völlige Neueinschätzung und Neueinpreisung von Öl bevorsteht. (Matt Simmons Prognose 250 Dollar in den nächsten 3-4 Jahren).

Servus,

ich geb zu ich bin mir nicht 100% tig sicher was die Qualität des Öls betrifft. Aber in der Firmanpresentation auf der Hompage von UTS stand etwas von diesem schweren Billigöl. (Da war ´ne Rechnung mit dieser furchtbaren Riverbow-Pisse von Encana)

Meine "Rechnung" bezog sich auf die Fördermenge. Bei einer Reservenbetrachtung ist UTS ohne Zweifel günstig. Bei einer DCF - Betrachtung ist ein Barrel, das in 50 Jahren gefördert wird aber selbst bei Preisen jenseits der 200$ nichts mehr wert.

Was die 250$ betrifft. Wie du schon sagtest betrifft das alle Ölinvestments. Nicht das du mich falsch verstehst: ich halte UTS für gut interessant und das Baby bleibt auch ganz oben aus der Watchlist. Aber andere Aktien gefallen mir derzeit etwas besser. Sicher ist das letztenendes auch eine Geschmacksfrage. Auf Sicht von 10 Jahren werden wir wahrscheinlich aber beide so oder so nicht drauflegen.

ich geb zu ich bin mir nicht 100% tig sicher was die Qualität des Öls betrifft. Aber in der Firmanpresentation auf der Hompage von UTS stand etwas von diesem schweren Billigöl. (Da war ´ne Rechnung mit dieser furchtbaren Riverbow-Pisse von Encana)

Meine "Rechnung" bezog sich auf die Fördermenge. Bei einer Reservenbetrachtung ist UTS ohne Zweifel günstig. Bei einer DCF - Betrachtung ist ein Barrel, das in 50 Jahren gefördert wird aber selbst bei Preisen jenseits der 200$ nichts mehr wert.

Was die 250$ betrifft. Wie du schon sagtest betrifft das alle Ölinvestments. Nicht das du mich falsch verstehst: ich halte UTS für gut interessant und das Baby bleibt auch ganz oben aus der Watchlist. Aber andere Aktien gefallen mir derzeit etwas besser. Sicher ist das letztenendes auch eine Geschmacksfrage. Auf Sicht von 10 Jahren werden wir wahrscheinlich aber beide so oder so nicht drauflegen.

@steigerwälder: Danke für Antwort. Das Engagement von

Pedrocanada etc. überzeugt mich von Sandqualität.

@kostolany4: Beobachte UTS ja auch, aber mit emotionaler Distanz. Die Jubelschreie machen mich immer skeptisch, und Du hast ja auch über Canwest geschrieben. Die dortige Achterbahn ist nix für mich, UTS ist schon eher mein Kaliber.

Allerdings sitze ich immer noch auf dem Bargeld und prüfe ob ich mich ewig binden soll. Deswegen kommt mir momentaner Rückgang zur weiteren Prüfung sehr entgegen. Wie es so schön heißt, prüfe 50 Firmen, dann findest du 5 Gute.

Davon laufen 1 super, 1 schmiert ab und 3 entwickeln sich ordentlich. UTS ist halt bisher nur auf meiner Liste.

Kritische und intelligente Bemerkungen zu UTS sind mir daher sehr willkommen.

Und Simmons 250$ in 3-4 Jahren wären ein Kriegsgrund.

Wie üblich eine zynische Investgelegenheit, und sehr beängstigend. Glaube ich persönlich jedoch nicht, zumal sich die Riesen (Exxon etc.)mit Investitionen sehr zurückhalten.

Grüße

Pedrocanada etc. überzeugt mich von Sandqualität.

@kostolany4: Beobachte UTS ja auch, aber mit emotionaler Distanz. Die Jubelschreie machen mich immer skeptisch, und Du hast ja auch über Canwest geschrieben. Die dortige Achterbahn ist nix für mich, UTS ist schon eher mein Kaliber.

Allerdings sitze ich immer noch auf dem Bargeld und prüfe ob ich mich ewig binden soll. Deswegen kommt mir momentaner Rückgang zur weiteren Prüfung sehr entgegen. Wie es so schön heißt, prüfe 50 Firmen, dann findest du 5 Gute.

Davon laufen 1 super, 1 schmiert ab und 3 entwickeln sich ordentlich. UTS ist halt bisher nur auf meiner Liste.

Kritische und intelligente Bemerkungen zu UTS sind mir daher sehr willkommen.

Und Simmons 250$ in 3-4 Jahren wären ein Kriegsgrund.

Wie üblich eine zynische Investgelegenheit, und sehr beängstigend. Glaube ich persönlich jedoch nicht, zumal sich die Riesen (Exxon etc.)mit Investitionen sehr zurückhalten.

Grüße

@Lexi

250 Dollar sind ein Kriegsgrund

Korrekt. Ich widerspreche nur insofern, als 250 Dollar 250 Kriegsgründe sind. Die Kriege gegen Iran, Syrien und Venezuela sind längst in Vorbereitung. Sollten jetzt in New York Bomben hochgehen, darf man mit Sicherheit annehmen, daß - wie auch beim 11.9.2001 - der CIA dahintersteckt. Er benutzt und finanziert halt ein paar Islamisten dafür.

@Neue COT-Daten

Die Commercials sind long in Crude gegangen und sind damit auf unserer Seite.

250 Dollar sind ein Kriegsgrund

Korrekt. Ich widerspreche nur insofern, als 250 Dollar 250 Kriegsgründe sind. Die Kriege gegen Iran, Syrien und Venezuela sind längst in Vorbereitung. Sollten jetzt in New York Bomben hochgehen, darf man mit Sicherheit annehmen, daß - wie auch beim 11.9.2001 - der CIA dahintersteckt. Er benutzt und finanziert halt ein paar Islamisten dafür.

@Neue COT-Daten

Die Commercials sind long in Crude gegangen und sind damit auf unserer Seite.

Connacher Oil and Gas Ltd. als Depotergänzung zu UTS? --> http://www.jenningscapital.com/pdfs/CLL09192005InTheWorldsHo…

Irgendwelche Meinungen dazu?

Irgendwelche Meinungen dazu?

Hat jemand von Euch die Namen der 7 Sisters of Natural Gas, die Mike Schaefer in Wealth daily anspricht?

Wäre dankbar für Gas aktien

Danke

Wäre dankbar für Gas aktien

Danke

@ madman

Nein habe ich leider nicht, aber ich habe alle Aktien, welche er im Brief "Pure Energy" verfolgt:

http://finance.yahoo.com/q/cq?d=v1&s=ADB.V+CLL.TO+CNH.TO+CNR…

Gruss HI

Nein habe ich leider nicht, aber ich habe alle Aktien, welche er im Brief "Pure Energy" verfolgt:

http://finance.yahoo.com/q/cq?d=v1&s=ADB.V+CLL.TO+CNH.TO+CNR…

Gruss HI

Die sieben Natural Gas Aktien sind:-

Cinch Energy (CNH)

Crew Energy (CR)

Delphi Energy (DEE)

Diamond Tree Energy (DT)

Galleon Energy (GO.A)

Grey Wolf Exploration (GWE)

Proex Energy (PXE)

Werden alle in Canada gehandelt, Crew und Proex auch in Deutschland.

Cinch Energy (CNH)

Crew Energy (CR)

Delphi Energy (DEE)

Diamond Tree Energy (DT)

Galleon Energy (GO.A)

Grey Wolf Exploration (GWE)

Proex Energy (PXE)

Werden alle in Canada gehandelt, Crew und Proex auch in Deutschland.

Danke an cajsa und happy investor. Ich schau mir das mal an.

Madman

Madman

Von ChangeWave wird folgend AKtie vorgestellt. Um welche Aktie handelt es sich ?? Um UTS natürlich

OUR NEXT HUGE WINNER

We`re buying this stock for our Aggressive Growth portfolio, where we take a little more risk in the search for truly life-changing profits.

Like when we recommended XM Satellite Radio, for example.

In 2002, we made an early call on the ultimate success of satellite radio, as our research showed enormous building demand for the new technology. In fact, I told subscribers that XM Satellite Radio would be "a 10-bagger winner if you keep your cost around $2." I recommended closing out this sale and redeploying the profits on April 2, 2004 - with the stock price at 30 bucks a share.

Now this little-known oil-sands stock could become our next ten-bagger.

I personally plan on holding this stock AT LEAST until 2010. And I expect to keep this investment in my godchildren`s accounts for the next 15 to 25 years.

Why am I excited about this? We are acquiring a 40% stake in an oil-sands field (known as the Fort Hills oil sands development) for a cost of 17 CENTS PER BARREL of light sweet crude.

Add in ALL the cost of mining, extracting, converting and

refining into synthetic crude, and we have production of 190,000 barrels a day for the next 40 YEARS at a cost of less than $10 a barrel.

That makes this company`s share of the Fort Hills project worth BILLIONS. And with a market cap under $500 million, I have not found a more compelling long-term energy play - ever.

The financing is in place. Now it`s simply a question of how well management executes its business plan. Are there risks there? There`s always some risk in investing - but when I weigh it against my expected payoff, there`s no way I can resist this stock.

My model says that when they start producing 200,000 barrels a day, this firm`s stake in Fort Hills is worth about $4 billion. And that will lift the stock price to $12 a share by 2008-2009.

It will cost you around $5 a share now, so you can control a big block with just a modest investment. And if you have any interest, I urge you to get in now. We`re at the "tipping point" for this company - the time when long-laid plans start reaching fruition - and the stock has already made its initial move up.

Buy it now and hang on for a long, enjoyable ride.

OUR NEXT HUGE WINNER

We`re buying this stock for our Aggressive Growth portfolio, where we take a little more risk in the search for truly life-changing profits.

Like when we recommended XM Satellite Radio, for example.

In 2002, we made an early call on the ultimate success of satellite radio, as our research showed enormous building demand for the new technology. In fact, I told subscribers that XM Satellite Radio would be "a 10-bagger winner if you keep your cost around $2." I recommended closing out this sale and redeploying the profits on April 2, 2004 - with the stock price at 30 bucks a share.

Now this little-known oil-sands stock could become our next ten-bagger.

I personally plan on holding this stock AT LEAST until 2010. And I expect to keep this investment in my godchildren`s accounts for the next 15 to 25 years.

Why am I excited about this? We are acquiring a 40% stake in an oil-sands field (known as the Fort Hills oil sands development) for a cost of 17 CENTS PER BARREL of light sweet crude.

Add in ALL the cost of mining, extracting, converting and

refining into synthetic crude, and we have production of 190,000 barrels a day for the next 40 YEARS at a cost of less than $10 a barrel.

That makes this company`s share of the Fort Hills project worth BILLIONS. And with a market cap under $500 million, I have not found a more compelling long-term energy play - ever.

The financing is in place. Now it`s simply a question of how well management executes its business plan. Are there risks there? There`s always some risk in investing - but when I weigh it against my expected payoff, there`s no way I can resist this stock.

My model says that when they start producing 200,000 barrels a day, this firm`s stake in Fort Hills is worth about $4 billion. And that will lift the stock price to $12 a share by 2008-2009.

It will cost you around $5 a share now, so you can control a big block with just a modest investment. And if you have any interest, I urge you to get in now. We`re at the "tipping point" for this company - the time when long-laid plans start reaching fruition - and the stock has already made its initial move up.

Buy it now and hang on for a long, enjoyable ride.

Für 4.40 Candollar bekommt man diese Aktie bestimmt so schnell nicht wieder !

MORE NEW ENERGY PLAYS

Dear WaveRiders,

The pullback in energy stocks is giving us more opportunities to beef up our portfolio, and I have some new ideas for your ChangeWave Investing portfolio today in coal and the Canadian tar sands.

NEW COAL PLAY: ALPHA NATURAL RESOURCES (ANR)

Coal demand from utilities has never been higher -- and with natural gas prices staying above $10, the plants that can use coal, will. Especially the low-sulfur variety.

This is the niche of Alpha Natural Resources (ANR), the leader in producing high-quality Appalachian coal.

Alpha has 64 mines with 500 million tons of proven and probable reserves, worth about $30 billion at current coal prices. Approximately 94% of the company`s reserve base is high-BTU coal and 89% is low-sulfur, qualities that are in high demand among electric utilities that use steam coal.

Alpha is also one of the nation`s largest producers and exportersof metallurgical coal (met coal), a key ingredient in steelmanufacturing.

You know how well we`ve done with Fording Canadian Coal (FDG) andits metallurgical coal, and ANR gives us another play on this rare variety.

Recently, ANR has been a victim of Hurricane Katrina because they had to delay shipping of met coal down the Mississippi to foreign buyers. This hurt Q3 sales, but those sales were not cancelled and they will be delivered in Q4.

But the company continues to look ahead with the acquisition of the privately held Nicewonder coal group. The acquisition raises production by about 20% in 2006 and EPS around 12%-15%, while giving them access to more low-sulfur coal as well as untapped reserves on 28,000 acres.

Alpha expects the Nicewonder properties, which are scattered across Virginia and West Virginia, to be accretive to earnings and significantly boost its operating results and free cash flow generation going forward.

The purchase agreements call for Alpha subsidiaries to issue Nicewonder affiliates $60 million of Alpha common stock and pay $256.2 million in cash and seller notes. Alpha plans to finance the cash portion of the purchase through $500 million of new senior-secured credit facilities.

KATRINA`S INFLUENCE ON Q3

Alpha is on target to meet its guidance for the quarter, but damage from Hurricane Katrina has delayed some of the exports of its met coal products, so shipments worth about $35 million will be delayed from the Gulf. Revenue forecasts are still on target for $1.3 billion to $1.6 billion for the year and do not include any anticipated contribution from the Nicewonder coal group.

The only other problems facing Alpha are some operations that were running behind plan because of a labor strike in some contractor-operated mines. This forced ANR to purchase coal at a higher cost than planned so the company could meet commitments to its customers.

Bottom line, problems in Q3 are NOT of the recurring variety, and cash flow per share looks to grow another 20% next year. That ultimately makes ANR a $35 stock this time next year.

My earnings estimate for 2006, including new acquisitions, is about $3 per share for 2006 and $4 in 2007. Tight coal supplies and rising prices should provide Alpha with strong cash flow, revenues and earnings growth -- and a $40 price by the end of 2006.

Buy Alpha Natural Resources at or under $27.50 for your Ballast Growth portfolio.

CANADIAN OIL SANDS

While we have been racking up significant gains in the Canadian oil sands stocks during the past year, the ride may just be beginning.

According to a recent report by Raymond James, "The best time to buy an oil sands company was five years ago, the second best time is today." The report is aptly titled: The Oil Sands of Canada -- The World Wakes Up: First to Peak Oil, Second to the Oil Sands of Canada.

Raymond James makes the point that the "low-hanging fruit" of global oil reserves have been picked. To find new, substantial reserves, producers often have to deal with extreme conditions, like drilling in ultra-deep water, the severe High Arctic, or in politically unstable areas.

Well, let me tell ya -- Venezuela, Russia and the Caspian Sea are FAR less attractive than Alberta. Furthermore, the governments in the first two seem increasingly intent on helping out the Chinese at the expense of the west, and in the third case, ownership of the deposit is hotly contested.

The report concludes that, "every investor should be exposed to the oil sands sector in a significant way because it provides growth from a known resource at a time when global oil production is getting more difficult to add, and demand continues to increase. Moreover, the oil sands resource is economic to develop and it occurs in a politically-stable country that happens to be next door to the largest energy consumer in the world."

HOW WE PLAY THIS

We recommended Suncor in the mid-$20s, and sold it at $52. We continue to recommend UTS Energy (UTS.TO), having purchased it for around $2, and watched it climb to $5.

I think the best is yet to come, and here`s why.

The big players in the Athabasca tar sands (i.e., Exxon, BP, PetroCanada, etc.) have been lobbying the SEC to expand the definition of oil sands reserves, and a favorable decision appears imminent.

From a pure reserve standpoint, only a tiny fraction of oil sands assets can currently be booked as reserves -- this is another insane lag in the energy accounting rules.

Given the power of the lobbying, my guess is these arcane and obsolete reserve rules will be thrown out next year -- and those of us who own tar sands reserves will see a windfall of valuation expansion.

Which brings us to Connacher Oil and Gas (CLL.TO)

I can make a strong case that we get an even better value owning Connacher at current prices.

CONTRAST AND COMPARE

The market is currently valuing UTS Energy (UTS.TO) at about $1.75 billion (Canadian). UTS`s 40% share of the Fort Hills project gives them control of 1.12 billion barrels of recoverable oil reserves.

Said another way, investors own about 2.62 barrels of oil per share.

With the recent $75 million (Canadian) financing included, Connacher is valued at about $280 million (Canadian) by the market. As it stands now, the company controls recoverable reserves of 311 million barrels of oil, equating to about 2.33 barrels per share.

With Connacher, you get 2.33 barrels per share vs. UTS Energy`s 2.62 barrels per share -- but at a much, much lower valuation.

The potential for reserve growth at CLL`s Great Divide property remains significant and reserves could prove to be a multiple of the present figure. But the upside for CLL is that they do NOT have to take on a partner to handle extraction infrastructure.

CLL should be extracting more than 10,000 BOE/day by the fourth quarter of next year. At $50-plus oil, the company could well see cash flow over $1 (Canadian) per share.

On that basis alone, Connacher could easily be valued at twice the current share price.

Bear in mind we have to wait until mid-2009 to see any production from UTS and its partners.

Another key difference here is that while UTS is essentially in the earthmoving business, CLL will be using steam-assisted gravity drainage (SAGD) technology to extract bitumen from the tar sands.

SAGD is a proven technology that involves drilling horizontal wells and constructing a processing facility that separates oil and water, generates steam and recycles water.

It`s a cheaper and quicker method of extracting oil. As a result of Great Divide`s amenability to SAGD, CLL doesn`t need to take on a partner and give away 60% of its project, nor does it need a 5-year construction period in a rising cost environment.

Buy under $2.50.

Dear WaveRiders,

The pullback in energy stocks is giving us more opportunities to beef up our portfolio, and I have some new ideas for your ChangeWave Investing portfolio today in coal and the Canadian tar sands.

NEW COAL PLAY: ALPHA NATURAL RESOURCES (ANR)

Coal demand from utilities has never been higher -- and with natural gas prices staying above $10, the plants that can use coal, will. Especially the low-sulfur variety.

This is the niche of Alpha Natural Resources (ANR), the leader in producing high-quality Appalachian coal.

Alpha has 64 mines with 500 million tons of proven and probable reserves, worth about $30 billion at current coal prices. Approximately 94% of the company`s reserve base is high-BTU coal and 89% is low-sulfur, qualities that are in high demand among electric utilities that use steam coal.

Alpha is also one of the nation`s largest producers and exportersof metallurgical coal (met coal), a key ingredient in steelmanufacturing.

You know how well we`ve done with Fording Canadian Coal (FDG) andits metallurgical coal, and ANR gives us another play on this rare variety.

Recently, ANR has been a victim of Hurricane Katrina because they had to delay shipping of met coal down the Mississippi to foreign buyers. This hurt Q3 sales, but those sales were not cancelled and they will be delivered in Q4.

But the company continues to look ahead with the acquisition of the privately held Nicewonder coal group. The acquisition raises production by about 20% in 2006 and EPS around 12%-15%, while giving them access to more low-sulfur coal as well as untapped reserves on 28,000 acres.

Alpha expects the Nicewonder properties, which are scattered across Virginia and West Virginia, to be accretive to earnings and significantly boost its operating results and free cash flow generation going forward.

The purchase agreements call for Alpha subsidiaries to issue Nicewonder affiliates $60 million of Alpha common stock and pay $256.2 million in cash and seller notes. Alpha plans to finance the cash portion of the purchase through $500 million of new senior-secured credit facilities.

KATRINA`S INFLUENCE ON Q3