Der Uran-Bullenmarkt geht weiter : ein kanadisches Musterportfolio - 500 Beiträge pro Seite

eröffnet am 21.06.09 13:55:17 von

neuester Beitrag 15.12.09 22:13:29 von

neuester Beitrag 15.12.09 22:13:29 von

Beiträge: 80

ID: 1.151.259

ID: 1.151.259

Aufrufe heute: 0

Gesamt: 14.218

Gesamt: 14.218

Aktive User: 0

Top-Diskussionen

| Titel | letzter Beitrag | Aufrufe |

|---|---|---|

| vor 51 Minuten | 3378 | |

| heute 12:26 | 3169 | |

| vor 31 Minuten | 3084 | |

| heute 12:06 | 1518 | |

| heute 07:52 | 1287 | |

| vor 32 Minuten | 1252 | |

| heute 13:04 | 1243 | |

| vor 1 Stunde | 1238 |

Meistdiskutierte Wertpapiere

| Platz | vorher | Wertpapier | Kurs | Perf. % | Anzahl | ||

|---|---|---|---|---|---|---|---|

| 1. | 1. | 18.687,12 | -0,31 | 97 | |||

| 2. | 3. | 160,60 | -0,02 | 51 | |||

| 3. | 5. | 6,3800 | -1,51 | 35 | |||

| 4. | 10. | 10,140 | -5,94 | 35 | |||

| 5. | 7. | 13,250 | +1,55 | 28 | |||

| 6. | 2. | 2.428,29 | +0,09 | 27 | |||

| 7. | 4. | 31,81 | -0,06 | 24 | |||

| 8. | 11. | 5,5720 | -2,11 | 24 |

10 Uran-Aktien für den kommende Fortsetzung des Uran-Bullen-Markts

Ich glaube, dass nach dem starken Anstieg des Uran-Preises vor zwei Jahren und dem anschließenden tiefen Fall mit dem Finale der Finanzkrise nun der nächste Schritt im Uran-Bullen-Markt ansteht.

Hier mal der Chart für den Spot-Preis von Uran über die letzten 2 Jahre (Peak knapp unter $ 140, Low $ 40, Aktuell $ 53) :

Zur Recherche über den Uranmarkt empfehle ich:

1. Seite von UXC : http://www.uxc.com/index.aspx

2. Spot-Preis Chart: http://www.uxc.com/review/uxc_Prices.aspx

3. Seite von Uranium Investing News: http://www.uraniuminvestingnews.com/

(re-load Knopf für Überspringen der Werbung drücken)

4. Seite von Uraniumletter International: http://goldletterint.com/uraniumletter.php

Und zu dem nächsten "Frühling" im Uran-Bullen-Markt folgende Artikel:

http://www.uraniuminvestingnews.com/1675/dawn-of-a-new-urani…

http://www.uraniuminvestingnews.com/1736/uranium-spot-price-…

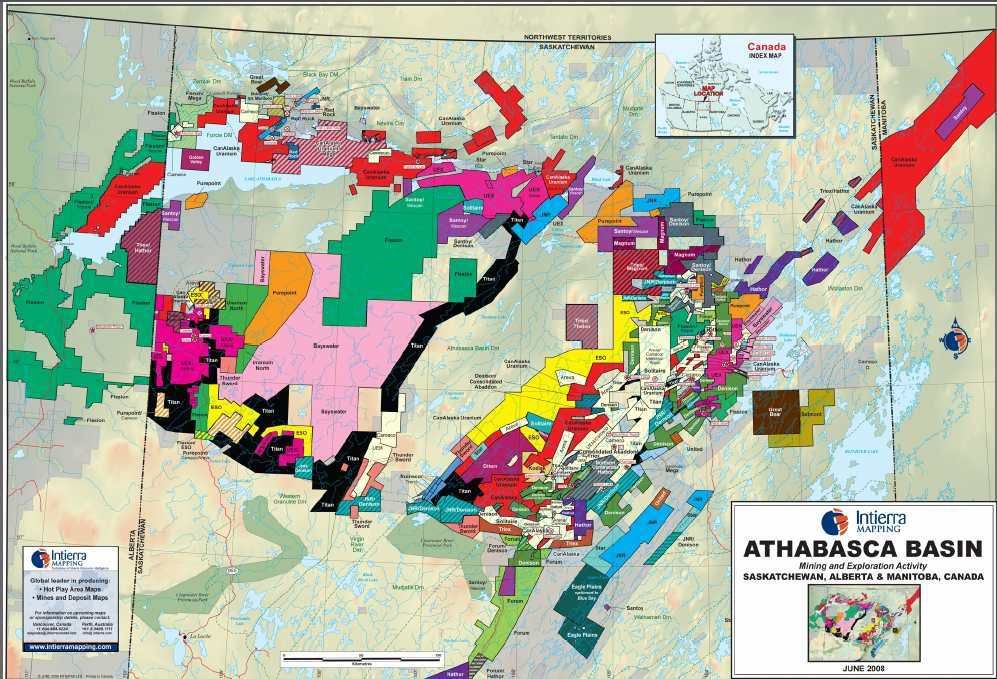

Mein Muster-Portfolio habe ich hauptsächlich aus Explorern und einem Produzenten in Kanada und hier aus dem Athabasca Becken zusammengestellt. (Zum Uranexploration im Athabasca Becken bald mehr hier in diesem Thread).

Denn mein "Wahlspruch" lautet : "GRADE IS KING" !

Warum ?

- Niedrigere Abbaukosten pro Pfund Uran,

- selbst kleinere Deposits sind wirtschaftlich,

- bessere Unterstützung für den Kurs eines Explorers, da sein hochgradiger Fund gerade bei niedrigen Uranpreisen noch wirtschaftlich ist,

- größeres Übernahmeinteresse durch einen Major !

"Size doesn´t matter" - dieser Spruch gilt insbesondere für die Exploration im Athabasca Becken. Denn auch, wenn ein Fund nicht gleich ein riesiges Deposit wird, hilft häufig die hohe Urankonzentration (die im hochgradigen Bereich bis zu 100 Mal höher ist als irgendwo anders auf der Welt), um immer noch ein ökonomisch abbaubares Vorkommen zu erhalten.

Wenn dann allerdings noch die Tonnage dazukommt (großer mineralisierter Erzkörper), hat man einen wahren "Elefanten" "am Haken" ! Und diese Chance ist für jeden Explorer im Athabasca Becken halt höher als irgendwo anders auf der Welt !

Im Athabasca Becken sind bis jetzt die weltweit meisten höchstgradigen Uranfunde gemacht worden.

Wir sprechen hier von höchstgradig mit zweistelligen Prozentzahlen, also > 10% U3O8 im Bohrkern und nicht, wie in vielen anderen Gebieten der Welt mit nur einer Stelle, nämlich der 0, VOR dem Komma !

Erdkruste: 0,0002% Uran (= 2 ppm , parts per million)

Low-grade deposit : 0,1% Uran (= 1000 ppm)

High-grade deposit: > 2% Uran (= 20000 ppm)

Super-High-grade deposit: > 20% Uran (= 200000 ppm) ,

Gerade Letzteres ist meines Wissens nur im Athabasca Becken zu finden, da kann Namibia, Australien und die USA nur von Träumen.

Hier ist vor allem die in den 80´er Jahren entdeckte McArthur River Mine zu nennen, die weltweit größte, höchstgradigste Uranmine mit 437 Mio. Pfund Uran (801.000 Tonnen mit einem DURCHSCHNITTLICHEN Urangehalt von 25% !!!).

Wie oben schon erwähnt, spielt Größe des Deposits in Athabasca nur eine untergeordnete Rolle bei diesen Urangehalten. Bei McArthur River muß man sich vor Augen führen, daß ein Großteil des Deposits in einem Erzkörper 500 Meter unter der Oberfläche mit einer Ausdehnung von NUR 70 Meter Länge, 30 Meter Breite und 70 Meter Tiefe gebildet wird !

FANTOMAS

Ich glaube, dass nach dem starken Anstieg des Uran-Preises vor zwei Jahren und dem anschließenden tiefen Fall mit dem Finale der Finanzkrise nun der nächste Schritt im Uran-Bullen-Markt ansteht.

Hier mal der Chart für den Spot-Preis von Uran über die letzten 2 Jahre (Peak knapp unter $ 140, Low $ 40, Aktuell $ 53) :

Zur Recherche über den Uranmarkt empfehle ich:

1. Seite von UXC : http://www.uxc.com/index.aspx

2. Spot-Preis Chart: http://www.uxc.com/review/uxc_Prices.aspx

3. Seite von Uranium Investing News: http://www.uraniuminvestingnews.com/

(re-load Knopf für Überspringen der Werbung drücken)

4. Seite von Uraniumletter International: http://goldletterint.com/uraniumletter.php

Und zu dem nächsten "Frühling" im Uran-Bullen-Markt folgende Artikel:

http://www.uraniuminvestingnews.com/1675/dawn-of-a-new-urani…

http://www.uraniuminvestingnews.com/1736/uranium-spot-price-…

Mein Muster-Portfolio habe ich hauptsächlich aus Explorern und einem Produzenten in Kanada und hier aus dem Athabasca Becken zusammengestellt. (Zum Uranexploration im Athabasca Becken bald mehr hier in diesem Thread).

Denn mein "Wahlspruch" lautet : "GRADE IS KING" !

Warum ?

- Niedrigere Abbaukosten pro Pfund Uran,

- selbst kleinere Deposits sind wirtschaftlich,

- bessere Unterstützung für den Kurs eines Explorers, da sein hochgradiger Fund gerade bei niedrigen Uranpreisen noch wirtschaftlich ist,

- größeres Übernahmeinteresse durch einen Major !

"Size doesn´t matter" - dieser Spruch gilt insbesondere für die Exploration im Athabasca Becken. Denn auch, wenn ein Fund nicht gleich ein riesiges Deposit wird, hilft häufig die hohe Urankonzentration (die im hochgradigen Bereich bis zu 100 Mal höher ist als irgendwo anders auf der Welt), um immer noch ein ökonomisch abbaubares Vorkommen zu erhalten.

Wenn dann allerdings noch die Tonnage dazukommt (großer mineralisierter Erzkörper), hat man einen wahren "Elefanten" "am Haken" ! Und diese Chance ist für jeden Explorer im Athabasca Becken halt höher als irgendwo anders auf der Welt !

Im Athabasca Becken sind bis jetzt die weltweit meisten höchstgradigen Uranfunde gemacht worden.

Wir sprechen hier von höchstgradig mit zweistelligen Prozentzahlen, also > 10% U3O8 im Bohrkern und nicht, wie in vielen anderen Gebieten der Welt mit nur einer Stelle, nämlich der 0, VOR dem Komma !

Erdkruste: 0,0002% Uran (= 2 ppm , parts per million)

Low-grade deposit : 0,1% Uran (= 1000 ppm)

High-grade deposit: > 2% Uran (= 20000 ppm)

Super-High-grade deposit: > 20% Uran (= 200000 ppm) ,

Gerade Letzteres ist meines Wissens nur im Athabasca Becken zu finden, da kann Namibia, Australien und die USA nur von Träumen.

Hier ist vor allem die in den 80´er Jahren entdeckte McArthur River Mine zu nennen, die weltweit größte, höchstgradigste Uranmine mit 437 Mio. Pfund Uran (801.000 Tonnen mit einem DURCHSCHNITTLICHEN Urangehalt von 25% !!!).

Wie oben schon erwähnt, spielt Größe des Deposits in Athabasca nur eine untergeordnete Rolle bei diesen Urangehalten. Bei McArthur River muß man sich vor Augen führen, daß ein Großteil des Deposits in einem Erzkörper 500 Meter unter der Oberfläche mit einer Ausdehnung von NUR 70 Meter Länge, 30 Meter Breite und 70 Meter Tiefe gebildet wird !

FANTOMAS

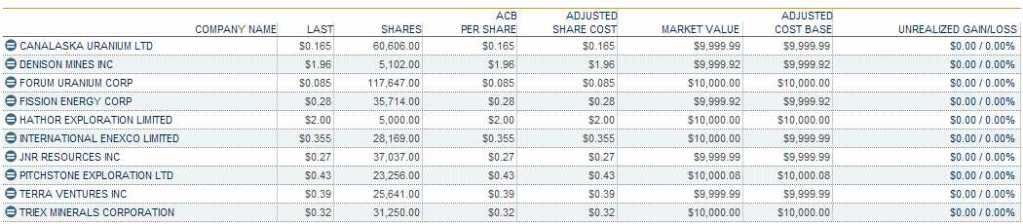

Das Muster-Portfolio:

1. Denison Mines (DML.TO)

2. Hathor Exploration (HAT.V)

3. JNR Resources (JNN.V)

4. CanAlaska Uranium (CVV.V)

5. Terra Ventures (TAS.V)

6. Pitchstone Exploration (PXP.V)

7. Fission Energy (FIS.V)

8. Int. Enexco (IEC.V)

9. Forum Uranium (FDC.V)

10. Triex Minerals (TXM.V)

(Die Reihenfolge ist nach aktueller Marktkapitalisierung zusammengestellt und soll keine Wertung darstellen)

Hier eine Zusammenfassung des Portfolios:

http://finance.yahoo.com/q?s=DML.TO,HAT.V,JNN.V,TAS.V,CVV.V…

Und die “Fast Facts” zu den einzelnen Unternehmen (Kurse 19.06.09, Aktienstruktur Ende Mai 09):

1. Denison Mines (DML.TO)

a. Produzent: 1,6 Mio. Pfund U3O8 (2008)

b. Aktien: 226 Mio.

c. Kurs: C$ 1,96

d. Marktkapitalisierung: C$ 443,0 Mio.

e. Website: http://www.denisonmines.com/SiteResources/ViewContent.asp?D…

f. Aktuelle Präsentation (04/09): http://www.denisonmines.com/SiteResources/data/MediaArchive…

2. Hathor Exploration (HAT.V)

a. Explorer

b. Aktien: 85,7 Mio.

c. Kurs: C$ 2,00

d. Marktkapitalisierung: C$ 171,4 Mio.

e. Website: http://www.hathor.ca/s/Home.asp

f. Aktuelle Präsentation (03/09): http://www.hathor.ca/i/presentations/Presentation20090330.p…

3. JNR Resources (JNN.V)

a. Explorer

b. Aktien: 88,5 Mio.

c. Kurs: C$ 0,27

d. Marktkapitalisierung: C$ 23,9 Mio.

e. Website: http://www.jnrresources.com/s/Home.asp

f. Aktuelle Präsentation (01/09): http://www.jnrresources.com/i/pdf/Profile_Jan09.pdf

4. CanAlaska Uranium (CVV.V)

a. Explorer

b. Aktien: 137,8 Mio.

c. Kurs: C$ 0,165

d. Marktkapitalisierung: C$ 22,7 Mio.

e. Website: http://www.canalaska.com/s/Home.asp

f. Aktuelle Präsentation: http://www.canalaska.com/i/slides/images/Nov07/gallery.html

5. Terra Ventures (TAS.V)

a. Explorer

b. Aktien: 53,2 Mio.

c. Kurs: C$ 0,39

d. Marktkapitalisierung: C$ 20,8 Mio.

e. Website: http://deutsch.terrauranium.com/haupt.php

f. Aktuelle Präsentation: http://www.terrauranium.com/Repository/documents_for_downloa…

6. Pitchstone Exploration (PXP.V)

a. Explorer

b. Aktien: 33,4 Mio.

c. Kurs: C$ 0,43

d. Marktkapitalisierung: C$ 14,4 Mio.

e. Website: http://www.pitchstone.net/

f. Aktuelle Präsentation (05/09): http://www.pitchstone.net/pdfs/PEL.Experienced%20Uranium%20E…

7. Fission Energy (FIS.V)

a. Explorer

b. Aktien: 42,1 Mio.

c. Kurs: C$ 0,28

d. Marktkapitalisierung: C$ 11,8 Mio.

e. Website: http://www.fission-energy.com/s/Home.asp

f. Aktuelle Präsentation (05/09): http://www.fission-energy.com/i/pdf/2009_06_PRESENTATION.pdf

8. Int. Enexco (IEC.V)

a. Explorer

b. Aktien: 22,6 Mio.

c. Kurs: C$ 0,355

d. Marktkapitalisierung: C$ 8,0 Mio.

e. Website: http://enexco.ca/main/?en&home

f. Aktuelle Präsentation (01/09): http://www.enexco.ca/userfiles/file/Enexco-Jan09-1.pps

9. Forum Uranium (FDC.V)

a. Explorer

b. Aktien: 88,3 Mio.

c. Kurs: C$ 0,085

d. Marktkapitalisierung: C$ 7,5 Mio.

e. Website: http://www.forumuranium.com/s/Home.asp

f. Aktuelle Präsentation: http://www.forumuranium.com/i/pdf/ForumPresentation2009.pdf

10. Triex Minerals (JNN.V)

a. Explorer

b. Aktien: 20,0 Mio.

c. Kurs: C$ 0,32

d. Marktkapitalisierung: C$ 6,4 Mio.

e. Website: http://www.triexminerals.com/s/Home.asp

f. Aktuelle Präsentation (01/09): http://www.triexminerals.com/i/pdf/TriexInvestorCambridge.pd…

1. Denison Mines (DML.TO)

2. Hathor Exploration (HAT.V)

3. JNR Resources (JNN.V)

4. CanAlaska Uranium (CVV.V)

5. Terra Ventures (TAS.V)

6. Pitchstone Exploration (PXP.V)

7. Fission Energy (FIS.V)

8. Int. Enexco (IEC.V)

9. Forum Uranium (FDC.V)

10. Triex Minerals (TXM.V)

(Die Reihenfolge ist nach aktueller Marktkapitalisierung zusammengestellt und soll keine Wertung darstellen)

Hier eine Zusammenfassung des Portfolios:

http://finance.yahoo.com/q?s=DML.TO,HAT.V,JNN.V,TAS.V,CVV.V…

Und die “Fast Facts” zu den einzelnen Unternehmen (Kurse 19.06.09, Aktienstruktur Ende Mai 09):

1. Denison Mines (DML.TO)

a. Produzent: 1,6 Mio. Pfund U3O8 (2008)

b. Aktien: 226 Mio.

c. Kurs: C$ 1,96

d. Marktkapitalisierung: C$ 443,0 Mio.

e. Website: http://www.denisonmines.com/SiteResources/ViewContent.asp?D…

f. Aktuelle Präsentation (04/09): http://www.denisonmines.com/SiteResources/data/MediaArchive…

2. Hathor Exploration (HAT.V)

a. Explorer

b. Aktien: 85,7 Mio.

c. Kurs: C$ 2,00

d. Marktkapitalisierung: C$ 171,4 Mio.

e. Website: http://www.hathor.ca/s/Home.asp

f. Aktuelle Präsentation (03/09): http://www.hathor.ca/i/presentations/Presentation20090330.p…

3. JNR Resources (JNN.V)

a. Explorer

b. Aktien: 88,5 Mio.

c. Kurs: C$ 0,27

d. Marktkapitalisierung: C$ 23,9 Mio.

e. Website: http://www.jnrresources.com/s/Home.asp

f. Aktuelle Präsentation (01/09): http://www.jnrresources.com/i/pdf/Profile_Jan09.pdf

4. CanAlaska Uranium (CVV.V)

a. Explorer

b. Aktien: 137,8 Mio.

c. Kurs: C$ 0,165

d. Marktkapitalisierung: C$ 22,7 Mio.

e. Website: http://www.canalaska.com/s/Home.asp

f. Aktuelle Präsentation: http://www.canalaska.com/i/slides/images/Nov07/gallery.html

5. Terra Ventures (TAS.V)

a. Explorer

b. Aktien: 53,2 Mio.

c. Kurs: C$ 0,39

d. Marktkapitalisierung: C$ 20,8 Mio.

e. Website: http://deutsch.terrauranium.com/haupt.php

f. Aktuelle Präsentation: http://www.terrauranium.com/Repository/documents_for_downloa…

6. Pitchstone Exploration (PXP.V)

a. Explorer

b. Aktien: 33,4 Mio.

c. Kurs: C$ 0,43

d. Marktkapitalisierung: C$ 14,4 Mio.

e. Website: http://www.pitchstone.net/

f. Aktuelle Präsentation (05/09): http://www.pitchstone.net/pdfs/PEL.Experienced%20Uranium%20E…

7. Fission Energy (FIS.V)

a. Explorer

b. Aktien: 42,1 Mio.

c. Kurs: C$ 0,28

d. Marktkapitalisierung: C$ 11,8 Mio.

e. Website: http://www.fission-energy.com/s/Home.asp

f. Aktuelle Präsentation (05/09): http://www.fission-energy.com/i/pdf/2009_06_PRESENTATION.pdf

8. Int. Enexco (IEC.V)

a. Explorer

b. Aktien: 22,6 Mio.

c. Kurs: C$ 0,355

d. Marktkapitalisierung: C$ 8,0 Mio.

e. Website: http://enexco.ca/main/?en&home

f. Aktuelle Präsentation (01/09): http://www.enexco.ca/userfiles/file/Enexco-Jan09-1.pps

9. Forum Uranium (FDC.V)

a. Explorer

b. Aktien: 88,3 Mio.

c. Kurs: C$ 0,085

d. Marktkapitalisierung: C$ 7,5 Mio.

e. Website: http://www.forumuranium.com/s/Home.asp

f. Aktuelle Präsentation: http://www.forumuranium.com/i/pdf/ForumPresentation2009.pdf

10. Triex Minerals (JNN.V)

a. Explorer

b. Aktien: 20,0 Mio.

c. Kurs: C$ 0,32

d. Marktkapitalisierung: C$ 6,4 Mio.

e. Website: http://www.triexminerals.com/s/Home.asp

f. Aktuelle Präsentation (01/09): http://www.triexminerals.com/i/pdf/TriexInvestorCambridge.pd…

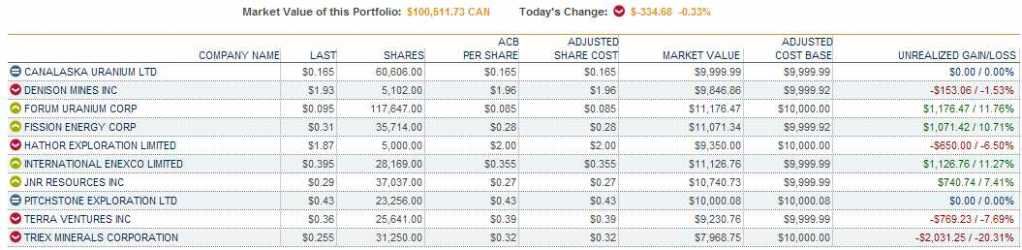

Und hier die Portfolio-Übersicht, Start: 19.06.2009 (wird regelmäßig aktualisiert):

FANTOMAS

FANTOMAS

Antwort auf Beitrag Nr.: 37.435.431 von Fantomas96 am 21.06.09 13:55:17http://www.uranium.info/index.cfm?go=c.page&id=60

kann man auch nutzen

Bei den von dir angegebenen Explorern wäre noch gut gewesen die warscheinliche Produktionszeit anzugeben.

kann man auch nutzen

Bei den von dir angegebenen Explorern wäre noch gut gewesen die warscheinliche Produktionszeit anzugeben.

Antwort auf Beitrag Nr.: 37.435.431 von Fantomas96 am 21.06.09 13:55:17Erstklassige Threaderöffnung!

Hochspannendes Thema, bin selber immer wieder in Uranwerten engagiert, sind auch meiner Meinung nach sehr gute Aktien dabei.

Was hält der Threaderöffner vom Thema Thorium, als möglicherweise und teilw. in Indien schon Anwendung findende Technologie der nächsten Generation?

LG, PR

Hochspannendes Thema, bin selber immer wieder in Uranwerten engagiert, sind auch meiner Meinung nach sehr gute Aktien dabei.

Was hält der Threaderöffner vom Thema Thorium, als möglicherweise und teilw. in Indien schon Anwendung findende Technologie der nächsten Generation?

LG, PR

Trading Spotlight

Antwort auf Beitrag Nr.: 37.435.431 von Fantomas96 am 21.06.09 13:55:17Hallo @Fantomas96,

sehr schöner Thread, sehr informativ und gut zusammengestellt!!

Danke hier schon mal für deine Mühe und Arbeit, hoffe es wird auch belohnt...!!!

Ich kenne näher nur TVC

http://www.tournigan.com/s/home.asp

WKN: 898464

ISIN: CA8915651035

Symbol: TGP

hier mal ne kleine Info :

The current resource at Kuriskova is 14.7 million pounds U3O8 indicated contained in 1.2 million tonnes at 0.558% U3O8 and 17.9 million pounds U3O8 inferred contained in 3.8 million tonnes at 0.215% U3O8; cut-off of 0.05%U. Tournigan's uranium licences include the Novoveska Huta uranium deposit

Assuming a positive preliminary assessment report, our plans are to initiate a pre-feasibility study which is expected to be completed in the first half of 2010. We are pleased to be working with PAH and RDI, both well-regarded firms known for their high standards, at this important stage of the development of our flagship property in Slovakia."

lovakia is economically and politically stable, has excellent infrastructure and, as of January 1, 2009, has adopted the Euro currency. Tournigan Energy is committed to safe and sustainable exploration and mine development in Slovakia and its other operational jurisdictions

Habe leider heute wenig Zeit, werde aber bestimmt hier mit lesen!!!

Gruß

TimLuca

sehr schöner Thread, sehr informativ und gut zusammengestellt!!

Danke hier schon mal für deine Mühe und Arbeit, hoffe es wird auch belohnt...!!!

Ich kenne näher nur TVC

http://www.tournigan.com/s/home.asp

WKN: 898464

ISIN: CA8915651035

Symbol: TGP

hier mal ne kleine Info :

The current resource at Kuriskova is 14.7 million pounds U3O8 indicated contained in 1.2 million tonnes at 0.558% U3O8 and 17.9 million pounds U3O8 inferred contained in 3.8 million tonnes at 0.215% U3O8; cut-off of 0.05%U. Tournigan's uranium licences include the Novoveska Huta uranium deposit

Assuming a positive preliminary assessment report, our plans are to initiate a pre-feasibility study which is expected to be completed in the first half of 2010. We are pleased to be working with PAH and RDI, both well-regarded firms known for their high standards, at this important stage of the development of our flagship property in Slovakia."

lovakia is economically and politically stable, has excellent infrastructure and, as of January 1, 2009, has adopted the Euro currency. Tournigan Energy is committed to safe and sustainable exploration and mine development in Slovakia and its other operational jurisdictions

Habe leider heute wenig Zeit, werde aber bestimmt hier mit lesen!!!

Gruß

TimLuca

Antwort auf Beitrag Nr.: 37.435.443 von Fantomas96 am 21.06.09 13:57:59Ja, da kann ich nur sagen: und das ist SPITZE !!! Bin in UUU drin,

denke für`s 1. reicht das. Gruß, chinagerd

denke für`s 1. reicht das. Gruß, chinagerd

mal wieder eine super Aufstellung von Fantomas.

Denison ist eigentlich der solideste Wert und fast ein muss (auch wenn ich sie momentan nicht hab)

Denison ist eigentlich der solideste Wert und fast ein muss (auch wenn ich sie momentan nicht hab)

Antwort auf Beitrag Nr.: 37.435.431 von Fantomas96 am 21.06.09 13:55:17Vorbildliche Threaderöffnung!

Lese gerne mit. Danke.

Lese gerne mit. Danke.

weitere gute Werte:

Strateco Res.

(abbau lohnt wohl erst ab einem uranpreis bei 60)

UR Energy

(lohnt schon bei 40 rum, wyoming-genehmigung da, von oberster stelle muss man wohl noch abwarten, produktion ab 2011 denke ich)

Strateco Res.

(abbau lohnt wohl erst ab einem uranpreis bei 60)

UR Energy

(lohnt schon bei 40 rum, wyoming-genehmigung da, von oberster stelle muss man wohl noch abwarten, produktion ab 2011 denke ich)

Athabasca Basin - "Grade is King" und “Size doesn´t matter” !

Das Athabasca Becken in Saskatchewan, Kanada, ist mit der weltweit besten geologischen Situation ausgestattet, um höchstgradige Uranvorkommen zu finden.

Hier sind seit 1968 insgesamt 18 Deposits mit einem Gesamtvolumen von 1,4 MILLIARDEN Pfund Uran gefunden worden.

Dazu zählt vor allem die McArthur River Mine (437 Mio. Pfund Uran mit durchschnittlichem Gehalt von 25% (!) , jährliche Produktion von 18 Mio. Pfund Uran für 20 Jahre seit 1999).

Aber auch die immer noch nicht in Betrieb genommene Cigar Lake Mine mit einem Vorkommen von 232 Mio. Pfund Uran mit durchschnittlichem Gehalt von 19% (!).

Und hier die größten Minen im Athabasca Becken mit ihren Vorkommen:

Im Athabasca Becken wird 23% der weltweiten Uranproduktion hergestellt und es befinden sich 33% der weltweiten Uran-Vorkommen in diesem Gebiet.

Von hochgradigen Vorkommen wird bei einer Urankonzentration von mehr als 2% (20.000 ppm = parts per million) gesprochen.

Die größten Minen im Athabasca Becken haben sogar Gehalte von 20% und mehr U3O8 (McArthur River / Cigar Lake).

Zum Vergleich liefern die größten australischen Minen (Olympic Dam / Ranger), ähnlich wie Uranminen in Afrika, gerade mal Gehalte von 0,2% U3O8 und werden somit in die Kategorie "Low-grade deposit" eingeordnet.

"Size doesn´t matter" - dieser Spruch gilt insbesondere für die Exploration im Athabasca Becken. Denn auch, wenn ein Fund nicht gleich ein riesiges Deposit wird, hilft häufig die hohe Urankonzentration (die im hochgradigen Bereich bis zu 100 Mal höher ist als irgendwo anders auf der Welt), um immer noch ein ökonomisch abbaubares Vorkommen zu erhalten.

Wenn dann allerdings noch die Tonnage dazukommt (großer mineralisierter Erzkörper), hat man einen wahren "Elefanten" "am Haken" ! Und diese Chance ist für jeden Explorer im Athabasca Becken halt höher als irgendwo anders auf der Welt !

Zur Geologie:

Ein Großteil der Funde im Athabasca Becken sind die sogenannten "unconformity-style deposits" :

hier handelt es sich um einen geophysikalischen Vorgang in der Erde, der auf zwei verschiedenen Gesteinsschichten beruht.

Im Athabasca Becken ist die untere, ältere Gesteinsschicht ("basement rock") häufig granitähnlich und verformt. Diese Schicht wird durch eine jüngere Sandsteinschicht überlagert.

Den Bereich, wo es durch Verschiebungen dieser zwei Schichten zu einem Bruch oder Spalt gekommen ist, nennt man "unconformity" (= Ungleichmäßigkeit). Dieser Bruch zieht sich in unregelmäßigen Linien und verschiedenen Tiefen (von knapp unter der Oberfläche bis zu 1000 Meter Tiefe) durch das gesamte Athabasca Becken.

Die "unconformity", der Spalt oder die Lücke zwischen zwei Gesteinsschichten, hat die Sammlung von uranhaltigen Flüssigkeiten (und anderen Metallen und Erzen) aus dem Erdinnern ermöglicht.

Diese sind durch magmatische und / oder hydrothermale Vorgänge im Erdinnern Richtung Oberfläche gedrückt worden.

Die "unconformity" spielte dann quasi eine natürliche geochemische Falle, da sich die flüssigen Elemente in dieser Spalte oder Lücke sammeln und absetzen konnten.

Weiterhin wird bei der Uranexploration im Athabasca Becken nicht nur nach der "unconformity zone" gesucht, sondern auch noch sogennante "fault zones" (Gräben oder Höhlen durch unterirdische Verschiebungen).

Diese "fault zones" entspringen häufig aus dem Grundgestein ("basement rocks") und können sich bis weit in den Sandsteinbereich ausbreiten.

Wo diese "fault zones" dann die "unconformity" unterberechen, werden genügend große unterirdische "Höhlen" geschaffen, in denen sich größere Mengen von flüssigen Metallen und Erzen sammeln konnten , um dann abzukühlen und zu erhärten.

Das Ergebnis sind die sogenannten "lenses", also linsenförmige unterirdische, erzhaltige Gebilde. Die "lenses" stellen die häufigste Urandeposit-Form im Athabasca Becken dar. Sie befinden sich häufig wie ein Sattel AUF der "unconformity" (klassische unconformity Mineralisierung), eventuell auch deutlich ÜBER der "unconformity" (wenn die "fault zone" sich eher vertikal über der unconformity erstreckt), oder auch UNTER der "unconformity" (eine typische "Grundmineralisierung" = "basement mineralization").

Die Deposits im Athabasca Becken sind i.d.R. durch luft- und/oder bodengestützte geophysikalische (magnetische und elektromagnetische) Untersuchungen eingegrenzt worden. Da häufig Grafit im Bereich der „unconformity“ anzufinden ist (daher auch häufig die „Brüche“ im Gestein und Bildung von „Linsen“), ist ein Vorkommen durch die Leitfähigkeit der Grafits (guter elektromagnetischer Leiter) in den „EM surveys“ gut zu lokalisieren.

Dann kommen bei Bohrungen noch weitere Spezialuntersuchungen zum Einsatz („downhole geophysics“), um die mineralisierten Zonen näher einzugrenzen.

Da die Deposits, wie oben geschrieben, zwar gehaltsmäßig häufig sehr hoch, aber flächenmäßig häufig sehr klein sein, ist das Auffinden sprichwörtlich mit „der Stecknadel im Heuhaufen“ zu vergleichen.

Am Beispiel von Hathor´s Bohrkern #40 soll diese Problematik mal veranschaulicht werden:

Bohrloch # 40 zeigt, wie dramatisch sich die Urangehalte verändern können.

Innerhalb weniger Zentimeter springen die Werte von 0,41% U3O8 (was bei vielen Explorern schon zu Freudensprüngen führen würde) auf sagenhafte 61,8% U3O8.

Ein entscheidender weiterer Anhaltspunkt für die Exploration sind die sogenannten „pathfinder minerals“.

Denn dort, wo sich die magmatischen Flüssigkeiten in den Höhlen bei der „unconformity“ angesammelt haben, hinterlassen sie auf ihrem Weg in den Zwischenräumen immer wieder „Reste“ der Mineralien und Erze. Die Ablagerungen in den „Gängen“ bis zu einem Deposit werden dann in den Bohrlöchern gefunden und bei höheren Konzentrationen nähert man sich quasi der Quelle des Deposits (daher auch der Name Pfadfinder-Mineralien).

Zu den typischen Uran-Pfadfinder-Mineralien gehören u.a. Nickel, Kobalt, Molybdän, Eisen, Arsen und Kupfer. Diese tragen bei einem möglichen Abbau eines Deposits natürlich auch zur Senkung der Abbaukosten bei, da sie als Nebenprodukte ökonomisch verwertet werden können (einige Vorkommen haben derart große „by-product“ Gehalte, dass die Uranförderung quasi zu Null-Kosten erfolgen kann!).

Das alles sind für mich nach viel Recherche die Fakten, warum ich neben einem kommenden Anstieg im Uranmarkt vor allem auf die Explorer und Produzenten im kanadischen Athabasca Becken setze.

Dies ist kein Investment-Hinweis, macht Euch selber ein Bild und recherchiert bevor ihr investiert.

Und vor allem diversifiziert Euer Investment bei Explorern auf mehrere Firmen (ideal 5-10), da der Markt sehr volatil ist.

“Buy low and sell high“ und viel Spaß mit Euren Uran-Investments über die nächsten Jahre wünscht

Das Athabasca Becken in Saskatchewan, Kanada, ist mit der weltweit besten geologischen Situation ausgestattet, um höchstgradige Uranvorkommen zu finden.

Hier sind seit 1968 insgesamt 18 Deposits mit einem Gesamtvolumen von 1,4 MILLIARDEN Pfund Uran gefunden worden.

Dazu zählt vor allem die McArthur River Mine (437 Mio. Pfund Uran mit durchschnittlichem Gehalt von 25% (!) , jährliche Produktion von 18 Mio. Pfund Uran für 20 Jahre seit 1999).

Aber auch die immer noch nicht in Betrieb genommene Cigar Lake Mine mit einem Vorkommen von 232 Mio. Pfund Uran mit durchschnittlichem Gehalt von 19% (!).

Und hier die größten Minen im Athabasca Becken mit ihren Vorkommen:

Im Athabasca Becken wird 23% der weltweiten Uranproduktion hergestellt und es befinden sich 33% der weltweiten Uran-Vorkommen in diesem Gebiet.

Von hochgradigen Vorkommen wird bei einer Urankonzentration von mehr als 2% (20.000 ppm = parts per million) gesprochen.

Die größten Minen im Athabasca Becken haben sogar Gehalte von 20% und mehr U3O8 (McArthur River / Cigar Lake).

Zum Vergleich liefern die größten australischen Minen (Olympic Dam / Ranger), ähnlich wie Uranminen in Afrika, gerade mal Gehalte von 0,2% U3O8 und werden somit in die Kategorie "Low-grade deposit" eingeordnet.

"Size doesn´t matter" - dieser Spruch gilt insbesondere für die Exploration im Athabasca Becken. Denn auch, wenn ein Fund nicht gleich ein riesiges Deposit wird, hilft häufig die hohe Urankonzentration (die im hochgradigen Bereich bis zu 100 Mal höher ist als irgendwo anders auf der Welt), um immer noch ein ökonomisch abbaubares Vorkommen zu erhalten.

Wenn dann allerdings noch die Tonnage dazukommt (großer mineralisierter Erzkörper), hat man einen wahren "Elefanten" "am Haken" ! Und diese Chance ist für jeden Explorer im Athabasca Becken halt höher als irgendwo anders auf der Welt !

Zur Geologie:

Ein Großteil der Funde im Athabasca Becken sind die sogenannten "unconformity-style deposits" :

hier handelt es sich um einen geophysikalischen Vorgang in der Erde, der auf zwei verschiedenen Gesteinsschichten beruht.

Im Athabasca Becken ist die untere, ältere Gesteinsschicht ("basement rock") häufig granitähnlich und verformt. Diese Schicht wird durch eine jüngere Sandsteinschicht überlagert.

Den Bereich, wo es durch Verschiebungen dieser zwei Schichten zu einem Bruch oder Spalt gekommen ist, nennt man "unconformity" (= Ungleichmäßigkeit). Dieser Bruch zieht sich in unregelmäßigen Linien und verschiedenen Tiefen (von knapp unter der Oberfläche bis zu 1000 Meter Tiefe) durch das gesamte Athabasca Becken.

Die "unconformity", der Spalt oder die Lücke zwischen zwei Gesteinsschichten, hat die Sammlung von uranhaltigen Flüssigkeiten (und anderen Metallen und Erzen) aus dem Erdinnern ermöglicht.

Diese sind durch magmatische und / oder hydrothermale Vorgänge im Erdinnern Richtung Oberfläche gedrückt worden.

Die "unconformity" spielte dann quasi eine natürliche geochemische Falle, da sich die flüssigen Elemente in dieser Spalte oder Lücke sammeln und absetzen konnten.

Weiterhin wird bei der Uranexploration im Athabasca Becken nicht nur nach der "unconformity zone" gesucht, sondern auch noch sogennante "fault zones" (Gräben oder Höhlen durch unterirdische Verschiebungen).

Diese "fault zones" entspringen häufig aus dem Grundgestein ("basement rocks") und können sich bis weit in den Sandsteinbereich ausbreiten.

Wo diese "fault zones" dann die "unconformity" unterberechen, werden genügend große unterirdische "Höhlen" geschaffen, in denen sich größere Mengen von flüssigen Metallen und Erzen sammeln konnten , um dann abzukühlen und zu erhärten.

Das Ergebnis sind die sogenannten "lenses", also linsenförmige unterirdische, erzhaltige Gebilde. Die "lenses" stellen die häufigste Urandeposit-Form im Athabasca Becken dar. Sie befinden sich häufig wie ein Sattel AUF der "unconformity" (klassische unconformity Mineralisierung), eventuell auch deutlich ÜBER der "unconformity" (wenn die "fault zone" sich eher vertikal über der unconformity erstreckt), oder auch UNTER der "unconformity" (eine typische "Grundmineralisierung" = "basement mineralization").

Die Deposits im Athabasca Becken sind i.d.R. durch luft- und/oder bodengestützte geophysikalische (magnetische und elektromagnetische) Untersuchungen eingegrenzt worden. Da häufig Grafit im Bereich der „unconformity“ anzufinden ist (daher auch häufig die „Brüche“ im Gestein und Bildung von „Linsen“), ist ein Vorkommen durch die Leitfähigkeit der Grafits (guter elektromagnetischer Leiter) in den „EM surveys“ gut zu lokalisieren.

Dann kommen bei Bohrungen noch weitere Spezialuntersuchungen zum Einsatz („downhole geophysics“), um die mineralisierten Zonen näher einzugrenzen.

Da die Deposits, wie oben geschrieben, zwar gehaltsmäßig häufig sehr hoch, aber flächenmäßig häufig sehr klein sein, ist das Auffinden sprichwörtlich mit „der Stecknadel im Heuhaufen“ zu vergleichen.

Am Beispiel von Hathor´s Bohrkern #40 soll diese Problematik mal veranschaulicht werden:

Bohrloch # 40 zeigt, wie dramatisch sich die Urangehalte verändern können.

Innerhalb weniger Zentimeter springen die Werte von 0,41% U3O8 (was bei vielen Explorern schon zu Freudensprüngen führen würde) auf sagenhafte 61,8% U3O8.

Ein entscheidender weiterer Anhaltspunkt für die Exploration sind die sogenannten „pathfinder minerals“.

Denn dort, wo sich die magmatischen Flüssigkeiten in den Höhlen bei der „unconformity“ angesammelt haben, hinterlassen sie auf ihrem Weg in den Zwischenräumen immer wieder „Reste“ der Mineralien und Erze. Die Ablagerungen in den „Gängen“ bis zu einem Deposit werden dann in den Bohrlöchern gefunden und bei höheren Konzentrationen nähert man sich quasi der Quelle des Deposits (daher auch der Name Pfadfinder-Mineralien).

Zu den typischen Uran-Pfadfinder-Mineralien gehören u.a. Nickel, Kobalt, Molybdän, Eisen, Arsen und Kupfer. Diese tragen bei einem möglichen Abbau eines Deposits natürlich auch zur Senkung der Abbaukosten bei, da sie als Nebenprodukte ökonomisch verwertet werden können (einige Vorkommen haben derart große „by-product“ Gehalte, dass die Uranförderung quasi zu Null-Kosten erfolgen kann!).

Das alles sind für mich nach viel Recherche die Fakten, warum ich neben einem kommenden Anstieg im Uranmarkt vor allem auf die Explorer und Produzenten im kanadischen Athabasca Becken setze.

Dies ist kein Investment-Hinweis, macht Euch selber ein Bild und recherchiert bevor ihr investiert.

Und vor allem diversifiziert Euer Investment bei Explorern auf mehrere Firmen (ideal 5-10), da der Markt sehr volatil ist.

“Buy low and sell high“ und viel Spaß mit Euren Uran-Investments über die nächsten Jahre wünscht

Antwort auf Beitrag Nr.: 37.435.951 von Fantomas96 am 21.06.09 16:55:11Also wenn - und davon gehe ich aus, du hier die Informationen suchst, findest und zusammenstellst, siehst du mich wirklich staunen.

Wiederhole mein Lob von vorhin daher sehr gerne.

Den Thread sollte man sich unbedingt merken.

Beste Grüße

PR

Wiederhole mein Lob von vorhin daher sehr gerne.

Den Thread sollte man sich unbedingt merken.

Beste Grüße

PR

Antwort auf Beitrag Nr.: 37.435.990 von Public_Relations am 21.06.09 17:10:01@PR

Vielen Dank für die Blumen!

Ja, Du siehst das Ergebnis einer wochenlangen Recherche hier, die ich gerne der Allgemeinheit zur Verfügung stelle (da kommt übrigens noch mehr!). Ich wünsche mir daher sehr konstruktive Reaktionen, die mich dann auch wieder weiterbringen.

Sehr idealistisch, ich weiß, aber meine Vorstellung von einem gut funktionierenden Aktien-Board !

Ich halte mich bei meinen Investitionen immer an den Rat, den ich allen hier im letzten Posting gegeben habe, da ich ein Long-Investor und kein Momentum-Trader bin.

"Recherche, Recherche und nochmals Recherche VOR jeder Investition, um die "richtige Perlen" zu finden".

Aber trotzdem ist und bleibt das Explorerbusiness sehr risikobehaftet und volatil.

Gruß,

FANTOMAS

Vielen Dank für die Blumen!

Ja, Du siehst das Ergebnis einer wochenlangen Recherche hier, die ich gerne der Allgemeinheit zur Verfügung stelle (da kommt übrigens noch mehr!). Ich wünsche mir daher sehr konstruktive Reaktionen, die mich dann auch wieder weiterbringen.

Sehr idealistisch, ich weiß, aber meine Vorstellung von einem gut funktionierenden Aktien-Board !

Ich halte mich bei meinen Investitionen immer an den Rat, den ich allen hier im letzten Posting gegeben habe, da ich ein Long-Investor und kein Momentum-Trader bin.

"Recherche, Recherche und nochmals Recherche VOR jeder Investition, um die "richtige Perlen" zu finden".

Aber trotzdem ist und bleibt das Explorerbusiness sehr risikobehaftet und volatil.

Gruß,

FANTOMAS

MERKEN

gute Arbeit

gute Arbeit

Antwort auf Beitrag Nr.: 37.435.473 von bonanzarad am 21.06.09 14:01:53@ bonanzarad

Bei den von dir angegebenen Explorern wäre noch gut gewesen die warscheinliche Produktionszeit anzugeben.

Wird schwierig, da die meisten Explorer (und nicht nur die von mir hier aufgezählten) wahrscheinlich NIEMALS produzieren werden.

Das primäre Ziel vieler Explorer ist das Auffinden von Vorkommen mit anschließendem Verkauf zu einem möglichst hohen Preis an einen Produzenten.

FANTOMAS

Bei den von dir angegebenen Explorern wäre noch gut gewesen die warscheinliche Produktionszeit anzugeben.

Wird schwierig, da die meisten Explorer (und nicht nur die von mir hier aufgezählten) wahrscheinlich NIEMALS produzieren werden.

Das primäre Ziel vieler Explorer ist das Auffinden von Vorkommen mit anschließendem Verkauf zu einem möglichst hohen Preis an einen Produzenten.

FANTOMAS

Antwort auf Beitrag Nr.: 37.435.625 von Public_Relations am 21.06.09 14:54:24@ PR

Was hält der Threaderöffner vom Thema Thorium, als möglicherweise und teilw. in Indien schon Anwendung findende Technologie der nächsten Generation?

Auch sehr interessantes Thema!

Bin aber in meiner Recherche da noch längst nicht soweit.

FANTOMAS

Was hält der Threaderöffner vom Thema Thorium, als möglicherweise und teilw. in Indien schon Anwendung findende Technologie der nächsten Generation?

Auch sehr interessantes Thema!

Bin aber in meiner Recherche da noch längst nicht soweit.

FANTOMAS

Antwort auf Beitrag Nr.: 37.435.775 von Boersenkrieger am 21.06.09 15:58:28@ Boersenkrieger

Strateco Res.

(abbau lohnt wohl erst ab einem uranpreis bei 60)

UR Energy

(lohnt schon bei 40 rum, wyoming-genehmigung da, von oberster stelle muss man wohl noch abwarten, produktion ab 2011 denke ich)

Beides gute Werte, aber leider nicht Athabasca !

Strateco im Otish Gebiet sehr vielversprechend, aber low grade.

USA ist mir mit Abbau-Genehmigungen zu heikel !

Aber nur meine Meinung.

FANTOMAS

Strateco Res.

(abbau lohnt wohl erst ab einem uranpreis bei 60)

UR Energy

(lohnt schon bei 40 rum, wyoming-genehmigung da, von oberster stelle muss man wohl noch abwarten, produktion ab 2011 denke ich)

Beides gute Werte, aber leider nicht Athabasca !

Strateco im Otish Gebiet sehr vielversprechend, aber low grade.

USA ist mir mit Abbau-Genehmigungen zu heikel !

Aber nur meine Meinung.

FANTOMAS

Antwort auf Beitrag Nr.: 37.436.055 von Fantomas96 am 21.06.09 17:32:42Der Laie staunt und der Fachmann wundert sich!

@Fantomas:

Wird im Muster-Portfolio auch mit SL gearbeitet? Erfolgt aufgrund der Kursentwicklung auch eine Rotation im Portfolio? Findet allenfalls auch ein Titel Aufnahme, der nicht mit dem Athasbasca Becken in Verbindung steht?

@Fantomas:

Wird im Muster-Portfolio auch mit SL gearbeitet? Erfolgt aufgrund der Kursentwicklung auch eine Rotation im Portfolio? Findet allenfalls auch ein Titel Aufnahme, der nicht mit dem Athasbasca Becken in Verbindung steht?

Antwort auf Beitrag Nr.: 37.436.070 von Fantomas96 am 21.06.09 17:37:56stimmt natürlich... ausserhalb des beckens diese werte.

Strateco ist schon relativ weit aber eben low grade und es lohnt sich erst wieder richtig wenn uran deutlicher steigt.

URE:

die genehmigung aus Wyoming ist eben schon da. aber es braucht ja auch eine regierungsgenehmigung. sollte eigentlich mal im frühjahr kommen... naja scheint auch eben an Obama zu liegen.

das gute ist halt dass sie auf einem cashberg sitzen und durchfinanziert sind aber eben auf Wyoming bezogen. sollte das wider erwarten doch noch schiefgehen sieht´s natürlich schlecht aus.

von daher bleibt hier halt ein risikofaktor der schwerwiegend wäre.

ich würde als soliden wert Dennison klar favorisieren bzgl kaum vorhandener Risiken.

Strateco ist schon relativ weit aber eben low grade und es lohnt sich erst wieder richtig wenn uran deutlicher steigt.

URE:

die genehmigung aus Wyoming ist eben schon da. aber es braucht ja auch eine regierungsgenehmigung. sollte eigentlich mal im frühjahr kommen... naja scheint auch eben an Obama zu liegen.

das gute ist halt dass sie auf einem cashberg sitzen und durchfinanziert sind aber eben auf Wyoming bezogen. sollte das wider erwarten doch noch schiefgehen sieht´s natürlich schlecht aus.

von daher bleibt hier halt ein risikofaktor der schwerwiegend wäre.

ich würde als soliden wert Dennison klar favorisieren bzgl kaum vorhandener Risiken.

Antwort auf Beitrag Nr.: 37.436.081 von Caravest am 21.06.09 17:42:23@ Caravest

Wird im Muster-Portfolio auch mit SL gearbeitet? Erfolgt aufgrund der Kursentwicklung auch eine Rotation im Portfolio? Findet allenfalls auch ein Titel Aufnahme, der nicht mit dem Athasbasca Becken in Verbindung steht?

1. Bei Explorern bitte NUR Stop Loss "im Kopf", sonst "klauen" Euch die Market Maker Eure Aktien "unter dem Hintern weg" !

2. Rotation bis jetzt nicht vorgesehen. Habe jeden Wert mit CAD 10.000 ins Portfolio aufgenommen (= CAD 100.000 gesamt).

Performance wird 1x monatlich gepostet. Es sind aber noch 2-3 Werte auf der "Nachrückliste", falls einer aus der Liste "aufgekauft" wird !

3. Titel, die NICHT im Athabasca Becken explorieren, sind zumindest bei mir NUR auf der Watchlist und kommen NICHT ins Portfolio (Gründe, s.o.).

FANTOMAS

Wird im Muster-Portfolio auch mit SL gearbeitet? Erfolgt aufgrund der Kursentwicklung auch eine Rotation im Portfolio? Findet allenfalls auch ein Titel Aufnahme, der nicht mit dem Athasbasca Becken in Verbindung steht?

1. Bei Explorern bitte NUR Stop Loss "im Kopf", sonst "klauen" Euch die Market Maker Eure Aktien "unter dem Hintern weg" !

2. Rotation bis jetzt nicht vorgesehen. Habe jeden Wert mit CAD 10.000 ins Portfolio aufgenommen (= CAD 100.000 gesamt).

Performance wird 1x monatlich gepostet. Es sind aber noch 2-3 Werte auf der "Nachrückliste", falls einer aus der Liste "aufgekauft" wird !

3. Titel, die NICHT im Athabasca Becken explorieren, sind zumindest bei mir NUR auf der Watchlist und kommen NICHT ins Portfolio (Gründe, s.o.).

FANTOMAS

Antwort auf Beitrag Nr.: 37.436.150 von Fantomas96 am 21.06.09 18:07:00o.k. Danke.

Antwort auf Beitrag Nr.: 37.435.431 von Fantomas96 am 21.06.09 13:55:17

moin F96,

thks für die zahlreichen infos in einem hofftl. weiterhin

´meinungsreichen´ thread

moin F96,

thks für die zahlreichen infos in einem hofftl. weiterhin

´meinungsreichen´ thread

Antwort auf Beitrag Nr.: 37.436.590 von hbg55 am 21.06.09 19:55:48Antwort zu einem anderen Uranwert

hat Mr. Woolford häufiger erwähnt. Er fragte auch nach dem Sinn, sich als fast einziges Land gegen die Atomkraft zu stemmen, und sich dann von den Nachbarn die Atommeiler vor die Haustüre stellen zu lassen. Er fragte sich, woher Deutschland denn in Zukunft seine Energielieferungen herbekommt. Aus Russland, Erdgas?

Dummes Geschwätz.

Der Trend geht Richtung Energiegewinnung aus der unerschöpflichen inneren vulkanischen Erdwärme und Richtung Solarstrom.

Die Münchner Rück und Siemens planen derzeit den Bau einer gigantischen Solaranlage in der Sahara,das ist vernünftiger, dorthinein sollte positiv investiert werden.

Die Entsorgungsprobleme von nuklearen Reaktoren sind noch völlig

ungelöst.

Die Kindersterblichkeit durch Krebs in Atomkraftwerksnähe ist besonders hoch...

Alles ungelöste Probleme, Uran ist lebensfeindlich.

Die Kernenergie hatte ihre Zeit, die ist aber abgelaufen.

Gott sei Dank!

Antwort auf Beitrag Nr.: 37.436.886 von Goldwalla am 21.06.09 21:12:51...nur wird diese heile welt noch ihre zeit brauchen... ein paar jahrzehnte gehen schnell mal ins land.

und selbst wenn wir mal "clean" sind geht´s in china erst richtig los.

und selbst wenn wir mal "clean" sind geht´s in china erst richtig los.

Antwort auf Beitrag Nr.: 37.436.949 von Boersenkrieger am 21.06.09 21:29:15Täusch Dich mal nicht, in China gibt es ein revolutionäres Aufwachen.

Es wurde viel und oft gegen die Umwelt gesündigt.

Es wurden viele Fehler gemacht,wie in Tibet Wälder abgeholzt die

on Folge zu gigantischen Überschwemmungen geführt haben.

Nun wird aufgeforstet,sogar mit Hilfe der Armee.

Auch wird der nuklearen Energiegewinnung nicht mehr so sehr vertraut,

es werden überwiegend Staudämme gebaut.

Die Solartechnik wird subventioniert, es gibt unendlich große

besonnte Wüstenflächen.

Es gibt unerschöüflich Energie auf dieser Erde,

kein Grund mehr in lebensfeindlich nukleare Technologie zu

investieren.

Es ist Zeit Entscheidungen zu treffen, bin ich für- oder gegen

das Leben?

Es wurde viel und oft gegen die Umwelt gesündigt.

Es wurden viele Fehler gemacht,wie in Tibet Wälder abgeholzt die

on Folge zu gigantischen Überschwemmungen geführt haben.

Nun wird aufgeforstet,sogar mit Hilfe der Armee.

Auch wird der nuklearen Energiegewinnung nicht mehr so sehr vertraut,

es werden überwiegend Staudämme gebaut.

Die Solartechnik wird subventioniert, es gibt unendlich große

besonnte Wüstenflächen.

Es gibt unerschöüflich Energie auf dieser Erde,

kein Grund mehr in lebensfeindlich nukleare Technologie zu

investieren.

Es ist Zeit Entscheidungen zu treffen, bin ich für- oder gegen

das Leben?

Antwort auf Beitrag Nr.: 37.436.991 von Goldwalla am 21.06.09 21:40:13irgendwie ist das das falsche thema für den thread.

hier geht´s um uran-aktien und auch nur um welche die im athabasca tätig sind und nicht um dden sinn des lebens....

mein ziel zu deiner beruhigung ist es auch mit den gewinnen dann ein kfw60-häuschen oder wohnung zu kaufen

von daher thema beendet (in einem anderen thread aber gerne)

hier geht´s um uran-aktien und auch nur um welche die im athabasca tätig sind und nicht um dden sinn des lebens....

mein ziel zu deiner beruhigung ist es auch mit den gewinnen dann ein kfw60-häuschen oder wohnung zu kaufen

von daher thema beendet (in einem anderen thread aber gerne)

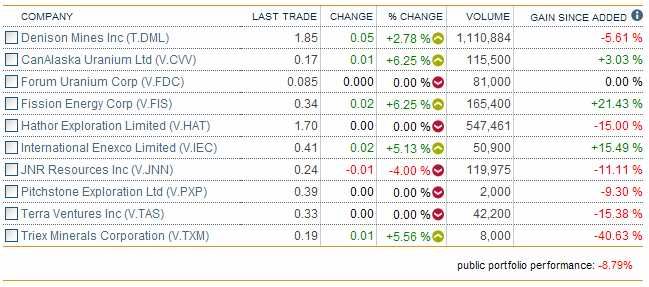

Und die 2-Jahres-Charts der vorgestellten Werte:

Denison

Hathor

JNR

Terra

CanAlaska

Fission

Pitchstone

Int. Enexco

Forum

Triex

Vielleicht hilft ja der eine oder andere Chart bei einer Entscheidung !

FANTOMAS

Denison

Hathor

JNR

Terra

CanAlaska

Fission

Pitchstone

Int. Enexco

Forum

Triex

Vielleicht hilft ja der eine oder andere Chart bei einer Entscheidung !

FANTOMAS

Antwort auf Beitrag Nr.: 37.436.991 von Goldwalla am 21.06.09 21:40:13Danke, Goldwalla, für Deine Hinweise auf die Gefahren der Atomenergie.

Leider muß ich Boersenkrieger Recht geben:

dieser Thread ist nicht zur Diskussion über Sinn oder Unsinn von Atomernergie gedacht gewesen, sondern zur Information über Uranexplorer und -produzenten im Athabasca Becken in Kanada.

Trotzdem vielen Dank für Deine Hinweise und vielleicht bringst Du Deine Argumente besser in einem allgemeinen Thread über Atomenergie an.

FANTOMAS

Leider muß ich Boersenkrieger Recht geben:

dieser Thread ist nicht zur Diskussion über Sinn oder Unsinn von Atomernergie gedacht gewesen, sondern zur Information über Uranexplorer und -produzenten im Athabasca Becken in Kanada.

Trotzdem vielen Dank für Deine Hinweise und vielleicht bringst Du Deine Argumente besser in einem allgemeinen Thread über Atomenergie an.

FANTOMAS

Der Vollständigkeit halber nenne ich auch noch meine "Nachzügler", jedoch ohne detaillierte Vorstellung:

1. Santoy Resources (SAN.V)

2. Purepoint Uranium (PTU.V)

3. Eso Uranium (ESO.V)

4. Titan Uranium (TUE.V)

FANTOMAS

1. Santoy Resources (SAN.V)

2. Purepoint Uranium (PTU.V)

3. Eso Uranium (ESO.V)

4. Titan Uranium (TUE.V)

FANTOMAS

@ Boersenkrieger / US-Genehmigungsprobleme

Aus der heutigen StarTribune Ausgabe:

http://www.casperstartribune.net/articles/2009/06/21/news/wy…

Permit delay worries uranium hopefuls

By DUSTIN BLEIZEFFER

Star-Tribune energy reporter

Sunday, June 21, 2009 12:26 AM MDT

Several proposed uranium mining projects in Wyoming and across the West will be delayed due the U.S. Nuclear Regulatory Commission's recent decision requiring a more thorough site-specific analysis for each project.

The NRC will require a supplemental environmental impact statement for each mining project rather than a more simplified environmental assessment, which the agency had considered.

Some officials in the uranium industry claim the NRC overreacted to a groundswell of public concern that they say comes from either ignorance of the in-situ leach mining process or a desire to block uranium mining.

Industry officials have also told the Star-Tribune they worry that investors are losing patience.

However, those who scrutinize the emerging next generation of uranium mining say both the industry and government regulators have a history that deserves skepticism. Shannon Anderson, community organizer for the Powder River Basin Resource Council, said she has researched dozens upon dozens of spills and excursions documented by the Wyoming Department of Environmental Quality.

The Star-Tribune has also reviewed DEQ documentation describing dozens of violations related to in-situ recovery of uranium in the state.

Most recently, a 2007 DEQ investigation documented yearslong, regular violations at Cameco Corp.'s Smith Ranch-Highland in-situ uranium mine in Converse County. It resulted in a $1 million settlement, although Cameco and DEQ insist no one was injured as a result of the violations, and there was no long-lasting environmental damage.

"Asking questions isn't necessarily opposition to these projects. We are citizens of Wyoming, and we want to promote development that is beneficial to the state. But we also want to protect citizens and the environment," Anderson said.

Industry officials counter that there have been at least 15 commercial-scale in-situ uranium well-fields successfully restored in Wyoming, and not one documented case of damage to human health or contamination of drinking water.

NRC's caution

Uranium One controls more than 100 million pounds of historically identified uranium resources in Wyoming, and says it has 61 potential mine projects in the state.

The predecessors of Uranium One first filed applications with the NRC and DEQ in October 2007 for the proposed Moore Ranch in-situ mine and processing plant near the Pumpkin Buttes in Campbell County. Company officials said the NRC's decision to require a more thorough environmental analysis means production will begin in 2011 rather than 2010.

"We have been told various firm dates by the NRC, yet every time we get close to ending the process, something changes," said Donna Wichers, senior vice president of Uranium One, Americas.

In moving to the supplemental environmental impact statement requirement, NRC reportedly told some in the uranium industry that the extra analysis makes the new mining projects less susceptible to lawsuits and legal delays.

Wayne Heili, president of mining for UR Energy, said he's obviously disappointed with the delay. However, he said it's hard to blame the NRC for doing its best to satisfy the requirements of the National Environmental Policy Act.

Heili said he believes the NRC's move toward a supplemental environmental impact statement has more to do with public comments insisting on more public involvement in the licensing process, and less about the industry's past track record.

"To the NRC's credit, they're being cautious and making sure these licenses are being issued on solid legal grounding," Heili said.

Anderson said the Powder River Basin Resource Council's membership is pleased with the NRC's decision. However, the group remains concerned that neither the federal nor state government has addressed the "legacy" issues of the industry's past, nor have they addressed the cumulative impacts of possibly dozens of new mines.

Although the in-situ recovery process is supposed to be contained within uranium ore-bearing aquifers that never have been sources of drinking water, individual landowners still deserve to know details about what's taking place underground, Anderson said. There's still no estimate of how much groundwater might be consumed cumulatively.

"(In-situ uranium recovery) can reduce aquifer pressure and affect artesian wells, and it can create draw-down in areas already impacted by coal-bed methane or other industrial development," Anderson said.

Fletcher Newton, executive vice president for marketing and strategic affairs for Uranium One, said the uranium industry is much more sophisticated than it was in the 1970s and 1980s.

"(The industry) certainly learned a lot about safe practices and protecting the environment. There's a big difference between today and the way things were 25 years ago," Newton said. "Nobody wants to go back and repeat the mistakes of the past."

White House uncertainty

Some uranium mining officials say they feel the Obama administration isn't as supportive of domestic uranium development as the previous administration. As evidence, they say the U.S. Department of Energy hasn't made good on loan guarantees promised to the industry under the Bush administration.

While there were 19 applications made to the DOE under the Bush administration, so far the DOE under the Obama administration has issued only $18.5 billion in loan guarantees to four companies that plan to build new nuclear reactors for electrical generation.

"I think this administration is moving very carefully," Newton said. "If they impose a carbon tax on utilities, then that would be an indirect way of supporting nuclear power because, suddenly, nuclear power becomes much more cost competitive."

Last week, the DOE announced it will provide $2.9 million in scholarships and fellowships to 86 U.S. nuclear science and engineering students, and will offer $6 million in grants to 29 U.S. universities for nuclear research infrastructure. None of the grant money was allocated to the University of Wyoming, according to a DOE press release.

According to the Nuclear Energy Institute, about half of the nuclear industry's work force will be eligible to retire during the next 10 years.

* The energy derived from 1 pound of uranium is equivalent to 20,000 pounds of coal.

Source: Wyoming Mining Association

* More than 200 million pounds of uranium has been mined in Wyoming since 1954. More than 300 million pounds of "historic" reserves remain.

Source: Uranium One

About in-situ mining

The conventional method of uranium mining involves carving large pits into the earth to recover ore-bearing material. In-situ recovery involves a series of wells to flush oxygen and carbon dioxide (and sometimes sodium bicarbonate) into a uranium ore-bearing aquifer, which breaks down the uranium ore.

The solution is brought to the surface through production wells where the uranium is recovered. From there, the uranium is isolated through a drying process and trucked to market in secure containers.

This ongoing circulation between injection wells and production wells takes place for two to three years in order to produce about 85 percent of the uranium resource. Monitor wells surround the production zone -- in the formations above and below -- to detect any leaks.

After production is complete, a yearslong remediation process begins. Using the same injection and production wells, the water is circulated through an ion-exchange facility

Uranium boom

The price for uranium neared $140 per pound in 2007, sparking renewed interest in the mining industry. The Nuclear Regulator Commission received notice of more than 20 in-situ uranium mine proposals across the West, mostly in Wyoming.

In response, the NRC launched a "generic" environmental impact statement to provide analysis of the in-situ leach mining process. A final version of the document was issued in May.

Today, uranium is selling for about $52 per pound, but companies are still planning many new mining operations.

FANTOMAS

Aus der heutigen StarTribune Ausgabe:

http://www.casperstartribune.net/articles/2009/06/21/news/wy…

Permit delay worries uranium hopefuls

By DUSTIN BLEIZEFFER

Star-Tribune energy reporter

Sunday, June 21, 2009 12:26 AM MDT

Several proposed uranium mining projects in Wyoming and across the West will be delayed due the U.S. Nuclear Regulatory Commission's recent decision requiring a more thorough site-specific analysis for each project.

The NRC will require a supplemental environmental impact statement for each mining project rather than a more simplified environmental assessment, which the agency had considered.

Some officials in the uranium industry claim the NRC overreacted to a groundswell of public concern that they say comes from either ignorance of the in-situ leach mining process or a desire to block uranium mining.

Industry officials have also told the Star-Tribune they worry that investors are losing patience.

However, those who scrutinize the emerging next generation of uranium mining say both the industry and government regulators have a history that deserves skepticism. Shannon Anderson, community organizer for the Powder River Basin Resource Council, said she has researched dozens upon dozens of spills and excursions documented by the Wyoming Department of Environmental Quality.

The Star-Tribune has also reviewed DEQ documentation describing dozens of violations related to in-situ recovery of uranium in the state.

Most recently, a 2007 DEQ investigation documented yearslong, regular violations at Cameco Corp.'s Smith Ranch-Highland in-situ uranium mine in Converse County. It resulted in a $1 million settlement, although Cameco and DEQ insist no one was injured as a result of the violations, and there was no long-lasting environmental damage.

"Asking questions isn't necessarily opposition to these projects. We are citizens of Wyoming, and we want to promote development that is beneficial to the state. But we also want to protect citizens and the environment," Anderson said.

Industry officials counter that there have been at least 15 commercial-scale in-situ uranium well-fields successfully restored in Wyoming, and not one documented case of damage to human health or contamination of drinking water.

NRC's caution

Uranium One controls more than 100 million pounds of historically identified uranium resources in Wyoming, and says it has 61 potential mine projects in the state.

The predecessors of Uranium One first filed applications with the NRC and DEQ in October 2007 for the proposed Moore Ranch in-situ mine and processing plant near the Pumpkin Buttes in Campbell County. Company officials said the NRC's decision to require a more thorough environmental analysis means production will begin in 2011 rather than 2010.

"We have been told various firm dates by the NRC, yet every time we get close to ending the process, something changes," said Donna Wichers, senior vice president of Uranium One, Americas.

In moving to the supplemental environmental impact statement requirement, NRC reportedly told some in the uranium industry that the extra analysis makes the new mining projects less susceptible to lawsuits and legal delays.

Wayne Heili, president of mining for UR Energy, said he's obviously disappointed with the delay. However, he said it's hard to blame the NRC for doing its best to satisfy the requirements of the National Environmental Policy Act.

Heili said he believes the NRC's move toward a supplemental environmental impact statement has more to do with public comments insisting on more public involvement in the licensing process, and less about the industry's past track record.

"To the NRC's credit, they're being cautious and making sure these licenses are being issued on solid legal grounding," Heili said.

Anderson said the Powder River Basin Resource Council's membership is pleased with the NRC's decision. However, the group remains concerned that neither the federal nor state government has addressed the "legacy" issues of the industry's past, nor have they addressed the cumulative impacts of possibly dozens of new mines.

Although the in-situ recovery process is supposed to be contained within uranium ore-bearing aquifers that never have been sources of drinking water, individual landowners still deserve to know details about what's taking place underground, Anderson said. There's still no estimate of how much groundwater might be consumed cumulatively.

"(In-situ uranium recovery) can reduce aquifer pressure and affect artesian wells, and it can create draw-down in areas already impacted by coal-bed methane or other industrial development," Anderson said.

Fletcher Newton, executive vice president for marketing and strategic affairs for Uranium One, said the uranium industry is much more sophisticated than it was in the 1970s and 1980s.

"(The industry) certainly learned a lot about safe practices and protecting the environment. There's a big difference between today and the way things were 25 years ago," Newton said. "Nobody wants to go back and repeat the mistakes of the past."

White House uncertainty

Some uranium mining officials say they feel the Obama administration isn't as supportive of domestic uranium development as the previous administration. As evidence, they say the U.S. Department of Energy hasn't made good on loan guarantees promised to the industry under the Bush administration.

While there were 19 applications made to the DOE under the Bush administration, so far the DOE under the Obama administration has issued only $18.5 billion in loan guarantees to four companies that plan to build new nuclear reactors for electrical generation.

"I think this administration is moving very carefully," Newton said. "If they impose a carbon tax on utilities, then that would be an indirect way of supporting nuclear power because, suddenly, nuclear power becomes much more cost competitive."

Last week, the DOE announced it will provide $2.9 million in scholarships and fellowships to 86 U.S. nuclear science and engineering students, and will offer $6 million in grants to 29 U.S. universities for nuclear research infrastructure. None of the grant money was allocated to the University of Wyoming, according to a DOE press release.

According to the Nuclear Energy Institute, about half of the nuclear industry's work force will be eligible to retire during the next 10 years.

* The energy derived from 1 pound of uranium is equivalent to 20,000 pounds of coal.

Source: Wyoming Mining Association

* More than 200 million pounds of uranium has been mined in Wyoming since 1954. More than 300 million pounds of "historic" reserves remain.

Source: Uranium One

About in-situ mining

The conventional method of uranium mining involves carving large pits into the earth to recover ore-bearing material. In-situ recovery involves a series of wells to flush oxygen and carbon dioxide (and sometimes sodium bicarbonate) into a uranium ore-bearing aquifer, which breaks down the uranium ore.

The solution is brought to the surface through production wells where the uranium is recovered. From there, the uranium is isolated through a drying process and trucked to market in secure containers.

This ongoing circulation between injection wells and production wells takes place for two to three years in order to produce about 85 percent of the uranium resource. Monitor wells surround the production zone -- in the formations above and below -- to detect any leaks.

After production is complete, a yearslong remediation process begins. Using the same injection and production wells, the water is circulated through an ion-exchange facility

Uranium boom

The price for uranium neared $140 per pound in 2007, sparking renewed interest in the mining industry. The Nuclear Regulator Commission received notice of more than 20 in-situ uranium mine proposals across the West, mostly in Wyoming.

In response, the NRC launched a "generic" environmental impact statement to provide analysis of the in-situ leach mining process. A final version of the document was issued in May.

Today, uranium is selling for about $52 per pound, but companies are still planning many new mining operations.

FANTOMAS

Ditem

fehlt auch noch. zumindest sind sie im becken vertreten (Beartooth) neben Otish (traten ja mal ihr Gebiet an Strateco ab und werden etwas mitverdienen/2% falls das projekt mal durchgeführt wird). früher nahm ich mal an dass sie nicht ausgerechnet ihr bestes stück im otish weggaben aber so sicher bin ich mir da nicht mehr, da sie die Exploration nicht erfunden haben

CEO Raymond Savoie (früherer Bergbauminister in Quebec)

burnrate niedrig managementgehälter gering (hab die zahlen nicht mehr im kopf)

bisherige drills eher ins leere

Savoie ist auch noch CEO von Gastem (Erdgas), auch da ging ohne fremde hilfe nix voran.

interessant war ende 2007 das MOU mit Sinosteel was dann aber von Seiten der chinesen wieder gestrichen wurde (so etwa ein jahr später) und es zu keinem JV kam und die Hoffnungen auf schnelle Fortschritte und Zukäufe zunichte machte.

derzeit im reich der vergessenen und auch so bewertet.

mehr wie däumchendrehen geht da wohl nicht.... bis zum nächsten MOU oder so...

fehlt auch noch. zumindest sind sie im becken vertreten (Beartooth) neben Otish (traten ja mal ihr Gebiet an Strateco ab und werden etwas mitverdienen/2% falls das projekt mal durchgeführt wird). früher nahm ich mal an dass sie nicht ausgerechnet ihr bestes stück im otish weggaben aber so sicher bin ich mir da nicht mehr, da sie die Exploration nicht erfunden haben

CEO Raymond Savoie (früherer Bergbauminister in Quebec)

burnrate niedrig managementgehälter gering (hab die zahlen nicht mehr im kopf)

bisherige drills eher ins leere

Savoie ist auch noch CEO von Gastem (Erdgas), auch da ging ohne fremde hilfe nix voran.

interessant war ende 2007 das MOU mit Sinosteel was dann aber von Seiten der chinesen wieder gestrichen wurde (so etwa ein jahr später) und es zu keinem JV kam und die Hoffnungen auf schnelle Fortschritte und Zukäufe zunichte machte.

derzeit im reich der vergessenen und auch so bewertet.

mehr wie däumchendrehen geht da wohl nicht.... bis zum nächsten MOU oder so...

Antwort auf Beitrag Nr.: 37.437.379 von Fantomas96 am 22.06.09 00:16:02hab ähnliches auch schon vernommen

"The additional requirements for completing an SEIS for each applicationhas necessitated a new NRC schedule which calls for completion of an SEIS for each of the pending applications by April 2010 and probableissuance of licenses by June 2010."

gefällt mir auch überhaupt nicht.

Uran ist eben ein sehr heikles thema.. da sind wir dann doch im Becken am besten aufgehoben.

letztlich nutzt es nichts wenn alle eckdaten hervorragend sind und sich die permits auf ewig hinziehen (kennt man ja auch bei anderen geschichten wie Canadian Zinc z.b. und da geht´s nur um zink und silber)

"The additional requirements for completing an SEIS for each applicationhas necessitated a new NRC schedule which calls for completion of an SEIS for each of the pending applications by April 2010 and probableissuance of licenses by June 2010."

gefällt mir auch überhaupt nicht.

Uran ist eben ein sehr heikles thema.. da sind wir dann doch im Becken am besten aufgehoben.

letztlich nutzt es nichts wenn alle eckdaten hervorragend sind und sich die permits auf ewig hinziehen (kennt man ja auch bei anderen geschichten wie Canadian Zinc z.b. und da geht´s nur um zink und silber)

Denison schließt C$ 82 Millionen Finanzierung ab

http://finance.yahoo.com/news/Denison-Mines-Corp-Closes-CDN-…

Denison Mines Corp. Closes CDN $82,000,000 Bought Deal Financing

FANTOMAS

http://finance.yahoo.com/news/Denison-Mines-Corp-Closes-CDN-…

Denison Mines Corp. Closes CDN $82,000,000 Bought Deal Financing

FANTOMAS

Pitchstone kündigt Finanzierung an: 1,25 Mio. Aktien zu C$ 0,40 für C$ 500.000, mit Warrants zu C$ 0,60 bzw. C$ 0,80

http://finance.yahoo.com/news/Pitchstone-Announces-500000-cc…

Pitchstone Announces $500,000 Financing

FANTOMAS

http://finance.yahoo.com/news/Pitchstone-Announces-500000-cc…

Pitchstone Announces $500,000 Financing

FANTOMAS

Mickey Fulp zu Uran, The Energy Report, 18.06.09:

http://www.stockhouse.com/Bullboards/MessageDetail.aspx?s=UR…

Mickey Fulp, Mercenary Geologist: The Demand is There

Well-known and highly regarded throughout the mining and exploration community, Mercenary Geologist Mickey Fulp returns to discuss the brightening prospects for uranium and natural gas with The Energy Report readers. A Certified Professional Geologist, Mickey says he's comfortable focusing his hard-earned dollars in junior and mid-tier uranium companies working in the U.S. and Canada.

The Energy Report: Mickey, you have followed uranium in the past. What’s your thinking about uranium now? Is it going to make that comeback? That famous newsletter writer, who is now the original rare earth element bug, is looking at uranium and saying it’s pretty positive. Do you agree?

Mickey Fulp: I agree wholeheartedly. I've liked this sector since before the first boom in '06. Uranium was the proverbial canary in the coalmine for the commodities crash, but the sector has shown recent strength. The long-term contracts price is $65 a pound. Short-term contracts are at $50 a pound. The uranium sector is still, from a market valuation, a little beaten up, but it’s been looking up, and I have a couple of favorite companies.

I recently visited Hathor Exploration’s (TSX.V:HAT) Roughrider project and was impressed with the grade and the pounds of uranium that they’ve drilled. In the U.S., I follow Strathmore Minerals Corp. (TSX.V:STM) (OTCBB:STHJF)and have for over two years. It has about 160 million pounds of resources in the ground. It came off a late winter low at $0.22, is currently trading at about $0.50, and has been as high as $0.82 in the last couple of months. I like their story. I also would be looking at others in Wyoming and Texas that are potential near-term producers with in-situ recovery deposits. I think we can expect new uranium production in Wyoming and Texas sometime within the next two years.

TER: Can you share with us what companies are mining or drilling in the Wyoming and Texas areas?

MF: I would look at Uranerz Energy Corporation (TSX:URZ) (NYSE.A:URZ) and Ur-Energy Inc. (TSX:URE) in Wyoming and perhaps Uranium Energy Corp. (NYSE.A:UEC), which has the Goliad deposit in South Texas. These are all companies in the advanced permitting stage. The Nuclear Regulatory Commission threw a bit of kink in the works recently, though it probably got more negative press than really deserved. They issued a ruling in late May saying they’re going to require project-specific Environmental Impact Statements (EIS); whereas before they were just going to issue a Generic Environmental Impact Statement for all ISR producers. So companies may face some delays, because they go directly to an EIS procedure vs. what was going to be an Environmental Assessment (EA) before. Now they all have to do a site-specific EIS, so it may have put a few months' delay on some of these projects, but I think it clarifies the situation because an EA might have generated requirement for a subsequent EIS. It makes the permitting requirements more straightforward. You know what you have to do and you can generate a more reliable time frame to get it done, the uncertainty is lessened.

TER: When we interviewed you for The Gold Report, you also were intrigued with emerging environments and the prospect of more major finds in areas that haven’t been as thoroughly explored or drilled. Would you expect anything in the uranium sector to come about in these emerging environments, do we even need to go there, or just stay in Wyoming and/or Texas?

MF: In the U.S. we have 104 of the world’s 430 or so nuclear reactors. We use about one-third of the world’s uranium every year. I’m very comfortable staying in the U.S., specifically Wyoming, Texas, and then in a little longer-term scenario, New Mexico.

In terms of geopolitical risk in the uranium sector, there have been some very negative developments over the last or three to four weeks. In Kazakhstan, the head of Kazatomprom was arrested and charged with making illegal and corrupt deals with unnamed foreign companies for uranium production —so speculation is that probably involves Uranium One (TSX:UUU). This incident leads to some intriguing questions. When is a deal actually a done deal? Is the Kazakhstan government on the road to increasing nationalization of its uranium production? We’ve seen this happen before in Kazakhstan in the gold sector. Kazakhstan is the world’s third-largest uranium producer. So that’s a bit scary for the West.

Recently in Niger, which is the world’s fifth-largest uranium producer, the president tried to get a referendum to pass parliament to allow him to run for a third consecutive term. That referendum was not passed and so he simply dissolved parliament. The point I make is there is considerable geopolitical risk to the West with its dependency on emerging market countries for a significant portion of uranium supply.

In the U.S., we have known deposits that the economics were derailed when our uranium industry crashed in the early '80s. They are basically sitting there, drilled out and waiting to be permitted, developed, and mined. So now it becomes a matter of the time period to permit the deposits. All in all, I’m comfortable focusing my hard-earned dollars in junior and mid-tier uranium companies working in the U.S. and Canada.

TER: Mickey, can you talk a little bit about the demand for uranium? Nuclear is still a nasty word, even though the U.S. is looking at alternative, cleaner sources of energy. I don’t think there are many new nuclear reactors on the dockets in the U.S. compared to countries like China and India. So are we really expecting to see these companies—Hathor, Strathmore, and the Wyoming and Texas companies—appreciate in value if the demand is not appreciating in value in North America?

MF: The demand is there. The mined supply every year is somewhere around 110 to120 million pounds. The current world demand is somewhere around 160 to 170 million pounds. So in terms of mine production, the world is at a one-third shortfall on a yearly basis. Over the last few years, these shortfalls have been supplied in large part by the Russians and their "Megatons to Megawatts" program, which converts highly enriched weapons-grade uranium into low-enriched uranium suitable for reactors. The Russians have stated publicly that sales to the U.S. are going to end in 2013. Currently, the U.S. uses somewhere around 55 million pounds of uranium per year and produces less than 4 million pounds. The demand obviously is there. We have not built a nuclear reactor in the U.S. for years, but we have increased the efficiency and increased units within our existing nuclear power plants, so that our demand has been going up. As an energy supplier, uranium is just about as green as you can get. It leaves no carbon footprint. It’s safe. The Three Mile Island scare was media-driven hype, and we all realize that now. Increasingly, the green sector is looking at nuclear energy as a viable, clean, alternative source in the United States.

TER: Are there other areas in the energy sector that are interesting to you?

MF: I continue to follow the natural gas sector. It’s been beaten up even more since March, as the yearly lows in natural gas are usually some time in the late spring or early summer; Henry Hub natural gas is at $3.75. Interestingly, November futures are at $5.00 and a lot of that is seasonal speculation as we get into the heating season in the northern tier of the United States. I continue to watch this sector.

There are some buys out there, no doubt, but the question in the natural gas sector is when is the price going to turn around? Is it going to be six months? Is it going to be 12 months or 18 months? Or could it even be two years? There was a lot of drill success in the shale gas arena in the U.S in the past couple of years, so we’re looking at a bit of a supply imbalance right now. But most of the shale gas producers are not going to make money at $3.75. It’s a sector that I continue to watch but have not yet moved into it; I’m casting about for the right companies. Many of these companies are debt ridden, so you probably want to find one that has manageable debt and has production ready to go, perhaps even shut in, and then it becomes a contrarian play. Buy at low volume when nobody else is buying the stock, and sell when the boom comes. Much like the gold and uranium sectors were in December—we knew that they were beaten up beyond imagination and that it couldn’t continue that way and the smart money got in then—and look at the returns we’ve had on some of these companies. That’s the way I view the gas sector right now.

TER: So gas is going to turn around; you just don’t know when and you need to find the right plays in that sector.

MF: Right. I’m going to be in before gas turns around, but at this point I’m looking for the right companies to get into. I’m own a couple of natural gas companies, Alberta producers, but I’ve been in them for a long time. I’m looking for undervalued stories right now.

TER: Very interesting. Maybe you can share them with us when you find them?

MF: Well, I’d certainly be glad to do that. Mickey, the Mercenary Geologist, hasn’t waded into this sector yet, but I really think it’s time. I’m just trying to do some due diligence and find out which companies I want to put some high-risk capital into. Ultimately, I think you can’t go wrong in this sector as long as you buy production and don’t buy companies that end up going bankrupt before it turns. That, of course, is the risk. The oil and gas sector is fairly debt ridden as opposed to the junior gold sector, which raises nearly all of its money through equity financing.