Gewinnerbranchen der Jahre 2006 bis 2040 (Seite 929)

eröffnet am 10.12.06 16:57:17 von

neuester Beitrag 16.02.24 09:33:08 von

neuester Beitrag 16.02.24 09:33:08 von

Beiträge: 94.068

ID: 1.099.361

ID: 1.099.361

Aufrufe heute: 8

Gesamt: 3.535.964

Gesamt: 3.535.964

Aktive User: 0

Top-Diskussionen

| Titel | letzter Beitrag | Aufrufe |

|---|---|---|

| vor 1 Stunde | 7229 | |

| vor 27 Minuten | 5429 | |

| heute 17:09 | 5142 | |

| vor 45 Minuten | 3555 | |

| vor 32 Minuten | 2915 | |

| vor 23 Minuten | 2820 | |

| vor 34 Minuten | 2813 | |

| vor 41 Minuten | 2647 |

Meistdiskutierte Wertpapiere

| Platz | vorher | Wertpapier | Kurs | Perf. % | Anzahl | ||

|---|---|---|---|---|---|---|---|

| 1. | 3. | 18.128,14 | -0,27 | 191 | |||

| 2. | 5. | 195,38 | +16,10 | 95 | |||

| 3. | 4. | 2.341,21 | +0,15 | 53 | |||

| 4. | 6. | 7,8800 | +7,21 | 47 | |||

| 5. | 2. | 0,7550 | -36,02 | 43 | |||

| 6. | 19. | 64,30 | -5,09 | 39 | |||

| 7. | 39. | 15,140 | -9,27 | 32 | |||

| 8. | 21. | 6,8040 | +0,65 | 28 |

Beitrag zu dieser Diskussion schreiben

Antwort auf Beitrag Nr.: 59.344.090 von clearasil am 02.12.18 12:44:11Galapagos CEO says a sale to Gilead is 50% likely

5 November 2018 - 12:03

The daily De Telegraaf on Saturday published a statement by Onno van De Stolpe, CEO of Belgium-based biotech Galapagos, according to which the group is 50% likely to be acquired by a competitor over the next 10 years. The chief executive considers California-based Gilead, which is already among its minority stakeholders, as the most likely buyer of Galapagos’. Moreover, the Dutch manager estimates that his company, currently valued at €5bn, will soon reach a capitalization comparable to Philips’ one, that is €30bn. Going forward, Galapagos’ success will almost completely depend on its investigational rheumatoid arthritis treatment filgotinib, expected to be launched on the market in 2020.

5 November 2018 - 12:03

The daily De Telegraaf on Saturday published a statement by Onno van De Stolpe, CEO of Belgium-based biotech Galapagos, according to which the group is 50% likely to be acquired by a competitor over the next 10 years. The chief executive considers California-based Gilead, which is already among its minority stakeholders, as the most likely buyer of Galapagos’. Moreover, the Dutch manager estimates that his company, currently valued at €5bn, will soon reach a capitalization comparable to Philips’ one, that is €30bn. Going forward, Galapagos’ success will almost completely depend on its investigational rheumatoid arthritis treatment filgotinib, expected to be launched on the market in 2020.

zu GILD/GLPG (im Bestand):

Gilead can now attempt at takeover of Galapagos

29 November 2018 - 16:43

The Dutch economic and financial daily Het Financieele Dagblad today has reviewed the press release issued by Belgian-Dutch biotech company Galapagos to announce that Van Herk Investments’ stake in the company has decreased to 9.91% due to dilution. As a direct result, the company is now vulnerable to a takeover by Gilead, which already owns 13% of the group’s shares.

Indeed, pursuant to the Belgian law, shareholders have to own more than 10% shares to oppose a takeover attempt. Now that the only shareholder with more than 10% of Galapagos’ shares is the same Californian biotech, it can start an acquisition program any time now. Galapagos’ shares rose over 5% (Amsterdam) after the announcement, while Gilead’s rose 3% (NASDAQ).

Gilead can now attempt at takeover of Galapagos

29 November 2018 - 16:43

The Dutch economic and financial daily Het Financieele Dagblad today has reviewed the press release issued by Belgian-Dutch biotech company Galapagos to announce that Van Herk Investments’ stake in the company has decreased to 9.91% due to dilution. As a direct result, the company is now vulnerable to a takeover by Gilead, which already owns 13% of the group’s shares.

Indeed, pursuant to the Belgian law, shareholders have to own more than 10% shares to oppose a takeover attempt. Now that the only shareholder with more than 10% of Galapagos’ shares is the same Californian biotech, it can start an acquisition program any time now. Galapagos’ shares rose over 5% (Amsterdam) after the announcement, while Gilead’s rose 3% (NASDAQ).

Antwort auf Beitrag Nr.: 59.341.634 von anton7 am 01.12.18 17:46:55interessante Firma - aber bis in 2020 hinein steigende verluste - sind die 4 traders -zahlen hier wiedermal nicht belastbar?

https://www.marketscreener.com/NUTANIX-INC-31497437/news/Nut…

seek.a. author meint:

As NTNX continues to shed their hardware sales, we should expect overall margins to improve, in terms of both gross and operating. In addition, as NTNX continues to scale, they should be able to decrease their operating expenses, such as R&D and S&M. The one caveat with this (which I discussed in a previous article) is that the quicker NTNX loses their hardware sales, their revenue growth will be artificially lower. This was seen this quarter as overall revenue grew only 14%, compared to software/support revenue growth of 44%. However, this means gross margins would come in higher than expected, which was also seen the past two quarters.

NTNX’s customer cohort is also a big driver of their future growth. Traditionally, they have focused on the enterprise market, leaving the middle market companies largely untouched. However, NTNX has placed a lot more emphasis on the middle market and has initiated several internal sales programs to place more emphasis on this large market opportunity.

At the end of Q1, NTNX had nearly 11,500 customers, with 720 of the Global 2,000 customers. Growing the middle market cohort will give NTNX a great opportunity to become the mainstream HCI name for companies of all sizes. In addition, NTNX experiences significant revenue growth from existing customers. This is demonstrated by customers who have been with NTNX for more than 18 months on average spend over 4x their initial purchase. Global 2,000 customers have an even stronger traction, with total lifetime purchases increasing 10.6x compared to the initial purchase. As NTNX continues to penetrate both the enterprise and middle market customer base, they will be able to have better insight into their revenue, much of which is rather sticky.

https://seekingalpha.com/article/4225014-nutanix-another-str…" target="_blank" rel="nofollow ugc noopener">

https://seekingalpha.com/article/4225014-nutanix-another-str…

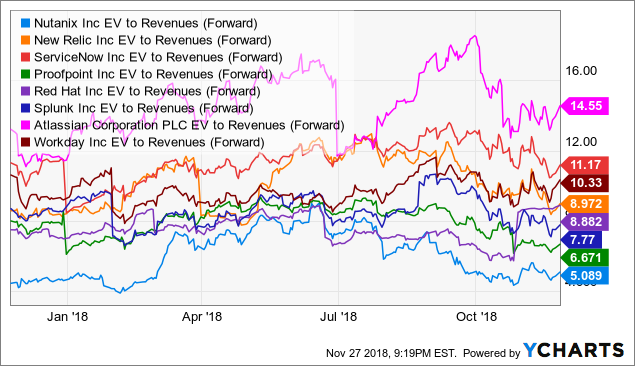

In order to properly value NTNX, I looked at a variety of fast-growth software companies who trade at premium revenue multiples compared to the greater market. The list of peers include: New Relic (NEWR), ServiceNow (NOW), Proofpoint (PFPT), Red Hat (RHT), Splunk (SPLK), Atlassian (TEAM), and Workday (WDAY). All of the peers are considered leaders in their respective industries, hosting both strong revenue growth rates and consistently high gross margins.

With NTNX trading at 4.0x FY20 revenue, I believe this multiple could expand closer to the average peer group over the next 18-24 months. Assuming NTNX trades at a 7.0x multiple, still below the current peer group average of nearly 10.0x, NTNX would have an enterprise value of ~$11.9 billion. Backing out a more conservative $500 million of net cash results in a market cap of ~$12.4 billion. Using a conservative 190 million shares, this results in a price target of $65, a 45% upside to Tuesday's after-hours price of $44.50.

I believe NTNX remains very undervalued given the company's transition to a software-only model and significant margin expansion. As the company completes this transition over the next 9-12 months, investors will begin to value NTNX as a software-only company, which typically comes with a higher revenue multiple premium.

Risks to NTNX include a slower than expected transition to software-only sales, though it would have a slight benefit to revenue growth, and would negatively impact gross margins. The emergence of more competitors would also hamper NTNX’s growth.

interessant wäre hierzu eine Meinung von oberkassel und investival ...

https://www.marketscreener.com/NUTANIX-INC-31497437/news/Nut…

seek.a. author meint:

As NTNX continues to shed their hardware sales, we should expect overall margins to improve, in terms of both gross and operating. In addition, as NTNX continues to scale, they should be able to decrease their operating expenses, such as R&D and S&M. The one caveat with this (which I discussed in a previous article) is that the quicker NTNX loses their hardware sales, their revenue growth will be artificially lower. This was seen this quarter as overall revenue grew only 14%, compared to software/support revenue growth of 44%. However, this means gross margins would come in higher than expected, which was also seen the past two quarters.

NTNX’s customer cohort is also a big driver of their future growth. Traditionally, they have focused on the enterprise market, leaving the middle market companies largely untouched. However, NTNX has placed a lot more emphasis on the middle market and has initiated several internal sales programs to place more emphasis on this large market opportunity.

At the end of Q1, NTNX had nearly 11,500 customers, with 720 of the Global 2,000 customers. Growing the middle market cohort will give NTNX a great opportunity to become the mainstream HCI name for companies of all sizes. In addition, NTNX experiences significant revenue growth from existing customers. This is demonstrated by customers who have been with NTNX for more than 18 months on average spend over 4x their initial purchase. Global 2,000 customers have an even stronger traction, with total lifetime purchases increasing 10.6x compared to the initial purchase. As NTNX continues to penetrate both the enterprise and middle market customer base, they will be able to have better insight into their revenue, much of which is rather sticky.

https://seekingalpha.com/article/4225014-nutanix-another-str…" target="_blank" rel="nofollow ugc noopener">

https://seekingalpha.com/article/4225014-nutanix-another-str…

In order to properly value NTNX, I looked at a variety of fast-growth software companies who trade at premium revenue multiples compared to the greater market. The list of peers include: New Relic (NEWR), ServiceNow (NOW), Proofpoint (PFPT), Red Hat (RHT), Splunk (SPLK), Atlassian (TEAM), and Workday (WDAY). All of the peers are considered leaders in their respective industries, hosting both strong revenue growth rates and consistently high gross margins.

With NTNX trading at 4.0x FY20 revenue, I believe this multiple could expand closer to the average peer group over the next 18-24 months. Assuming NTNX trades at a 7.0x multiple, still below the current peer group average of nearly 10.0x, NTNX would have an enterprise value of ~$11.9 billion. Backing out a more conservative $500 million of net cash results in a market cap of ~$12.4 billion. Using a conservative 190 million shares, this results in a price target of $65, a 45% upside to Tuesday's after-hours price of $44.50.

I believe NTNX remains very undervalued given the company's transition to a software-only model and significant margin expansion. As the company completes this transition over the next 9-12 months, investors will begin to value NTNX as a software-only company, which typically comes with a higher revenue multiple premium.

Risks to NTNX include a slower than expected transition to software-only sales, though it would have a slight benefit to revenue growth, and would negatively impact gross margins. The emergence of more competitors would also hamper NTNX’s growth.

interessant wäre hierzu eine Meinung von oberkassel und investival ...

Antwort auf Beitrag Nr.: 59.342.003 von Simonswald am 01.12.18 19:23:26 Hä? Jetzt doch keine weitere Outperformance mehr? Diese Wendungen gehen mir alle zu schnell, so flexibel bin ich nicht mehr.  Ohne Tech (fast 25% Gewichtung)kann der Markt insgesamt kaum nach oben.

Ohne Tech (fast 25% Gewichtung)kann der Markt insgesamt kaum nach oben.

meine Meinung ist die gleiche gebleiben, etwas outperformance im rebound, in der nächsten Schwäche wieder Abverkauf, die alten techfavoriten werden hinken.

stark: z.B TTD, VEEV, BEAT, die Paymentaktien z.B. GDOT, ABBV, GILD mit Lebenszeichen, EW, ISRG.

z.B. GDOT, ABBV, GILD mit Lebenszeichen, EW, ISRG.

schwach: überspekulierte Momentum-Altfavoriten z.B. ABMD, ALGN.

2019 wird vor allem volatil.

Ohne Tech (fast 25% Gewichtung)kann der Markt insgesamt kaum nach oben.

Ohne Tech (fast 25% Gewichtung)kann der Markt insgesamt kaum nach oben.meine Meinung ist die gleiche gebleiben, etwas outperformance im rebound, in der nächsten Schwäche wieder Abverkauf, die alten techfavoriten werden hinken.

stark: z.B TTD, VEEV, BEAT, die Paymentaktien

z.B. GDOT, ABBV, GILD mit Lebenszeichen, EW, ISRG.

z.B. GDOT, ABBV, GILD mit Lebenszeichen, EW, ISRG.schwach: überspekulierte Momentum-Altfavoriten z.B. ABMD, ALGN.

2019 wird vor allem volatil.

***

https://www.marketwatch.com/story/these-numbers-show-suze-or…

Hier machen sie die Leute verrückt... need 5 Million to retire … wüsst ich echt nicht wofür... mir reicht eine Drittel Mio... immerhin mach ich mit SmallValue doch easy 15% pa...

***

big tech ist vorerst durch.

Hä? Jetzt doch keine weitere Outperformance mehr? Diese Wendungen gehen mir alle zu schnell, so flexibel bin ich nicht mehr.

Ohne Tech (fast 25% Gewichtung)kann der Markt insgesamt kaum nach oben.

***

Bilanz November:

Large besser als Small

Value besser als Growth

Healthcare, Utilities stark

Öl, Tech schwach

https://www.marketwatch.com/story/these-numbers-show-suze-or…

Hier machen sie die Leute verrückt... need 5 Million to retire … wüsst ich echt nicht wofür... mir reicht eine Drittel Mio... immerhin mach ich mit SmallValue doch easy 15% pa...

***

big tech ist vorerst durch.

Hä? Jetzt doch keine weitere Outperformance mehr? Diese Wendungen gehen mir alle zu schnell, so flexibel bin ich nicht mehr.

Ohne Tech (fast 25% Gewichtung)kann der Markt insgesamt kaum nach oben.

***

Bilanz November:

Large besser als Small

Value besser als Growth

Healthcare, Utilities stark

Öl, Tech schwach

Trading Spotlight

Antwort auf Beitrag Nr.: 59.341.580 von Simonswald am 01.12.18 17:21:38Gestrige SP500 Avance bemerkenswert angeführt von defensiven Sektoren wie Pharma und Staples

an pharma und medtechmangel leide ich nicht.

big tech ist vorerst durch.

an pharma und medtechmangel leide ich nicht.

big tech ist vorerst durch.

Antwort auf Beitrag Nr.: 59.341.571 von Simonswald am 01.12.18 17:16:57 mein Dollarexposure reduzieren und aus steuerlichen Gründen Gewinne sichern.

das kann ich nachvollziehen.

ich jedenfalls bin vorerst weiter voll investiert.

das kann ich nachvollziehen.

ich jedenfalls bin vorerst weiter voll investiert.

Nutanix ist glaube ich hier noch nciht erwähnt worden. Hier ein Artikel dazu:

https://thedlf.de/nutanix-aktie-zahlen-q1-fy19/?fbclid=IwAR0…

https://thedlf.de/nutanix-aktie-zahlen-q1-fy19/?fbclid=IwAR0…

Gestrige SP500 Avance bemerkenswert angeführt von defensiven Sektoren wie Pharma und Staples, Tech hat (vorerst) seine Leader-Funktion abgegeben.

das kann ich alles nicht nachvollziehen.

Das wiederum kann ich nachvollziehen.

Ich wollte halt mein Depot um 10-15% reduzieren, mein Dollarexposure reduzieren und aus steuerlichen Gründen Gewinne sichern. Da musste ich halt einige grössere Depotpositionen auflösen.

sanofi hat weiter platz nach oben.

Durchaus möglich, aber ich hätte die aus steuerlichen Gründen eh vor der Divi-Zahlung verkauft. Kurzfristig sehen Novartis und GSK stärker aus, die ich sonst überlegt habe.

vivo bekommt eine Zulassung:

Interessant, hat den Markt aber nicht wesentlich interessiert.

fds ist qualität pur, die nach oben läuft.

Das schon - erstaunlich alleine schon wie viele Daten bspw comdirect von denen bezieht. Aber die Umsatz- und Gewinndynamik ist schwächer als auch schon. Zudem das KGV nach meiner Rechnung unschön von üblichen 20-25 auf 30 hochgelaufen. Prädesitiniert für Seitwärtsphase. Als Finanzdienstleister zudem von möglicher Kapitalmarktbaisse ev. überproportionanl betroffen.

für mentalstopps geeigneter doppelboden im markt.

Das wiederum kann ich nachvollziehen.

Ich wollte halt mein Depot um 10-15% reduzieren, mein Dollarexposure reduzieren und aus steuerlichen Gründen Gewinne sichern. Da musste ich halt einige grössere Depotpositionen auflösen.

sanofi hat weiter platz nach oben.

Durchaus möglich, aber ich hätte die aus steuerlichen Gründen eh vor der Divi-Zahlung verkauft. Kurzfristig sehen Novartis und GSK stärker aus, die ich sonst überlegt habe.

vivo bekommt eine Zulassung:

Interessant, hat den Markt aber nicht wesentlich interessiert.

fds ist qualität pur, die nach oben läuft.

Das schon - erstaunlich alleine schon wie viele Daten bspw comdirect von denen bezieht. Aber die Umsatz- und Gewinndynamik ist schwächer als auch schon. Zudem das KGV nach meiner Rechnung unschön von üblichen 20-25 auf 30 hochgelaufen. Prädesitiniert für Seitwärtsphase. Als Finanzdienstleister zudem von möglicher Kapitalmarktbaisse ev. überproportionanl betroffen.

für mentalstopps geeigneter doppelboden im markt.