Dividenden Strategie (Seite 63)

eröffnet am 18.10.11 11:57:29 von

neuester Beitrag 07.05.23 11:51:33 von

neuester Beitrag 07.05.23 11:51:33 von

Beiträge: 742

ID: 1.169.703

ID: 1.169.703

Aufrufe heute: 1

Gesamt: 96.004

Gesamt: 96.004

Aktive User: 0

Top-Diskussionen

| Titel | letzter Beitrag | Aufrufe |

|---|---|---|

| gestern 11:52 | 2141 | |

| vor 46 Minuten | 2060 | |

| gestern 22:26 | 1282 | |

| 08.05.24, 11:56 | 1278 | |

| vor 1 Stunde | 1121 | |

| vor 32 Minuten | 1087 | |

| vor 1 Stunde | 960 | |

| vor 49 Minuten | 886 |

Meistdiskutierte Wertpapiere

| Platz | vorher | Wertpapier | Kurs | Perf. % | Anzahl | ||

|---|---|---|---|---|---|---|---|

| 1. | 1. | 18.772,85 | +0,46 | 131 | |||

| 2. | 3. | 0,2170 | +3,33 | 125 | |||

| 3. | Neu! | 8,2570 | +96,67 | 108 | |||

| 4. | 4. | 156,46 | -2,31 | 103 | |||

| 5. | 14. | 5,7540 | -2,18 | 56 | |||

| 6. | 2. | 0,2980 | -3,87 | 50 | |||

| 7. | 5. | 2,3720 | -7,54 | 49 | |||

| 8. | 7. | 6,8000 | +2,38 | 38 |

Beitrag zu dieser Diskussion schreiben

Eine Kriegserklärung:

Tomorrow And Tomorrow And Tomorrow

From Mark Grant, author of Financial Commentary "Out of the Box"

"Tomorrow and tomorrow and tomorrow

creeps in this petty pace from day to day

to the last syllable of recorded time.

And all our yesterdays have lighted fools

the way to dusty death.

Out, out brief candle.

Life’s but a walking shadow, a poor player

that struts and frets his hour upon the stage,

and then is heard no more.

It is a tale told by an idiot, full of sound and fury,

signifying nothing."

-Macbeth, Act 5, Scene 5

Today, as I look at the markets, is a day signified by foolishness. Today the Euro is up, equity futures are up and the markets believe that a sustainable debt solution for Greece has been found and will be agreed upon later today. Such silliness, such idiocy; as investors believe the mockery dribbled out of Brussels and Berlin. Yet I smile, I have waited for over two years now and tomorrow I shall certainly smile because what will be decided will not be what anyone expects and because there is no choice now except to make the decisions that must be made with the looming reality of the Greek debt pay-out on March 20. Today is marked by misguided hope but tomorrow will be marked by quite a different reality.

It is not that I can predict today’s outcome any better than anyone else. When Finance Ministers convene and when politics is brought to bear the burdens and prejudices of their home countries will be brought to the table along with their ambitions and their desires to be re-elected. Grand designs give way to grim realities and exaggerated hopes and prayers will no longer suffice; of this I am quite certain. The road has run its course and now a direction must be taken, a choice made, and the rambling at a shuffled pace going nowhere is no longer sufficient. Today, finally, choices will be made and laid on the table to be examined in the sun of a different day and what was has ended; and tomorrow will mark a new beginning that cannot be controverted by political rhetoric or washed over by grand assurances signifying nothing except to lead the sheep into the next pasture. Today will be one thing; tomorrow will be another.

“Yesterday is history, tomorrow is a mystery, but today is a gift, that's why we call it the present.”

-Winnie the Pooh

Once we see what Europe is really going to do, not what they have told us they might do, the real show gets underway. Everything up till now was just a preamble, a mincemeat of words flowing like a unsubstantiated river from mouths full of fluff, orated by the deceptors and laid out on a table where cheese was pointed to as Prime Rib and where radishes were sworn to be asparagus but these days end tomorrow and as sure as the sun rises in the East; tomorrow will arrive.

There is the collateral for Finland, the CDS trigger, the “Collective Action Clause, who is really represented by the IIF, the $20Bn budget shortfall, the contribution of the IMF, the methodology for handing Greece the money, possible further notions that Greece has not met its commitments, law suits on the way for the ECB’s subordination of private bond holders and for the “haircut” coercion where different classes of investors have been retroactively applied and for the retroactive implementation of some “CAC”. All of these things are forthcoming regardless of what we find in Europe’s pronouncements so that the lens laid over today’s sun will tomorrow be removed and the glare of the light will be startling in its clarity and reflection.

Tomorrow the bond investors not manipulated by the European authorities return to the playing field and the reaction begins to the ECB swapping their Greek bonds for new ones to the detriment of everyone else. It may be that with the new day that there will be a brief rally as some deal is done but it will be short-lived if it occurs I predict. I can report with certain knowledge that a good number of bond investors are angry and they have realized, like I have, that if the ECB can do this with a “Collective Action Clause” that they can do this with any other clause and if they can do this with Greece they can do it with any other country. Tomorrow marks the day when the hidden cards are turned over and the bluff is revealed. Tomorrow will be a defining moment and the definition will spark a reaction that can only be guessed at presently and my guess is retribution and vengeance and the furies unleashed. What has been promised will not be what is delivered as the unraveled flag of reality is finally shown to one and all.

Gird for Battle.

“I've developed a new philosophy... I only dread one day at a time.”

-Charlie Brown

Tomorrow And Tomorrow And Tomorrow

From Mark Grant, author of Financial Commentary "Out of the Box"

"Tomorrow and tomorrow and tomorrow

creeps in this petty pace from day to day

to the last syllable of recorded time.

And all our yesterdays have lighted fools

the way to dusty death.

Out, out brief candle.

Life’s but a walking shadow, a poor player

that struts and frets his hour upon the stage,

and then is heard no more.

It is a tale told by an idiot, full of sound and fury,

signifying nothing."

-Macbeth, Act 5, Scene 5

Today, as I look at the markets, is a day signified by foolishness. Today the Euro is up, equity futures are up and the markets believe that a sustainable debt solution for Greece has been found and will be agreed upon later today. Such silliness, such idiocy; as investors believe the mockery dribbled out of Brussels and Berlin. Yet I smile, I have waited for over two years now and tomorrow I shall certainly smile because what will be decided will not be what anyone expects and because there is no choice now except to make the decisions that must be made with the looming reality of the Greek debt pay-out on March 20. Today is marked by misguided hope but tomorrow will be marked by quite a different reality.

It is not that I can predict today’s outcome any better than anyone else. When Finance Ministers convene and when politics is brought to bear the burdens and prejudices of their home countries will be brought to the table along with their ambitions and their desires to be re-elected. Grand designs give way to grim realities and exaggerated hopes and prayers will no longer suffice; of this I am quite certain. The road has run its course and now a direction must be taken, a choice made, and the rambling at a shuffled pace going nowhere is no longer sufficient. Today, finally, choices will be made and laid on the table to be examined in the sun of a different day and what was has ended; and tomorrow will mark a new beginning that cannot be controverted by political rhetoric or washed over by grand assurances signifying nothing except to lead the sheep into the next pasture. Today will be one thing; tomorrow will be another.

“Yesterday is history, tomorrow is a mystery, but today is a gift, that's why we call it the present.”

-Winnie the Pooh

Once we see what Europe is really going to do, not what they have told us they might do, the real show gets underway. Everything up till now was just a preamble, a mincemeat of words flowing like a unsubstantiated river from mouths full of fluff, orated by the deceptors and laid out on a table where cheese was pointed to as Prime Rib and where radishes were sworn to be asparagus but these days end tomorrow and as sure as the sun rises in the East; tomorrow will arrive.

There is the collateral for Finland, the CDS trigger, the “Collective Action Clause, who is really represented by the IIF, the $20Bn budget shortfall, the contribution of the IMF, the methodology for handing Greece the money, possible further notions that Greece has not met its commitments, law suits on the way for the ECB’s subordination of private bond holders and for the “haircut” coercion where different classes of investors have been retroactively applied and for the retroactive implementation of some “CAC”. All of these things are forthcoming regardless of what we find in Europe’s pronouncements so that the lens laid over today’s sun will tomorrow be removed and the glare of the light will be startling in its clarity and reflection.

Tomorrow the bond investors not manipulated by the European authorities return to the playing field and the reaction begins to the ECB swapping their Greek bonds for new ones to the detriment of everyone else. It may be that with the new day that there will be a brief rally as some deal is done but it will be short-lived if it occurs I predict. I can report with certain knowledge that a good number of bond investors are angry and they have realized, like I have, that if the ECB can do this with a “Collective Action Clause” that they can do this with any other clause and if they can do this with Greece they can do it with any other country. Tomorrow marks the day when the hidden cards are turned over and the bluff is revealed. Tomorrow will be a defining moment and the definition will spark a reaction that can only be guessed at presently and my guess is retribution and vengeance and the furies unleashed. What has been promised will not be what is delivered as the unraveled flag of reality is finally shown to one and all.

Gird for Battle.

“I've developed a new philosophy... I only dread one day at a time.”

-Charlie Brown

PIMCO @PIMCO

Gross: #ECB subordinates all #Greek debt holders & in so doing subordinates all holders of Euroland sovereign debt.

Gross: #ECB subordinates all #Greek debt holders & in so doing subordinates all holders of Euroland sovereign debt.

Trading Spotlight

A Very Different Take On The "Iran Barters Gold For Food" Story

http://www.zerohedge.com/news/very-different-take-iran-barte…

http://www.zerohedge.com/news/very-different-take-iran-barte…

http://www.zerohedge.com/news/guest-post-do-we-really-know-g…

Guest Post: Do We Really Know Greece's Default Will Be Orderly?

CDS - Problematik

Sovereign CDS – Hellenic Republic CDS

http://seekingalpha.com/instablog/948480-peter-tchir/239727-…

Guest Post: Do We Really Know Greece's Default Will Be Orderly?

CDS - Problematik

Sovereign CDS – Hellenic Republic CDS

http://seekingalpha.com/instablog/948480-peter-tchir/239727-…

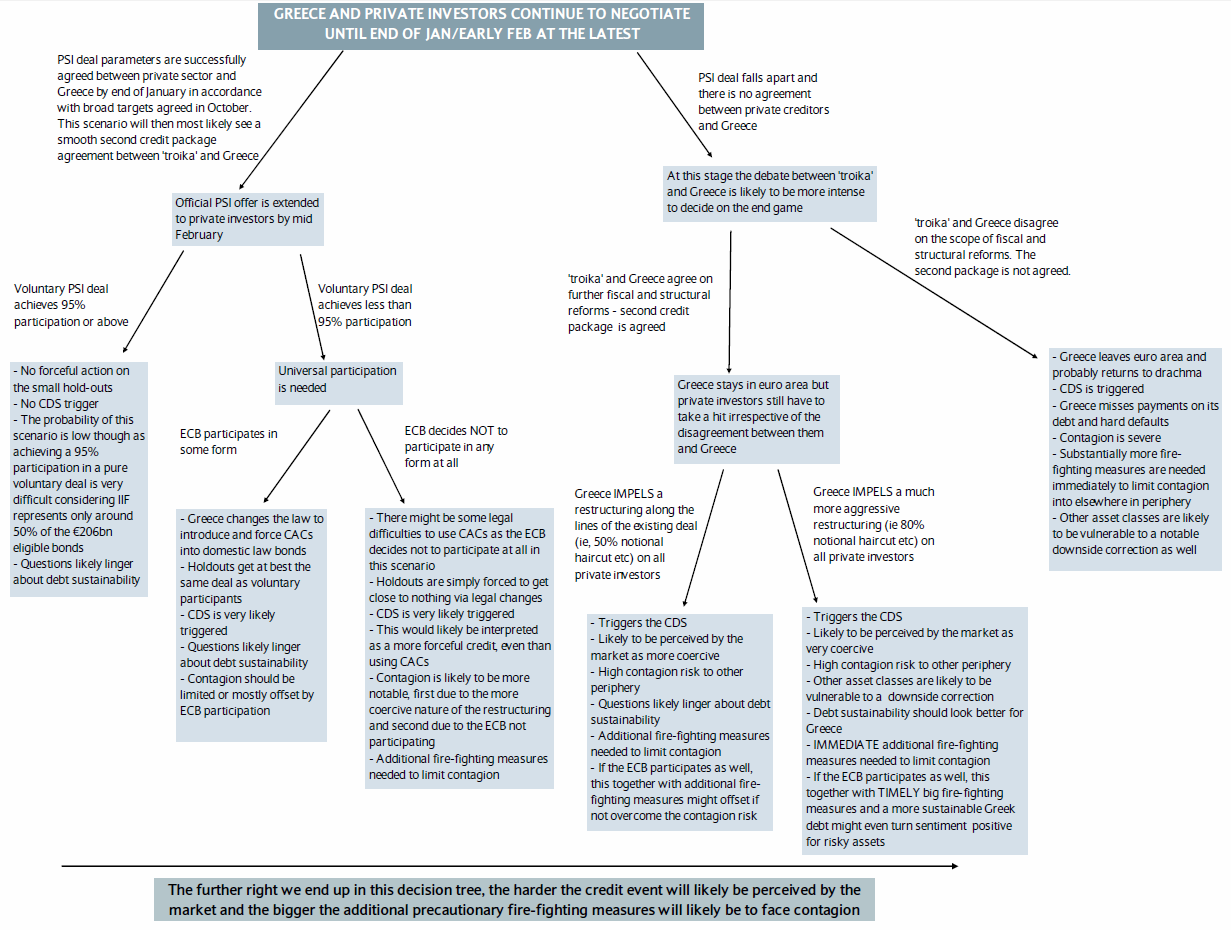

EZB bailout->PSI failure->CAC action->credit event->CDS triggering~> banks collapse-> market turmoil

Credit Suisse The Sequel: "Probability Of The Largest Disorderly Default Loss In History On March 20 Has Increased"

A week ago we presented an excerpt from Credit Suisse's most excellent piece "The Flaw" - merely the latest in one of the best overviews of the neverending Greek soap opera by William Porter. Yet every soap opera eventually ends. Although when it comes to Nielsen ratings, the denouement is usually a whimper. In the case of Greece, it will be anything but. Yet listening to the daily cacafony of din from Europe's leaders, who are likely more clueless than the average reader as to what is really going on, one may be left with the impression that there is a simple solution to the problem, and Greece may be "saved... in hours." It can't. In fact, as of today, Porter's s conclusion is: "we are left with a sense that the probability of delivering the largest default loss in history in a disorderly way on or before 20 March has increased relative to doing so in an orderly way."

....

http://www.zerohedge.com/news/credit-suisse-sequel-probabili…

A week ago we presented an excerpt from Credit Suisse's most excellent piece "The Flaw" - merely the latest in one of the best overviews of the neverending Greek soap opera by William Porter. Yet every soap opera eventually ends. Although when it comes to Nielsen ratings, the denouement is usually a whimper. In the case of Greece, it will be anything but. Yet listening to the daily cacafony of din from Europe's leaders, who are likely more clueless than the average reader as to what is really going on, one may be left with the impression that there is a simple solution to the problem, and Greece may be "saved... in hours." It can't. In fact, as of today, Porter's s conclusion is: "we are left with a sense that the probability of delivering the largest default loss in history in a disorderly way on or before 20 March has increased relative to doing so in an orderly way."

....

http://www.zerohedge.com/news/credit-suisse-sequel-probabili…

http://www.zerohedge.com/news/market-slowly-figures-out-ecb-…

Market Slowly Figures Out ECB Fake Out Is Euro And Greece Negative As Greek 1 Year Bonds Hit 639%

Yesterday, when the rumor (because it has not been confirmed by the ECB, and most certainly not by the Bundesbank) that the ECB would distribute its "gains" (i.e., personally fund the difference between cost basis and par on Greek bonds - incidentally, a development which BUBA president Jens Weidmann has said would only happen over his dead body) we urged readers "to ignore the constant barrage of meaningless noise and flashing red headlines" as apparently nobody who trades the EURUSD has any clue what subordination means or has ever participated in any debt for equity transaction. Specifically, with regard to the idiotic EURUSD reaction we said: "Today [yesterday] is a great case in point of a tangential detour which does nothing to change the reality that Germany no longer wants Greece in the Eurozone (remember, oh, yesterday), and that the ECB is merely playing possum with PSI creditors who will block the deal with even greater vigor than before (anyone recall the FT story about the PSI deal being on the verge of collapse not due to the ECB but due to private creditors?) as the ECB's even bigger subordination will simply make the amount of hold outs even greater." We concluded by assuming that "algos will take the required 12-48 hours to figure out what just happened today." Well, the algos are still lost in idiot vacuum tube world, but at least the banks are starting to comprehend what the 'deal' really means and that the Nash Equilibrium is even worse than before. From Bloomberg: "A plan being considered by the European Central Bank to shield its Greek bond holdings from a restructuring may hurt the euro because it implies senior status for the ECB over other investors, UBS AG said. “There are at least two euro-negative dimensions, which will likely lead to euro weakness” as a result of the plan, Chris Walker, a foreign-exchange strategist at UBS in London, wrote in a research report today." Once again, we urge all FX traders to read our primer on subordination, and why and how it will define trading this year, as reactions such as the one yesterday confirm that the market is not only broken but also very stupid.

More:

“The risk of a voluntary restructuring morphing into a coercive one has arguably increased significantly,” Walker said. “It may appear that the ECB is receiving preferential treatment, raising questions about whether the ECB is senior to private sector bondholders, not only in the case of Greek debt, but also regarding the debt of other euro-zone nations that the ECB may be purchasing.

“A private sector bondholder that has been suddenly and unexpectedly subordinated may have a reduced incentive to continue to hold onto that debt,” he said.

UBS, the world’s third-biggest currency trader, estimates the shared currency will slide to $1.25 in three months and $1.15 in one year, according to today’s report.

And while FX, and naturally stock, markets are getting dumber by the minute, the one final bastion or rationality remains credit. Indeed, Greek 1 year bonds just dropped to a new all time low, yielding a jaw-dropping 583% and trading as high as 639%.

Market Slowly Figures Out ECB Fake Out Is Euro And Greece Negative As Greek 1 Year Bonds Hit 639%

Yesterday, when the rumor (because it has not been confirmed by the ECB, and most certainly not by the Bundesbank) that the ECB would distribute its "gains" (i.e., personally fund the difference between cost basis and par on Greek bonds - incidentally, a development which BUBA president Jens Weidmann has said would only happen over his dead body) we urged readers "to ignore the constant barrage of meaningless noise and flashing red headlines" as apparently nobody who trades the EURUSD has any clue what subordination means or has ever participated in any debt for equity transaction. Specifically, with regard to the idiotic EURUSD reaction we said: "Today [yesterday] is a great case in point of a tangential detour which does nothing to change the reality that Germany no longer wants Greece in the Eurozone (remember, oh, yesterday), and that the ECB is merely playing possum with PSI creditors who will block the deal with even greater vigor than before (anyone recall the FT story about the PSI deal being on the verge of collapse not due to the ECB but due to private creditors?) as the ECB's even bigger subordination will simply make the amount of hold outs even greater." We concluded by assuming that "algos will take the required 12-48 hours to figure out what just happened today." Well, the algos are still lost in idiot vacuum tube world, but at least the banks are starting to comprehend what the 'deal' really means and that the Nash Equilibrium is even worse than before. From Bloomberg: "A plan being considered by the European Central Bank to shield its Greek bond holdings from a restructuring may hurt the euro because it implies senior status for the ECB over other investors, UBS AG said. “There are at least two euro-negative dimensions, which will likely lead to euro weakness” as a result of the plan, Chris Walker, a foreign-exchange strategist at UBS in London, wrote in a research report today." Once again, we urge all FX traders to read our primer on subordination, and why and how it will define trading this year, as reactions such as the one yesterday confirm that the market is not only broken but also very stupid.

More:

“The risk of a voluntary restructuring morphing into a coercive one has arguably increased significantly,” Walker said. “It may appear that the ECB is receiving preferential treatment, raising questions about whether the ECB is senior to private sector bondholders, not only in the case of Greek debt, but also regarding the debt of other euro-zone nations that the ECB may be purchasing.

“A private sector bondholder that has been suddenly and unexpectedly subordinated may have a reduced incentive to continue to hold onto that debt,” he said.

UBS, the world’s third-biggest currency trader, estimates the shared currency will slide to $1.25 in three months and $1.15 in one year, according to today’s report.

And while FX, and naturally stock, markets are getting dumber by the minute, the one final bastion or rationality remains credit. Indeed, Greek 1 year bonds just dropped to a new all time low, yielding a jaw-dropping 583% and trading as high as 639%.