BL - Musterdepot (2012) Start mit 10.000 CAD - 500 Beiträge pro Seite

eröffnet am 04.01.12 21:10:13 von

neuester Beitrag 26.08.14 20:58:08 von

neuester Beitrag 26.08.14 20:58:08 von

Beiträge: 431

ID: 1.171.451

ID: 1.171.451

Aufrufe heute: 0

Gesamt: 37.444

Gesamt: 37.444

Aktive User: 0

Top-Diskussionen

| Titel | letzter Beitrag | Aufrufe |

|---|---|---|

| vor 18 Minuten | 692 | |

| vor 15 Minuten | 461 | |

| vor 17 Minuten | 425 | |

| 28.05.24, 23:11 | 422 | |

| vor 17 Minuten | 384 | |

| heute 00:38 | 295 | |

| heute 03:24 | 264 | |

| gestern 23:59 | 257 |

Meistdiskutierte Wertpapiere

| Platz | vorher | Wertpapier | Kurs | Perf. % | Anzahl | ||

|---|---|---|---|---|---|---|---|

| 1. | 1. | 18.620,73 | -0,09 | 188 | |||

| 2. | 2. | 7,4620 | +1,17 | 139 | |||

| 3. | 3. | 2.367,46 | +0,51 | 93 | |||

| 4. | 4. | 29,02 | +0,29 | 74 | |||

| 5. | 5. | 19,794 | +2,76 | 61 | |||

| 6. | 6. | 160,52 | -0,24 | 56 | |||

| 7. | 7. | 10,440 | -2,61 | 50 | |||

| 8. | 9. | 0,1865 | -0,53 | 39 |

Dieses Depot ist quasi eine alternative Ausbildungsversicherung für meinen Sohn- praktikabler Weise hier nur eine virtuelle Nachbildung (stockhouse).

Ich handele dabei ausschliesslich in Canada und gebe die jeweilige "Commission" der Einfachheit halber jeweils mit jeweils 10 CAD an. Zunaechst werden im Schwerpunkt nur Werte im Segement Rohstoffwerte, Minen und Explorer gehandelt. Nur long, kein short. Hohes Risiko mit der Erwartung eines raschen Wertzuwachses.

Der erste Trade (Teileinstieg): 2500 CDU zu 1,06 CAD.

Begruendung: Interessanter Kohleplay in Canada, riesige Eisenerzlagerstaette in Ghana bringt zusaetzliches Potential.

Portfolio Value Summary as of 14:56:17 Wed 04 Jan 2012 ($cad)

Total $Bought cad$ 2,660

Total $Sold $ 0

Total Equity Cost $ 2,660

Current Equity Value $ 2,650

Your Net Return $ -10 -0.38%

Net Cash From Trades $ -2,660

Total Cash Deposits $ 0

Total Cash Dividends $ 0

Total Cash Withdrawls $ 0

Fixed Cash Balance in Cdn$ $ 10,000

Total Cash Balance $ 7,340

Current Equity Value $ 2,650

Total Portfolio Value $ 9,990

Ich handele dabei ausschliesslich in Canada und gebe die jeweilige "Commission" der Einfachheit halber jeweils mit jeweils 10 CAD an. Zunaechst werden im Schwerpunkt nur Werte im Segement Rohstoffwerte, Minen und Explorer gehandelt. Nur long, kein short. Hohes Risiko mit der Erwartung eines raschen Wertzuwachses.

Der erste Trade (Teileinstieg): 2500 CDU zu 1,06 CAD.

Begruendung: Interessanter Kohleplay in Canada, riesige Eisenerzlagerstaette in Ghana bringt zusaetzliches Potential.

Portfolio Value Summary as of 14:56:17 Wed 04 Jan 2012 ($cad)

Total $Bought cad$ 2,660

Total $Sold $ 0

Total Equity Cost $ 2,660

Current Equity Value $ 2,650

Your Net Return $ -10 -0.38%

Net Cash From Trades $ -2,660

Total Cash Deposits $ 0

Total Cash Dividends $ 0

Total Cash Withdrawls $ 0

Fixed Cash Balance in Cdn$ $ 10,000

Total Cash Balance $ 7,340

Current Equity Value $ 2,650

Total Portfolio Value $ 9,990

2. Trade:

Canada TV 3000 0.95 $cad

Begruendung: Erwarte Schub - Produktionsaufnahme steht bevor, das Financing sollte abgearbeitet sein.

--

Portfolio Value Summary as of 15:19:39 Wed 04 Jan 2012 ($cad)

Total $Bought cad$ 5,520

Total $Sold $ 0

Total Equity Cost $ 5,520

Current Equity Value $ 5,500

Your Net Return $ -20 -0.36%

Net Cash From Trades $ -5,520

Total Cash Deposits $ 0

Total Cash Dividends $ 0

Total Cash Withdrawls $ 0

Fixed Cash Balance in Cdn$ $ 10,000

Total Cash Balance $ 4,480

Current Equity Value $ 5,500

Total Portfolio Value $ 9,980

Canada TV 3000 0.95 $cad

Begruendung: Erwarte Schub - Produktionsaufnahme steht bevor, das Financing sollte abgearbeitet sein.

--

Portfolio Value Summary as of 15:19:39 Wed 04 Jan 2012 ($cad)

Total $Bought cad$ 5,520

Total $Sold $ 0

Total Equity Cost $ 5,520

Current Equity Value $ 5,500

Your Net Return $ -20 -0.36%

Net Cash From Trades $ -5,520

Total Cash Deposits $ 0

Total Cash Dividends $ 0

Total Cash Withdrawls $ 0

Fixed Cash Balance in Cdn$ $ 10,000

Total Cash Balance $ 4,480

Current Equity Value $ 5,500

Total Portfolio Value $ 9,980

Antwort auf Beitrag Nr.: 42.551.537 von boersenbrieflemming am 04.01.12 21:20:43Eine WKN wäre schon das mindeste...

Antwort auf Beitrag Nr.: 42.552.588 von EPB am 05.01.12 09:32:31

Cardero Resource Aktie ISIN: CA14140U1057 | WKN: 919945 | Symbol: CR5

Cardero Resource Aktie ISIN: CA14140U1057 | WKN: 919945 | Symbol: CR5

Ein neuer Kauf:

USA (TSX): 6,500 zu 0.43 CAD

http://www.us-silver.com/

@BRBa

Der Handel an der FSE ist mir bei vielen Werten auf meiner WL einfach zu duenn.

USA (TSX): 6,500 zu 0.43 CAD

http://www.us-silver.com/

@BRBa

Der Handel an der FSE ist mir bei vielen Werten auf meiner WL einfach zu duenn.

Trading Spotlight

Nachtrag zum Kauf vom 4. Januar (Trevali, TV)

Trevali Commences Initial Production at Halfmile Mine in New Brunswick ...

http://finance.yahoo.com/news/Trevali-Commences-Initial-iw-2…

Trevali Commences Initial Production at Halfmile Mine in New Brunswick ...

http://finance.yahoo.com/news/Trevali-Commences-Initial-iw-2…

Nachtrag zum Depotwert CDU:

Cardero publishes finalised PEA for BC coal project

http://www.miningweekly.com/article/cardero-publishes-finali…

Cardero publishes finalised PEA for BC coal project

http://www.miningweekly.com/article/cardero-publishes-finali…

Ein kleiner Trade: 6000 ABS (Abzu Gold) zu 0,245 CAD

2012-01-11 00:00 Buy Canada ABS 6000 0.245 $cad 10.00 $cad 1,480 Edit Delete 1,480 6,000

Stand:

Portfolio Value Summary as of 14:51:48 Wed 11 Jan 2012 ($cad)

Total $Bought cad$ 9,805

Total $Sold $ 0

Total Equity Cost $ 9,805

Current Equity Value $ 10,248

Your Net Return $ 443 4.51%

Net Cash From Trades $ -9,805

Total Cash Deposits $ 0

Total Cash Dividends $ 0

Total Cash Withdrawls $ 0

Fixed Cash Balance in Cdn$ $ 10,000

Total Cash Balance $ 195

Current Equity Value $ 10,248

Total Portfolio Value $ 10,443

2012-01-11 00:00 Buy Canada ABS 6000 0.245 $cad 10.00 $cad 1,480 Edit Delete 1,480 6,000

Stand:

Portfolio Value Summary as of 14:51:48 Wed 11 Jan 2012 ($cad)

Total $Bought cad$ 9,805

Total $Sold $ 0

Total Equity Cost $ 9,805

Current Equity Value $ 10,248

Your Net Return $ 443 4.51%

Net Cash From Trades $ -9,805

Total Cash Deposits $ 0

Total Cash Dividends $ 0

Total Cash Withdrawls $ 0

Fixed Cash Balance in Cdn$ $ 10,000

Total Cash Balance $ 195

Current Equity Value $ 10,248

Total Portfolio Value $ 10,443

@BL - Was hältst Du denn von WML (WKN: A0CADP) und IDI (WKN: A0MQ4E)?

Kommen doch auch beide "aus dem Hause" Cardero: http://www.cardero-group.com/

...und sind vom Kurs her auch jeweils völlig ausgebombt und könnten somit ebenso für einen flotten Rebound gut sein:

Kommen doch auch beide "aus dem Hause" Cardero: http://www.cardero-group.com/

...und sind vom Kurs her auch jeweils völlig ausgebombt und könnten somit ebenso für einen flotten Rebound gut sein:

Antwort auf Beitrag Nr.: 42.585.326 von 666-2004 am 12.01.12 16:00:15Ich habe beide Shares auf meiner Watchlist - beide verfuegen ueber Vermehrfachungspotential. Das tun andere Werte aber auch.

Ich muss mich bei einem 10.000 CAD Depot sehr stark beschraenken und anders als gewohnt handeln, da zudem noch ein Zeitfaktor hinzukommt: Ich bin ab Montag fuer ein paar Wochen in Afrika und dann auch in Gebieten, bei denen es keine (oder nur eingeschraenkte) Internetkonnektivitaet gibt.

Bei Werten wie TV, CDU oder USA muss man nicht zwingend auf jede kleine Ueberraschung reagieren und bei ABS rechne ich mit weiterer Exploration, die BE fand ich bis jetzt anstaendig - sind noch sehr am Anfang. Hier wird dann die Aussagekraft weiter zunehmen, dafuer spricht schon das Gebiet.

Wir scheinen uns zu kennen, mit wem habe ich das Vergnuegen?

BL

Ich muss mich bei einem 10.000 CAD Depot sehr stark beschraenken und anders als gewohnt handeln, da zudem noch ein Zeitfaktor hinzukommt: Ich bin ab Montag fuer ein paar Wochen in Afrika und dann auch in Gebieten, bei denen es keine (oder nur eingeschraenkte) Internetkonnektivitaet gibt.

Bei Werten wie TV, CDU oder USA muss man nicht zwingend auf jede kleine Ueberraschung reagieren und bei ABS rechne ich mit weiterer Exploration, die BE fand ich bis jetzt anstaendig - sind noch sehr am Anfang. Hier wird dann die Aussagekraft weiter zunehmen, dafuer spricht schon das Gebiet.

Wir scheinen uns zu kennen, mit wem habe ich das Vergnuegen?

BL

Ein kleiner Nachtrag zu Trevali:

M Partners maintains a buy reccomendation on Trevali with a 12 month target of $3.00

GMP vor Kurzem: $2,20

Jeweils 12-Monatsziele - die Haeuser reizen sich hoch.

M Partners maintains a buy reccomendation on Trevali with a 12 month target of $3.00

GMP vor Kurzem: $2,20

Jeweils 12-Monatsziele - die Haeuser reizen sich hoch.

http://www.marketwatch.com/story/trevali-and-first-nations-l…" target="_blank" rel="nofollow ugc noopener">News zu den Depotwerten TV und CDU:

http://www.marketwatch.com/story/trevali-and-first-nations-l…

http://www.marketwatch.com/story/trevali-and-first-nations-l…

sorry:

http://www.marketwatch.com/story/trevali-and-first-nations-l…" target="_blank" rel="nofollow ugc noopener">

http://www.marketwatch.com/story/trevali-and-first-nations-l…

http://www.marketwatch.com/story/trevali-and-first-nations-l…" target="_blank" rel="nofollow ugc noopener">

http://www.marketwatch.com/story/trevali-and-first-nations-l…

Portfolio Value Summary as of 15:48:02 Wed 18 Jan 2012 ($cad)

Total $Bought cad$ 9,805

Total $Sold $ 0

Total Equity Cost $ 9,805

Current Equity Value $ 10,613

Your Net Return $ 808 8.24%

Net Cash From Trades $ -9,805

Total Cash Deposits $ 0

Total Cash Dividends $ 0

Total Cash Withdrawls $ 0

Fixed Cash Balance in Cdn$ $ 10,000

Total Cash Balance $ 195

Current Equity Value $ 10,613

Total Portfolio Value $ 10,808

Total $Bought cad$ 9,805

Total $Sold $ 0

Total Equity Cost $ 9,805

Current Equity Value $ 10,613

Your Net Return $ 808 8.24%

Net Cash From Trades $ -9,805

Total Cash Deposits $ 0

Total Cash Dividends $ 0

Total Cash Withdrawls $ 0

Fixed Cash Balance in Cdn$ $ 10,000

Total Cash Balance $ 195

Current Equity Value $ 10,613

Total Portfolio Value $ 10,808

Weil es mich für meinen Sohn freut:

Portfolio Value Summary as of 12:20:31 Thu 19 Jan 2012 ($cad)

Total $Bought cad$ 9,805

Total $Sold $ 0

Total Equity Cost $ 9,805

Current Equity Value $ 10,855

Your Net Return $ 1,050 10.71%

Net Cash From Trades $ -9,805

Total Cash Deposits $ 0

Total Cash Dividends $ 0

Total Cash Withdrawls $ 0

Fixed Cash Balance in Cdn$ $ 10,000

Total Cash Balance $ 195

Current Equity Value $ 10,855

Total Portfolio Value $ 11,050

--

Portfolio Value Summary as of 12:20:31 Thu 19 Jan 2012 ($cad)

Total $Bought cad$ 9,805

Total $Sold $ 0

Total Equity Cost $ 9,805

Current Equity Value $ 10,855

Your Net Return $ 1,050 10.71%

Net Cash From Trades $ -9,805

Total Cash Deposits $ 0

Total Cash Dividends $ 0

Total Cash Withdrawls $ 0

Fixed Cash Balance in Cdn$ $ 10,000

Total Cash Balance $ 195

Current Equity Value $ 10,855

Total Portfolio Value $ 11,050

--

Portfolio Value Summary as of 10:20:19 Thu 26 Jan 2012 ($cad)

Total $Bought cad$ 9,805

Total $Sold $ 0

Total Equity Cost $ 9,805

Current Equity Value $ 11,978

Your Net Return $ 2,173 22.16%

Total $Bought cad$ 9,805

Total $Sold $ 0

Total Equity Cost $ 9,805

Current Equity Value $ 11,978

Your Net Return $ 2,173 22.16%

Portfolio Value Summary as of 12:37:28 Thu 02 Feb 2012 ($cad)

Total $Bought cad$ 9,805

Total $Sold $ 0

Total Equity Cost $ 9,805

Current Equity Value $ 12,424

Your Net Return $ 2,619 26.71%

USA:

US Silver Corp (1)

Symbol C : USA

Shares Issued 309,182,717

Close 2012-01-25 C$ 0.465

Recent Sedar Documents

View Original Document

U.S. Silver to consolidate shares 1:5 Jan. 30

Total $Bought cad$ 9,805

Total $Sold $ 0

Total Equity Cost $ 9,805

Current Equity Value $ 12,424

Your Net Return $ 2,619 26.71%

USA:

US Silver Corp (1)

Symbol C : USA

Shares Issued 309,182,717

Close 2012-01-25 C$ 0.465

Recent Sedar Documents

View Original Document

U.S. Silver to consolidate shares 1:5 Jan. 30

Alles schoen gruen.

5 ABS Canada 6,000 0 1,480 0 1,480 6,000 0.25 0.325 1,950 470 31.76 TR

5 CDU Canada 2,500 0 2,660 0 2,660 2,500 1.06 1.47 3,675 1,015 38.16 TR

5 TV Canada 3,000 0 2,860 0 2,860 3,000 0.95 1.30 3,900 1,040 36.36 TR

5 USA Canada 1,300 0 2,805 0 2,805 1,300 2.16 2.40 3,120 315 11.23 TR

5 ABS Canada 6,000 0 1,480 0 1,480 6,000 0.25 0.325 1,950 470 31.76 TR

5 CDU Canada 2,500 0 2,660 0 2,660 2,500 1.06 1.47 3,675 1,015 38.16 TR

5 TV Canada 3,000 0 2,860 0 2,860 3,000 0.95 1.30 3,900 1,040 36.36 TR

5 USA Canada 1,300 0 2,805 0 2,805 1,300 2.16 2.40 3,120 315 11.23 TR

2012-02-09 00:00 Sell Canada TV 1500 1.50 $cad 10.00 $cad -2,240

Teilverkauf Trevali (derzeit + 56,99%)

Trevali bleibt in meinen uebrigen Depots unangetastet, hier brauche ich aber fuer die naechste Woche etwas Cash - zudem muss ich bei einem 10.000 CAD Depot anders handeln.

Teilverkauf Trevali (derzeit + 56,99%)

Trevali bleibt in meinen uebrigen Depots unangetastet, hier brauche ich aber fuer die naechste Woche etwas Cash - zudem muss ich bei einem 10.000 CAD Depot anders handeln.

Portfolio Value Summary as of 11:10:45 Thu 09 Feb 2012 ($cad)

Total $Bought cad$ 9,805

Total $Sold $ 2,240

Total Equity Cost $ 7,565

Current Equity Value $ 10,320

Your Net Return $ 2,755 28.10%

Net Cash From Trades $ -7,565

Total Cash Deposits $ 0

Total Cash Dividends $ 0

Total Cash Withdrawls $ 0

Fixed Cash Balance in Cdn$ $ 10,000

Total Cash Balance $ 2,435

Current Equity Value $ 10,320

Total Portfolio Value $ 12,755

Total $Bought cad$ 9,805

Total $Sold $ 2,240

Total Equity Cost $ 7,565

Current Equity Value $ 10,320

Your Net Return $ 2,755 28.10%

Net Cash From Trades $ -7,565

Total Cash Deposits $ 0

Total Cash Dividends $ 0

Total Cash Withdrawls $ 0

Fixed Cash Balance in Cdn$ $ 10,000

Total Cash Balance $ 2,435

Current Equity Value $ 10,320

Total Portfolio Value $ 12,755

Ein neuer Kauf, nachdem mir ein anderer Share davon gelaufen ist:

2012-02-17 00:00 Buy Canada SLX 5200 0.425 $cad 10.00 $cad 2,220 Edit Delete 2,220 5,200

--

5200 - SILVERMEX RESOURCES INC. - http://www.silvermexresources.com

--

Silvermex hat nachvollziehbar kraeftig abgegeben und sollte bei guenstigen Bedingujngen nun wieder etwas performen.

2012-02-17 00:00 Buy Canada SLX 5200 0.425 $cad 10.00 $cad 2,220 Edit Delete 2,220 5,200

--

5200 - SILVERMEX RESOURCES INC. - http://www.silvermexresources.com

--

Silvermex hat nachvollziehbar kraeftig abgegeben und sollte bei guenstigen Bedingujngen nun wieder etwas performen.

Portfolio Value Summary as of 12:12:22 Thu 23 Feb 2012 ($cad)

Total $Bought cad$ 12,025

Total $Sold $ 2,240

Total Equity Cost $ 9,785

Current Equity Value $ 13,046

Your Net Return $ 3,261 27.12%

Net Cash From Trades $ -9,785

Total Cash Deposits $ 0

Total Cash Dividends $ 0

Total Cash Withdrawls $ 0

Fixed Cash Balance in Cdn$ $ 10,000

Total Cash Balance $ 215

Current Equity Value $ 13,046

Total Portfolio Value $ 13,261

Total $Bought cad$ 12,025

Total $Sold $ 2,240

Total Equity Cost $ 9,785

Current Equity Value $ 13,046

Your Net Return $ 3,261 27.12%

Net Cash From Trades $ -9,785

Total Cash Deposits $ 0

Total Cash Dividends $ 0

Total Cash Withdrawls $ 0

Fixed Cash Balance in Cdn$ $ 10,000

Total Cash Balance $ 215

Current Equity Value $ 13,046

Total Portfolio Value $ 13,261

Verkauf SLX

2012-02-23 00:00 Sell Canada SLX 5200 0.48 $cad 0.00 $cad -2,496 Edit Delete -276 0

Den kleineren Gewinn nehme ich gerne mit, ich brauche etwas cash.

2012-02-23 00:00 Sell Canada SLX 5200 0.48 $cad 0.00 $cad -2,496 Edit Delete -276 0

Den kleineren Gewinn nehme ich gerne mit, ich brauche etwas cash.

Kauf CMK (Cline Mining)

2012-02-28 00:00 Buy Canada CMK 1300 1.98 $cad 20.00 $cad 2,594 Edit Delete 2,594 1,300

(20 CAD Commission, da beim Verkauf von SLX vergessen)

2012-02-28 00:00 Buy Canada CMK 1300 1.98 $cad 20.00 $cad 2,594 Edit Delete 2,594 1,300

(20 CAD Commission, da beim Verkauf von SLX vergessen)

Falls sich zwischenzeitlich an der Portfoliozusammensetzung nichts geändert hat, dann hat Dein Depot seit Jahresbeginn um rund 15% verloren.

Ganz schön heftig sehen laut deiner Einträge aus:

Abzu -27%

Cardero -12%

Cline -34%

Ein Vergleichswert, zu dem Du gelegentlich negative Stimmen postest, ist seit Jahresbeginn hingegen deutlich im Plus..

Denk mal drüber nach.

Ganz schön heftig sehen laut deiner Einträge aus:

Abzu -27%

Cardero -12%

Cline -34%

Ein Vergleichswert, zu dem Du gelegentlich negative Stimmen postest, ist seit Jahresbeginn hingegen deutlich im Plus..

Denk mal drüber nach.

Mr. Ken Bates reports

MARKET TRENDS

Cline Mining Corp. wishes to advise that there are no developments in the business or affairs of the company which have not been announced. Management attributes recent price movements in its shares as being the result of current market pricing for coal on world markets. The demand for and price of coal have been adversely affected by global economic conditions.

---

Zu Cline: Mitteilungen wie diese sind für den Markt natürlich Gift - mit derzeit um einen 1 CAD halte ich die Bewertung für einen Witz.

Portfolio:

Total Portfolio Value $ 9,800

5 ABS Canada 6,000 0 1,480 0 1,480 6,000 0.25 0.26 1,560 80 5.41 TR

5 CDU Canada 2,500 0 2,660 0 2,660 2,500 1.06 0.97 2,425 -235 -8.83 TR

5 CMK Canada 1,300 0 2,594 0 2,594 1,300 2.00 1.05 1,365 -1,229 -47.38 TR

5 TV Canada 3,000 1,500 2,860 2,240 620 1,500 0.41 1.32 1,980 1,360 47.55 TR

5 USA Canada 1,300 0 2,805 0 2,805 1,300 2.16 1.81 2,353 -452 -16.11 TR

MARKET TRENDS

Cline Mining Corp. wishes to advise that there are no developments in the business or affairs of the company which have not been announced. Management attributes recent price movements in its shares as being the result of current market pricing for coal on world markets. The demand for and price of coal have been adversely affected by global economic conditions.

---

Zu Cline: Mitteilungen wie diese sind für den Markt natürlich Gift - mit derzeit um einen 1 CAD halte ich die Bewertung für einen Witz.

Portfolio:

Total Portfolio Value $ 9,800

5 ABS Canada 6,000 0 1,480 0 1,480 6,000 0.25 0.26 1,560 80 5.41 TR

5 CDU Canada 2,500 0 2,660 0 2,660 2,500 1.06 0.97 2,425 -235 -8.83 TR

5 CMK Canada 1,300 0 2,594 0 2,594 1,300 2.00 1.05 1,365 -1,229 -47.38 TR

5 TV Canada 3,000 1,500 2,860 2,240 620 1,500 0.41 1.32 1,980 1,360 47.55 TR

5 USA Canada 1,300 0 2,805 0 2,805 1,300 2.16 1.81 2,353 -452 -16.11 TR

Ich verkaufe:

2012-04-16 00:00 Sell Canada USA 1300 1.80 $cad 10.00 $cad -2,330 Edit Delete

USA hat mich vom Kursverlauf her ziemlich enttäuscht.

2012-04-16 00:00 Sell Canada USA 1300 1.80 $cad 10.00 $cad -2,330 Edit Delete

USA hat mich vom Kursverlauf her ziemlich enttäuscht.

Kauf: 2012-04-16 00:00 Buy Canada CDU 2000 0.95 $cad 10.00 $cad 1,910 Edit Delete 4,570 4,50

--

Es könnten zwar noch billiger werden - ich erwarte aber noch News vor Ablauf der Earning Season.

--

Es könnten zwar noch billiger werden - ich erwarte aber noch News vor Ablauf der Earning Season.

Zitat von boersenbrieflemming (am 16.04.12 17:11:26): (..)

Portfolio:

Total Portfolio Value $ 9,800

5 ABS Canada 6,000 0 1,480 0 1,480 6,000 0.25 0.26 1,560 80 5.41 TR

5 CDU Canada 2,500 0 2,660 0 2,660 2,500 1.06 0.97 2,425 -235 -8.83 TR

5 CMK Canada 1,300 0 2,594 0 2,594 1,300 2.00 1.05 1,365 -1,229 -47.38 TR

5 TV Canada 3,000 1,500 2,860 2,240 620 1,500 0.41 1.32 1,980 1,360 47.55 TR

5 USA Canada 1,300 0 2,805 0 2,805 1,300 2.16 1.81 2,353 -452 -16.11 TR

Da haben sich,wenn ich das richtig sehe, wohl versehentlich 1.500 Trevalis dazugemogelt, die schon längst verkauft wurden.

Der Total Portfolio Value sieht also bei richtiger Rechnung nicht mehr ganz so toll aus wie in obigem Posting :

Hier dokumentiert wurden für TV ein Kauf von 3.000 Stück am 4.1. und ein Verkauf von 1.500 Stück am 9.2.

Mit nunmehr

- 6.000 Stück ABS

- 1.500 TV

- 1.300 CMK

- 4.500 CDU

hat das Depot derzeit einen Kurswert von rund 6.656,- CAD und einen Kassenstand 537,- CAD

Gesamtwert 7.193,-CAD

Bei Anfänglich 10.000 CAD bedeutet dies einen Verlust von satten 28,07% seit Jahresbeginn.

Bei solch einem Fiasko im eigenen Depot steht es wahrlich nicht gut zu Gesicht, besser laufende Aktien hier im Board mit immer wieder wiederholten SELL-CONFIRMED-Meldungen provokativ schlechtzureden.

Denkmal drüber nach.

Antwort auf Beitrag Nr.: 43.057.941 von DCShoes am 19.04.12 01:31:13Du kannst da leider nicht richtig rechnen - aktuell ist das Depot aber tatsächlich ins Minus gerutscht:

Total $Bought cad$ 16,529

Total $Sold $ 7,066

Total Equity Cost $ 9,463

Current Equity Value $ 8,652

Your Net Return $ -811 -4.91%

Net Cash From Trades $ -9,463

Total Cash Deposits $ 0

Total Cash Dividends $ 0

Total Cash Withdrawls $ 0

Fixed Cash Balance in Cdn$ $ 10,000

Total Cash Balance $ 537

Current Equity Value $ 8,652

Total Portfolio Value $ 9,189

--

Die Performance ist deutlich unter meinen Erwartungen, jedoch angesichts der Marktlage derzeit eben so hinzunehmen. Bei der CMK konnte ich aus technischen Gründen ein paar Tage nicht reagiere , was bei der Aktie im Moment allerdings weniger problematisch ist.

ABS: 6000 Stck. 1,350 CAD

CDU:4500 Stck. 4,140 CAD

CMK:1300 Stck. 1,287 CAD

TV: 1500 Stck 1,875 CAD

Cash: 537 CAD

Ich wäre Dir sehr dankbar, wenn ich hier keine weiteren Kommentare von dir lesen würde. Du gehörst zu den WO-Nutzern, die unter unterschiedlichen IDs agierten und in der Vergangenheit bei WO getrickst und getäuscht haben, um Aktien zu bewerben. Ich erinnere dich da gerne an die Masche, in der du dich als englischsprachiger Investor in anderen Threads ausgegeben hast.

Total $Bought cad$ 16,529

Total $Sold $ 7,066

Total Equity Cost $ 9,463

Current Equity Value $ 8,652

Your Net Return $ -811 -4.91%

Net Cash From Trades $ -9,463

Total Cash Deposits $ 0

Total Cash Dividends $ 0

Total Cash Withdrawls $ 0

Fixed Cash Balance in Cdn$ $ 10,000

Total Cash Balance $ 537

Current Equity Value $ 8,652

Total Portfolio Value $ 9,189

--

Die Performance ist deutlich unter meinen Erwartungen, jedoch angesichts der Marktlage derzeit eben so hinzunehmen. Bei der CMK konnte ich aus technischen Gründen ein paar Tage nicht reagiere , was bei der Aktie im Moment allerdings weniger problematisch ist.

ABS: 6000 Stck. 1,350 CAD

CDU:4500 Stck. 4,140 CAD

CMK:1300 Stck. 1,287 CAD

TV: 1500 Stck 1,875 CAD

Cash: 537 CAD

Ich wäre Dir sehr dankbar, wenn ich hier keine weiteren Kommentare von dir lesen würde. Du gehörst zu den WO-Nutzern, die unter unterschiedlichen IDs agierten und in der Vergangenheit bei WO getrickst und getäuscht haben, um Aktien zu bewerben. Ich erinnere dich da gerne an die Masche, in der du dich als englischsprachiger Investor in anderen Threads ausgegeben hast.

Antwort auf Beitrag Nr.: 43.058.026 von boersenbrieflemming am 19.04.12 06:33:19Da Du in den Threads meiner gehaltenen Werte wenig Zurückhaltung übst, auf vermeintliche Fehler aufmerksam zu machen, nehme ich auch mir heraus, Dich bei Deinen Werten auf vermeintliche Fehler aufmerksam zu machen.

Ist doch wichtig der Austausch in einem Forum.

Ist doch wichtig der Austausch in einem Forum.

Das Problem ist doch, dass hier kein Fehler vorlag. Du hättest nur die Grundrechenarten nutzen müssen. Im Zweifel hilft auch einTaschenrechner.

Antwort auf Beitrag Nr.: 43.058.879 von boersenbrieflemming am 19.04.12 10:00:23Schon wieder -1,14% am Wochenschluss?

Mit Cardero und Trevali hast Du Dir keine schönen Werte ins Depot gelegt. Und Cline auch schon bei -50%... Einzig Trevali hält sich leidlich. Das war zumindest kurzfristig ein guter Griff.

Mit Cardero und Trevali hast Du Dir keine schönen Werte ins Depot gelegt. Und Cline auch schon bei -50%... Einzig Trevali hält sich leidlich. Das war zumindest kurzfristig ein guter Griff.

Antwort auf Beitrag Nr.: 43.088.897 von boersenbrieflemming am 25.04.12 22:18:34geht ja schon über hoch im Depot. Hatte bei Cardero keine solche Reaktion mehr erwartet. Cline bin ich gespannt, Du scheinst da ja völlig ruhig zu sein und die 50% Miesen auszusitzen.  Bin gespannt.

Bin gespannt.

Bin gespannt.

Bin gespannt.

Antwort auf Beitrag Nr.: 43.089.131 von DCShoes am 25.04.12 23:12:45Das hat ja noch ganz schön gedreht heute für Deine Werte.

Bei glänzendem Börsenwetter ging es doch noch 2,91% abwärts und somit auf insgesamt über -20% seit Kauf für die im Depot befindlichen Werte.

In vier Monaten ein peinlicher Verlust für solch stets hochgelobte Aktien.

Bei glänzendem Börsenwetter ging es doch noch 2,91% abwärts und somit auf insgesamt über -20% seit Kauf für die im Depot befindlichen Werte.

In vier Monaten ein peinlicher Verlust für solch stets hochgelobte Aktien.

Uiuiui, was für ein Massaker hier

Bist du sicher dass dein Sohn mit dieser Art von Anlage einverstanden ist?

Benutz doch wenigstens SL's, 50% und mehr Verlust "auszusitzen" ist sicherlich nicht state of the art Kann nur hoffen dass hier kein User das Depot nachgebildet hat ...

Kann nur hoffen dass hier kein User das Depot nachgebildet hat ...

Bist du sicher dass dein Sohn mit dieser Art von Anlage einverstanden ist?

Benutz doch wenigstens SL's, 50% und mehr Verlust "auszusitzen" ist sicherlich nicht state of the art

Kann nur hoffen dass hier kein User das Depot nachgebildet hat ...

Kann nur hoffen dass hier kein User das Depot nachgebildet hat ...

Antwort auf Beitrag Nr.: 43.094.692 von uall am 26.04.12 23:15:42Bist du sicher dass dein Sohn mit dieser Art von Anlage einverstanden ist?

Der denkt über so etwas noch nicht nach.

Der denkt über so etwas noch nicht nach.

Antwort auf Beitrag Nr.: 43.094.621 von DCShoes am 26.04.12 22:56:40insgesamt über -20%

Stimmt nicht - bitte nachrechnen. Danke.

Portfolio Value Summary as of 11:33:17 Fri 27 Apr 2012 ($cad)

Total $Bought cad$ 16,529

Total $Sold $ 7,066

Total Equity Cost $ 9,463

Current Equity Value $ 8,200

Your Net Return $ -1,263 -7.64%

Net Cash From Trades $ -9,463

Total Cash Deposits $ 0

Total Cash Dividends $ 0

Total Cash Withdrawls $ 0

Fixed Cash Balance in Cdn$ $ 10,000

Total Cash Balance $ 537

Current Equity Value $ 8,200

Total Portfolio Value $ 8,737

--

Es ist zwar ein aergerlicher Verlust, aber noch kein Beinbruch. Nicht in diesem Segment.

P.S. CMK erholt sich derzeit richtig gut.

Stimmt nicht - bitte nachrechnen. Danke.

Portfolio Value Summary as of 11:33:17 Fri 27 Apr 2012 ($cad)

Total $Bought cad$ 16,529

Total $Sold $ 7,066

Total Equity Cost $ 9,463

Current Equity Value $ 8,200

Your Net Return $ -1,263 -7.64%

Net Cash From Trades $ -9,463

Total Cash Deposits $ 0

Total Cash Dividends $ 0

Total Cash Withdrawls $ 0

Fixed Cash Balance in Cdn$ $ 10,000

Total Cash Balance $ 537

Current Equity Value $ 8,200

Total Portfolio Value $ 8,737

--

Es ist zwar ein aergerlicher Verlust, aber noch kein Beinbruch. Nicht in diesem Segment.

P.S. CMK erholt sich derzeit richtig gut.

Gute Handelstage bringen manchmal einen kleinen Schub:

Portfolio Value Summary as of 19:21:00 Fri 27 Apr 2012 ($cad)

Total $Bought cad$ 16,529

Total $Sold $ 7,066

Total Equity Cost $ 9,463

Current Equity Value $ 8,745

Your Net Return $ -718 -4.34%

Net Cash From Trades $ -9,463

Total Cash Deposits $ 0

Total Cash Dividends $ 0

Total Cash Withdrawls $ 0

Fixed Cash Balance in Cdn$ $ 10,000

Total Cash Balance $ 537

Current Equity Value $ 8,745

Total Portfolio Value $ 9,282

Portfolio Value Summary as of 19:21:00 Fri 27 Apr 2012 ($cad)

Total $Bought cad$ 16,529

Total $Sold $ 7,066

Total Equity Cost $ 9,463

Current Equity Value $ 8,745

Your Net Return $ -718 -4.34%

Net Cash From Trades $ -9,463

Total Cash Deposits $ 0

Total Cash Dividends $ 0

Total Cash Withdrawls $ 0

Fixed Cash Balance in Cdn$ $ 10,000

Total Cash Balance $ 537

Current Equity Value $ 8,745

Total Portfolio Value $ 9,282

Antwort auf Beitrag Nr.: 43.057.941 von DCShoes am 19.04.12 01:31:13Das ist völlig unmögliches Vorgehen. Einfach einen Verkauf zu posten, Geld einzubuchen und im Depot dann nicht nachzuvollziehen. Sauber sag ich.

Antwort auf Beitrag Nr.: 43.103.463 von valueinvestor am 30.04.12 10:51:38Unsinn. Wo soll das passiert sein?

Zitat von boersenbrieflemming: Unsinn. Wo soll das passiert sein?

boersenbrieflemming

schrieb am 04.01.12 21:20:43

Beitrag Nr.2

(42.551.537)

2. Trade:

Canada TV 3000 0.95 $cad

-----------------------------------------------------------------------

boersenbrieflemming

schrieb am 09.02.12 17:12:24

Beitrag Nr.19

(42.726.963)

Antwort

Zitat

2012-02-09 00:00 Sell Canada TV 1500 1.50 $cad 10.00 $cad -2,240

------------------------------------------------------------------------

boersenbrieflemming

schrieb am 16.04.12 17:11:26

Beitrag Nr.26

(43.044.925)

Portfolio:

5 TV Canada 3,000 1,500 2,860 2,240 620 1,500 0.41 1.32 1,980 1,360 47.55 TR

--------------------------------------------------------------------------

nix für ungut

Antwort auf Beitrag Nr.: 43.106.763 von valueinvestor am 01.05.12 10:08:57

5 TV Canada 3,000 1,500 2,860 2,240 620 1,500 0.41 1.32 1,980 1,360 47.55 TR

Das ist doch richtig - es sind 1500 Shares im Depot - 3000 wurden gekauft (grün) und 1500 verkauft (rot), verbleiben 1500 im Bestand (gefettet). Das sind einfache Grundrechenarten (Plus und Minus).

5 TV Canada 3,000 1,500 2,860 2,240 620 1,500 0.41 1.32 1,980 1,360 47.55 TR

Das ist doch richtig - es sind 1500 Shares im Depot - 3000 wurden gekauft (grün) und 1500 verkauft (rot), verbleiben 1500 im Bestand (gefettet). Das sind einfache Grundrechenarten (Plus und Minus).

ich halte es für sinnfrei, unbeschriftete Zahlenkolonnen zu posten und diese dann nach Gutdünken umzuinterpretieren.

Antwort auf Beitrag Nr.: 43.107.352 von valueinvestor am 01.05.12 14:28:34Man könnte dann auch die Lernerfolge auf das Multiplizieren ("Malnehmen") oder Dividieren ("Teilen") ausweiten.

Ich habe einmal Deine aktuelleren Tipps ( Quelle: 41.926.653) zusammengesucht.

CPN -43.40%

KAM -48.25%

MDW -32.87%

SA: -42.47% (Seabridge Gold/US)

Mach doch auch ein 10.000 CAD-Depot auf - ich lasse Dir gerne die paar Prozente Vorsprung.

Ich habe einmal Deine aktuelleren Tipps ( Quelle: 41.926.653) zusammengesucht.

CPN -43.40%

KAM -48.25%

MDW -32.87%

SA: -42.47% (Seabridge Gold/US)

Mach doch auch ein 10.000 CAD-Depot auf - ich lasse Dir gerne die paar Prozente Vorsprung.

Den Thread kann man eigentlich schliessen, sinnlos...

Total $Bought cad$ 16,529

Total $Sold $ 7,066

Total Equity Cost $ 9,463

Current Equity Value $ 8,867

Your Net Return $ -596 -3.61%

Net Cash From Trades $ -9,463

Total Cash Deposits $ 0

Total Cash Dividends $ 0

Total Cash Withdrawls $ 0

Fixed Cash Balance in Cdn$ $ 10,000

Total Cash Balance $ 537

Current Equity Value $ 8,867

Total Portfolio Value $ 9,404

Total $Sold $ 7,066

Total Equity Cost $ 9,463

Current Equity Value $ 8,867

Your Net Return $ -596 -3.61%

Net Cash From Trades $ -9,463

Total Cash Deposits $ 0

Total Cash Dividends $ 0

Total Cash Withdrawls $ 0

Fixed Cash Balance in Cdn$ $ 10,000

Total Cash Balance $ 537

Current Equity Value $ 8,867

Total Portfolio Value $ 9,404

Zu den Depotwerten (alles beachtenswerte News):

CDU:

Cardero Announces Appointment of Angus Christie to Chief Operating Officer Position

http://www.marketwatch.com/story/cardero-announces-appointme…

Das sind genau die Art von News, die der Markt jetzt bracht damit es auch mit dem Kurs aufwärts geht.

TV:

Trevali Mining Corporation (TSX:TV)

RATING Outperform 2

Closing Price C$1.27

___________________________________

Event: During market hours on May 1, 2012 Trevali provided an update on mining at its Halfmile polymetallic mine in New Brunswick.

Details:

* Halfmile Upper Zone wider than expected - The reconciliation of the actual mining so far versus the mine plan indicates that the ore-body in the Upper Zone of the Halfmile mine is approximately 25% wider than modeled (as shown in Exhibit 1). While positive, the company does not expect this to materially change its production schedule, given that the Upper Zone represents less than 10% of the Halfmile deposit.

* Mined grades on target - So far the company has mined 37,000 tonnes of ore grading 6.39% Zn, 1.9% Pb, 0.65% Cu, 40.57 grams/tonne Ag, and 0.4 grams/tonne Au. This is essentially in-line with the mine plan for the zinc and lead grades, however, it is better-than the resource model on copper, silver, and gold.

* Inaugural ore processing - Trevali also confirmed that 30,000 tonnes of ore from Halfmile has been processed through Xstrata's nearby Brunswick-12 concentrator. This represents the first batch of Trevali's ore to be processed.

Analysis: Should the Upper Zone continue to be 25% wider than modeled, we estimate that this could contribute an additional 5 months of mining (the Halfmile mine plan currently has a mine life of 20 years). The greater width of the mineralization may also enable more efficient mining conditions due to the ability to mine larger stopes. We anticipate that Trevali will generate its first revenue in late 2Q12 from the inaugural batch of 30,000 tonnes of ore that has been processed.

Adam Low, CFA

Raymond James Ltd.

ABS:

CEO Appointment and Board Changes

VANCOUVER, BRITISH COLUMBIA, May 01, 2012 (MARKETWIRE via COMTEX) -- Abzu Gold Ltd. CA:ABS 0.00% (otcqx:ABZUF) ("Abzu") is pleased to announce that Mr. Tim McCutcheon has been appointed as CEO and Director of the Company, effective immediately.

http://www.marketwatch.com/story/ceo-appointment-and-board-c…

CMK:

Cline Mining issues US$25M in secured bonds to expand New Elk mine; stock soars

http://www.canadianbusiness.com/article/82069--cline-mining-…

--

Ich wäre sehr froh, wenn sich der User valueinvestor/DCShoes einen anderen Sandkasten suchen würde.

CDU:

Cardero Announces Appointment of Angus Christie to Chief Operating Officer Position

http://www.marketwatch.com/story/cardero-announces-appointme…

Das sind genau die Art von News, die der Markt jetzt bracht damit es auch mit dem Kurs aufwärts geht.

TV:

Trevali Mining Corporation (TSX:TV)

RATING Outperform 2

Closing Price C$1.27

___________________________________

Event: During market hours on May 1, 2012 Trevali provided an update on mining at its Halfmile polymetallic mine in New Brunswick.

Details:

* Halfmile Upper Zone wider than expected - The reconciliation of the actual mining so far versus the mine plan indicates that the ore-body in the Upper Zone of the Halfmile mine is approximately 25% wider than modeled (as shown in Exhibit 1). While positive, the company does not expect this to materially change its production schedule, given that the Upper Zone represents less than 10% of the Halfmile deposit.

* Mined grades on target - So far the company has mined 37,000 tonnes of ore grading 6.39% Zn, 1.9% Pb, 0.65% Cu, 40.57 grams/tonne Ag, and 0.4 grams/tonne Au. This is essentially in-line with the mine plan for the zinc and lead grades, however, it is better-than the resource model on copper, silver, and gold.

* Inaugural ore processing - Trevali also confirmed that 30,000 tonnes of ore from Halfmile has been processed through Xstrata's nearby Brunswick-12 concentrator. This represents the first batch of Trevali's ore to be processed.

Analysis: Should the Upper Zone continue to be 25% wider than modeled, we estimate that this could contribute an additional 5 months of mining (the Halfmile mine plan currently has a mine life of 20 years). The greater width of the mineralization may also enable more efficient mining conditions due to the ability to mine larger stopes. We anticipate that Trevali will generate its first revenue in late 2Q12 from the inaugural batch of 30,000 tonnes of ore that has been processed.

Adam Low, CFA

Raymond James Ltd.

ABS:

CEO Appointment and Board Changes

VANCOUVER, BRITISH COLUMBIA, May 01, 2012 (MARKETWIRE via COMTEX) -- Abzu Gold Ltd. CA:ABS 0.00% (otcqx:ABZUF) ("Abzu") is pleased to announce that Mr. Tim McCutcheon has been appointed as CEO and Director of the Company, effective immediately.

http://www.marketwatch.com/story/ceo-appointment-and-board-c…

CMK:

Cline Mining issues US$25M in secured bonds to expand New Elk mine; stock soars

http://www.canadianbusiness.com/article/82069--cline-mining-…

--

Ich wäre sehr froh, wenn sich der User valueinvestor/DCShoes einen anderen Sandkasten suchen würde.

Zitat von boersenbrieflemming: Ich habe einmal Deine aktuelleren Tipps ( Quelle: 41.926.653) zusammengesucht.

CPN -43.40%

KAM -48.25%

MDW -32.87%

SA: -42.47% (Seabridge Gold/US)

Unverschämte Kürzung meines Postings - hier die Empfehlungen im Wortlaut von damals:

"ich denke an Papiere vom Yukon (KAM mit 75g Au auf 4 m heute gemeldet, GPD) oder MDW, CPN, PZG, PVG, SA oder auch SLX.

In einer neuerlichen Rezession sollte man nicht mehr in Kohle oder Eisen investieren. Bei kollabierenden Währungssystemen sind Silber und Gold erste Wahl."

KAM close 9.8.2011 3,42 -47,3%

GPD 1,19 -59,2%

MDW 2,25 -36,9% (USA)

CPN 0,53 -44,4%

PZG 2,32 +3,9% (USA)

SA 29,30 -45,2%

PVG 9,70 +59,7%

SLX 0,59 -8,5%

Im Durchschnitt also ein Verlust von 22,24%

Im Vergleich dazu ging der GDXJ von 33,93 31,65% in die Knie, der GLDX Global X Gold Explorers ETF verlor von 14,88 36,6%. Das ist nicht schön - diese Talfahrt der Explorer habe ich nicht vorhergesehen - aber ich bin insgesamt noch gut im Rennen.

Es spricht Bände, dass du nur selektiv die größten Verluste herausgreifst. Meine Empfehlung zu SLX hast du sogar hier in deinem Thread genassauert.

Ergänzend dazu noch die Empfehlungskurse, zu denen ich die Unternehmen zum ersten Mal erwähnt habe.

Kaminak 3,41$

Seabridge 2,36$ (erstes Posting im Thread, gekauft hatte ich ab 1,55$)

CPN 0,47$

GPD 0,7$

Pretium 6,16$

den SLX Vorläufer Genco zu um Gratisaktien bereinigte 0,24$

Midway zu 0,675$

PZG 1,36$

Dies nur als Korrektur zu dem beschämend verkürztem Herausgreifen weniger Werte aus dem Posting.

Antwort auf Beitrag Nr.: 43.112.427 von valueinvestor am 02.05.12 19:53:12Bleib mal locker.

Du hast wesentliche Bestandteile deines Postings weggelassen - du hast die Aktien in einem anderen Thread beworben und empfohlen den dort besprochenen Wert in deine katastrophale Minusriege zu tauschen.

Den Wert, aus dem man rausgehen sollte hat zwar auch eine negative Performance, diese liegt bei -12.38% und nicht zwischen -40-50%.

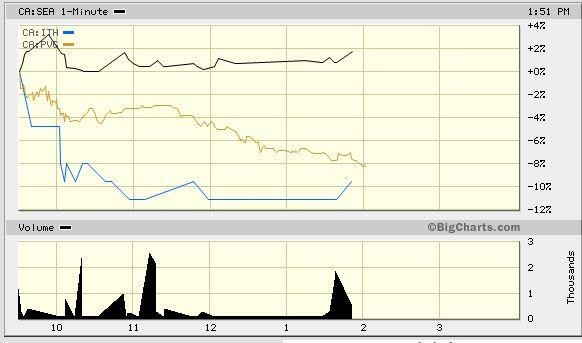

Haeufig ist das Muster aehnlich, du gehst in andere Threads praesentierst dort Aktien zu Hoechstkursen, die zumeist danach einbrechen (Bsp:: KAM, SEA, CPN, etc.pp.).

Ich erinnerne mich an Beispiele, zum Beispiel in ITH-Threads User um 0,90 Cent herauszuschreiben und SEA (damals weit jenseits der 30 USD) zu bewerben. Fakt: ITH stieg auf ueber 10 Dollar und SEA rauchte ueber 50% ab.

Ich bin da eh etwas verwundert und halte deine Empfehlungen fuer die schlechtesten, die WO an Schreibern zu bieten hat. Du kannst haeufig ja auch nicht anders, da du u.a. unter einer Explorer-E-Mail fungierst. Ich waere dir sehr dankbar, wenn du deinen Schrott hier unterlassen wuerdest. Das gilt auch fuer einige der die Antizyklisch Investieren - ich sehe derartiges Gebaren (s.o.) kritisch, auch das du E-Mail-Adressen von einem Explorer nutzt. Du ueberschaetzt dich.

Du hast wesentliche Bestandteile deines Postings weggelassen - du hast die Aktien in einem anderen Thread beworben und empfohlen den dort besprochenen Wert in deine katastrophale Minusriege zu tauschen.

Den Wert, aus dem man rausgehen sollte hat zwar auch eine negative Performance, diese liegt bei -12.38% und nicht zwischen -40-50%.

Haeufig ist das Muster aehnlich, du gehst in andere Threads praesentierst dort Aktien zu Hoechstkursen, die zumeist danach einbrechen (Bsp:: KAM, SEA, CPN, etc.pp.).

Ich erinnerne mich an Beispiele, zum Beispiel in ITH-Threads User um 0,90 Cent herauszuschreiben und SEA (damals weit jenseits der 30 USD) zu bewerben. Fakt: ITH stieg auf ueber 10 Dollar und SEA rauchte ueber 50% ab.

Ich bin da eh etwas verwundert und halte deine Empfehlungen fuer die schlechtesten, die WO an Schreibern zu bieten hat. Du kannst haeufig ja auch nicht anders, da du u.a. unter einer Explorer-E-Mail fungierst. Ich waere dir sehr dankbar, wenn du deinen Schrott hier unterlassen wuerdest. Das gilt auch fuer einige der die Antizyklisch Investieren - ich sehe derartiges Gebaren (s.o.) kritisch, auch das du E-Mail-Adressen von einem Explorer nutzt. Du ueberschaetzt dich.

Antwort auf Beitrag Nr.: 43.114.692 von boersenbrieflemming am 03.05.12 11:39:48Die Daumen sagen Alles, Thread ist ueberfluessig...

Antwort auf Beitrag Nr.: 43.114.752 von ooy am 03.05.12 11:50:33User-Depots sind doch eine hochspannende Bereicherung!

Man kann so manchmal auch lernen, dass umfangreiche Empfehlungen in anderen Threads in Wirklichkeit gar nicht immer kaufenswert sind.

Hier die aktuell im Depot angegebenen Werte:

Man kann so manchmal auch lernen, dass umfangreiche Empfehlungen in anderen Threads in Wirklichkeit gar nicht immer kaufenswert sind.

Hier die aktuell im Depot angegebenen Werte:

Bezeichnung Stueck Kauf (CAD) Kurs (CAD) heute % total %

TREVALI MINING CORP 1500 0,95 1,19 -2,1% 25,3%

CLINE MINING CORP 1300 1,98 0,97 -4,6% -51,0%

CARDERO RESOURCE CO 4500 1,01 0,86 -6,0% -14,9%

ABZU GOLD LTD. 6000 0,25 0,19 -4,1% -22,4%

Seit Kauf % -19,6%

Heute % -5,6%

Antwort auf Beitrag Nr.: 43.118.613 von DCShoes am 04.05.12 00:47:47Auch diese Aufstellung ist fehlerhaft - bei Trevali z.B. hat einen Kostenfaktor von 0,41 CAD/Share und Du hast überall die Comission vergessen.

Stockwatch:

Portfolio Value Summary as of 20:03:59 Thu 03 May 2012 ($cad)

Total $Bought cad$ 16,529

Total $Sold $ 7,066

Total Equity Cost $ 9,463

Current Equity Value $ 8,056

Your Net Return $ -1,407 -8.51%

Net Cash From Trades $ -9,463

Total Cash Deposits $ 0

Total Cash Dividends $ 0

Total Cash Withdrawls $ 0

Fixed Cash Balance in Cdn$ $ 10,000

Total Cash Balance $ 537

Current Equity Value $ 8,056

Total Portfolio Value $ 8,593

--

Ich würde mich aber dennoch freuen, wenn du mal etwas entspannst - auf mich wirkt das etwas verbissen:

Stockwatch:

Portfolio Value Summary as of 20:03:59 Thu 03 May 2012 ($cad)

Total $Bought cad$ 16,529

Total $Sold $ 7,066

Total Equity Cost $ 9,463

Current Equity Value $ 8,056

Your Net Return $ -1,407 -8.51%

Net Cash From Trades $ -9,463

Total Cash Deposits $ 0

Total Cash Dividends $ 0

Total Cash Withdrawls $ 0

Fixed Cash Balance in Cdn$ $ 10,000

Total Cash Balance $ 537

Current Equity Value $ 8,056

Total Portfolio Value $ 8,593

--

Ich würde mich aber dennoch freuen, wenn du mal etwas entspannst - auf mich wirkt das etwas verbissen:

Das ist doch mal eine gute Idee, setz dich auf die PX36 oder KC51 und entspann dich!

Antwort auf Beitrag Nr.: 43.119.421 von valueinvestor am 04.05.12 09:48:04Mopedmotoren zu verheizen und dann bei WO die dicke Lippe zu riskieren, das ist nicht meine Welt.

Antwort auf Beitrag Nr.: 43.120.288 von DCShoes am 04.05.12 12:31:04Hier noch einmal die Transaktionen:

--

Die Transaktionskosten müssen aber mit rein. Ich weiss, einem Mofamotor so richtig einzuheizen mag einfacher sein.

2012-01-04 00:00 Buy ??? TV 3000 0.95 $cad 10.00 $??? NaN NaN NaN

2012-01-04 00:00 Buy ??? CDU 2500 1.06 $cad 10.00 $??? NaN NaN NaN

2012-01-06 00:00 Buy ??? USA 1300 2.15 $cad 10.00 $??? NaN NaN NaN

2012-01-11 00:00 Buy ??? ABS 6000 0.245 $cad 10.00 $??? NaN NaN NaN

2012-02-09 00:00 Sell ??? TV -1500 1.50 $cad 10.00 $??? NaN NaN NaN

2012-02-17 00:00 Buy ??? SLX 5200 0.425 $cad 10.00 $??? NaN NaN NaN

2012-02-23 00:00 Sell ??? SLX -5200 0.48 $cad 0.00 $??? NaN NaN NaN

2012-02-28 00:00 Buy ??? CMK 1300 1.98 $cad 20.00 $??? NaN NaN NaN

2012-04-16 00:00 Sell ??? USA -1300 1.80 $cad 10.00 $??? NaN NaN NaN

2012-04-16 00:00 Buy ??? CDU 2000 0.95 $cad 10.00 $??? NaN NaN NaN

--

Die Transaktionskosten müssen aber mit rein. Ich weiss, einem Mofamotor so richtig einzuheizen mag einfacher sein.

Hurra, ich verrechne alle Aktien Kreuz und Quer, ist nicht schwer und übergehe großzügig die Einstiegskurse. Auf dem Weg zum Märchen-Millionär.

Antwort auf Beitrag Nr.: 43.120.843 von DCShoes am 04.05.12 14:24:11Zahlen sind da unerbittlich. ...

---

Du verschwendest sehr viel Zeit mit mir. Ich mache Dir einen Vorschlag: Schick mir ne BM und du darfst nach Absprache meinen Rasen mähen ( mit Motor). Im Gegenzug nervst du mich hier nicht.

---

Du verschwendest sehr viel Zeit mit mir. Ich mache Dir einen Vorschlag: Schick mir ne BM und du darfst nach Absprache meinen Rasen mähen ( mit Motor). Im Gegenzug nervst du mich hier nicht.

Antwort auf Beitrag Nr.: 43.120.919 von boersenbrieflemming am 04.05.12 14:35:19Wer sein schlecht laufendes Depot hier öffentlich darstellt hat auch ein Anrecht auf konstruktive Kritik.

Schönrechnerei hilft nämlich nicht viel, wenn es bei den Werten nur abwärts geht, dass muss man auch einem Anfänger mal sagen.

Es sind meiner Meinung nach einfach schlechte Werte im Depot, egal, was die Vergangenheit für "Gewinne" gebracht hat. Diese wurden zudem in derzeitigen Verliereraktien "angelegt" und sind nicht mehr da, dürfen also auch nicht mit beliebigen Einstandskursen verrechnet werden.

Vielleicht wäre Dein Geld in einem Indexfonds besser angelegt. Gewinner (TV) verkaufen und dafür Verlierer (Cardero etc.) kaufen ist kein so guter Anlagetip.

Schönrechnerei hilft nämlich nicht viel, wenn es bei den Werten nur abwärts geht, dass muss man auch einem Anfänger mal sagen.

Es sind meiner Meinung nach einfach schlechte Werte im Depot, egal, was die Vergangenheit für "Gewinne" gebracht hat. Diese wurden zudem in derzeitigen Verliereraktien "angelegt" und sind nicht mehr da, dürfen also auch nicht mit beliebigen Einstandskursen verrechnet werden.

Vielleicht wäre Dein Geld in einem Indexfonds besser angelegt. Gewinner (TV) verkaufen und dafür Verlierer (Cardero etc.) kaufen ist kein so guter Anlagetip.

Also ich finde das unbeschriftete Einstellen von Zahlenkolonnen wenig hilfreich. Was bedeutet oben beispielsweise die Position "???" die bei jeder Aktie aufgeführt ist, oder das dreimalige Anhängen der Buchstabenkombination NaN?

ich sehe schon, ich habe zwei meiner drei Lieblings-WO-User hier dauerhaft an der Backe.

2012-02-09 00:00 Sell ??? TV -1500 1.50 $cad 10.00 $???

TV am 9.2.2012 verkauft (1500 Stück) zum Preis von 1,50 CAD.

2012-02-09 00:00 Sell ??? TV -1500 1.50 $cad 10.00 $???

TV am 9.2.2012 verkauft (1500 Stück) zum Preis von 1,50 CAD.

dann schreibe das doch auch so.

Antwort auf Beitrag Nr.: 43.121.878 von valueinvestor am 04.05.12 17:08:21Hatte ich doch.

2012-02-09 00:00 Sell Canada TV 1500 1.50 $cad 10.00 $cad -2,240

Teilverkauf Trevali (derzeit + 56,99%)

2012-02-09 00:00 Sell Canada TV 1500 1.50 $cad 10.00 $cad -2,240

Teilverkauf Trevali (derzeit + 56,99%)

Antwort auf Beitrag Nr.: 43.121.477 von DCShoes am 04.05.12 16:05:06schlechte Werte im Depot

Sehe ich nicht so.

CDU: Eine grosse Kohlegrube (met coal) auf dem Weg zur Mine, hier warte ich ganz klar auf ein Signal, wer die CAPEX finanziert oder Verkauf des Projektes, Analystenpreisschild bei 500 Mio. - ganz klar Erweiterunspotenial.

ABS: Aussichtsreicher Goldexplorer.

TV: 1 funktionierende Mine, etwas Ueberhang aus dem letzten Financing, umweltgenehmigungen für die 2. Mine. ggf. weitere Mine, Ausweitung der Produktion.

CMK: Derzeit ein tatsächlicher Fehlgriff, bleibt aber im Depot - bei Kursen um 1. Dollar ein klarer Kauf (thermal coal).

Sehe ich nicht so.

CDU: Eine grosse Kohlegrube (met coal) auf dem Weg zur Mine, hier warte ich ganz klar auf ein Signal, wer die CAPEX finanziert oder Verkauf des Projektes, Analystenpreisschild bei 500 Mio. - ganz klar Erweiterunspotenial.

ABS: Aussichtsreicher Goldexplorer.

TV: 1 funktionierende Mine, etwas Ueberhang aus dem letzten Financing, umweltgenehmigungen für die 2. Mine. ggf. weitere Mine, Ausweitung der Produktion.

CMK: Derzeit ein tatsächlicher Fehlgriff, bleibt aber im Depot - bei Kursen um 1. Dollar ein klarer Kauf (thermal coal).

Zitat von boersenbrieflemming: CDU: Eine grosse Kohlegrube (met coal) auf dem Weg zur Mine, hier warte ich ganz klar auf ein Signal, wer die CAPEX finanziert oder Verkauf des Projektes, Analystenpreisschild bei 500 Mio. - ganz klar Erweiterunspotenial.

Genau. Seit bald 10 Jahren kündigt man bei Cardero schon einen Verkauf an:

Wie lese ich schon in einem Post aus dem Jahr 2004 beim Kurs von 2,99 (Beitrag 13.275.178):

Cardero Resource - Kursexplosion zu erwarten! (..) Nicht Start der Produktion, sondern möglichst lukrativer Verkauf des Projekts ist das Ziel von Cardero! (01.06.2004)

Wenn das nochmal 10 Jahre so geht, dann kommt das pünktlich zur Ausbildung für den Sohnemann und der Kurs sinkt um weitere 70% auf 0,27 Cents..

Denkmal und glaub nicht allen schon oft wiederholten Versprechungen.

Antwort auf Beitrag Nr.: 43.123.669 von DCShoes am 05.05.12 02:01:43Wir müssen aber nicht weiter Cardero diskutieren, es soll hier ja um Dein Depot gehen. Ich würde ja ein paar Seas mit reinnehmen :-)

Antwort auf Beitrag Nr.: 43.123.669 von DCShoes am 05.05.12 02:01:43 Nicht Start der Produktion, sondern möglichst lukrativer Verkauf des Projekts ist das Ziel von Cardero!

Was Du da schreibst ist merkwürdig. Sie haben das Port besprochene Projekt doch äußerst lukrativ verkauft - für etwas das 10fache der aufgewendeten Kosten (Aquise und Exploration) - 100. Mio. USD. Mit den Verkäufen geht es weiter: aktuell gerade Sheini und weitere werden folgen. Carbon Creek ist ein Company-Maker, ein hochinteressanter Play.

Was Du da schreibst ist merkwürdig. Sie haben das Port besprochene Projekt doch äußerst lukrativ verkauft - für etwas das 10fache der aufgewendeten Kosten (Aquise und Exploration) - 100. Mio. USD. Mit den Verkäufen geht es weiter: aktuell gerade Sheini und weitere werden folgen. Carbon Creek ist ein Company-Maker, ein hochinteressanter Play.

Antwort auf Beitrag Nr.: 43.124.344 von boersenbrieflemming am 05.05.12 12:13:27das Port besprochene Projekt = das dort besprochene Projekt

Antwort auf Beitrag Nr.: 43.124.344 von boersenbrieflemming am 05.05.12 12:13:27Mit den Verkäufen geht es weiter:

So sehe ich das auch. Die Anleger verkaufen heftigst. Hätte bei all der Werbetrommelei in diversen Foren nicht gedacht, dass es mit solchen Werten so schnell abwärts über die Klippe gehen kann.

Wenn ich das richtig sehe heute bisher schon wieder über 4% abwärts in Deinem Depot. Möchtest Du nicht auch verkaufen?

So sehe ich das auch. Die Anleger verkaufen heftigst. Hätte bei all der Werbetrommelei in diversen Foren nicht gedacht, dass es mit solchen Werten so schnell abwärts über die Klippe gehen kann.

Wenn ich das richtig sehe heute bisher schon wieder über 4% abwärts in Deinem Depot. Möchtest Du nicht auch verkaufen?

Nun bestehen zwischen den Depotwerten intensive Verflechtungen, das Management ist oft in Personalunion tätig oder tätig gewesen, es bestehen Beteiligungsverhältnisse - unter den Gesichtspunkten der Depotstruktur ist so etwas natürlich unmöglich, weil dadurch ein unglaubliches Klumpungsrisiko entsteht, was auch zu massiven Einzeltagesverlusten oberhalb der üblichen Marktvolatiulität führt.

In Wirklichkeit gibt es dieses Depopt wahrscheinlich auch gar nicht, man muss dies eher als weiteren Distributionspfad verstehen.

In Wirklichkeit gibt es dieses Depopt wahrscheinlich auch gar nicht, man muss dies eher als weiteren Distributionspfad verstehen.

Antwort auf Beitrag Nr.: 43.132.751 von valueinvestor am 07.05.12 22:07:58So, der Stand nach dem heutigen Tag:

Portfolio Value Summary as of 16:50:14 Mon 07 May 2012 ($cad)

Total $Bought cad$ 16,529

Total $Sold $ 7,066

Total Equity Cost $ 9,463

Current Equity Value $ 7,763

Your Net Return $ -1,700 -10.28%

Net Cash From Trades $ -9,463

Total Cash Deposits $ 0

Total Cash Dividends $ 0

Total Cash Withdrawls $ 0

Fixed Cash Balance in Cdn$ $ 10,000

Total Cash Balance $ 537

Current Equity Value $ 7,763

Total Portfolio Value $ 8,300

Portfolio Value Summary as of 16:50:14 Mon 07 May 2012 ($cad)

Total $Bought cad$ 16,529

Total $Sold $ 7,066

Total Equity Cost $ 9,463

Current Equity Value $ 7,763

Your Net Return $ -1,700 -10.28%

Net Cash From Trades $ -9,463

Total Cash Deposits $ 0

Total Cash Dividends $ 0

Total Cash Withdrawls $ 0

Fixed Cash Balance in Cdn$ $ 10,000

Total Cash Balance $ 537

Current Equity Value $ 7,763

Total Portfolio Value $ 8,300

Antwort auf Beitrag Nr.: 43.132.751 von valueinvestor am 07.05.12 22:07:58Was hat steht eigentlich dein Musterdepot im Antizyklischen Aktienclub? Du hast ja leider seit dem Februar nicht mehr berichtet.

!

Dieser Beitrag wurde von akummermehr moderiert. Grund: keine Quellenangabe!

Dieser Beitrag wurde von akummermehr moderiert. Grund: bitte besser belegen

... bisher sind die Verluste noch erträglich - wie sieht das bei Eurem Musterdepot des Antizyklischen Aktienklubs aus? Ich komme da auf knapp 40% Minus seit Jahresbeginn. Aber leider werden die aktuellen Zahlen ja seit Anfang Februar aus bestimmten Gründen nicht mehr veröffentlicht.

Antwort auf Beitrag Nr.: 43.137.095 von boersenbrieflemming am 08.05.12 18:35:29Ich kenne das von Dir erwähnte Depot nicht. Da macht im Gegensatz zu Deinen Aktien auch keiner Werbung für hier im Board.

Die bei Dir derzeit -26% im Depot und heute schon fast Schussfahrt um mittlerweile -6% lassen ja das schlimmste befürchten. Cardero und Abzu will man anscheinend schnellstmöglich nur noch loswerden. Der Markt hat nur noch wenige Stunden offen.. Hast Du in der aktuellen Panik auch schon geschmissen?

Die bei Dir derzeit -26% im Depot und heute schon fast Schussfahrt um mittlerweile -6% lassen ja das schlimmste befürchten. Cardero und Abzu will man anscheinend schnellstmöglich nur noch loswerden. Der Markt hat nur noch wenige Stunden offen.. Hast Du in der aktuellen Panik auch schon geschmissen?

Antwort auf Beitrag Nr.: 43.137.362 von DCShoes am 08.05.12 19:33:49Die bei Dir derzeit -26% im Depot

Unsinn.

Portfolio Value Summary as of 15:07:40 Tue 08 May 2012 ($cad)

Total $Bought cad$ 16,529

Total $Sold $ 7,066

Total Equity Cost $ 9,463

Current Equity Value $ 7,542

Your Net Return $ -1,921 -11.62%

Net Cash From Trades $ -9,463

Total Cash Deposits $ 0

Total Cash Dividends $ 0

Total Cash Withdrawls $ 0

Fixed Cash Balance in Cdn$ $ 10,000

Total Cash Balance $ 537

Current Equity Value $ 7,542

Total Portfolio Value $ 8,079

Unsinn.

Portfolio Value Summary as of 15:07:40 Tue 08 May 2012 ($cad)

Total $Bought cad$ 16,529

Total $Sold $ 7,066

Total Equity Cost $ 9,463

Current Equity Value $ 7,542

Your Net Return $ -1,921 -11.62%

Net Cash From Trades $ -9,463

Total Cash Deposits $ 0

Total Cash Dividends $ 0

Total Cash Withdrawls $ 0

Fixed Cash Balance in Cdn$ $ 10,000

Total Cash Balance $ 537

Current Equity Value $ 7,542

Total Portfolio Value $ 8,079

Antwort auf Beitrag Nr.: 43.137.901 von boersenbrieflemming am 08.05.12 21:09:00ja, wenn Du alte Gewinne gegenrechnest sind es natürlich nur 9 Prozent Verlust.

Ich meine aber die konkreten Werte im Depot.

Die haben gegenüber ihrem Einstandskurs über 23% Verlust. Den gesamten alten Gewinn und dazu noch 9% der Ausgangssumme wieder in den Sand gesetzt.

Ich meine aber die konkreten Werte im Depot.

Die haben gegenüber ihrem Einstandskurs über 23% Verlust. Den gesamten alten Gewinn und dazu noch 9% der Ausgangssumme wieder in den Sand gesetzt.

Antwort auf Beitrag Nr.: 43.138.191 von DCShoes am 08.05.12 22:05:43Suche dir bitte einen anderen Betreuer. Das ist ja schon Stalking.

Antwort auf Beitrag Nr.: 43.138.263 von boersenbrieflemming am 08.05.12 22:19:17Stalking?

Nimms nicht persönlich, mir geht es nicht um Deine Person. Die beworbenen Werte stehen hier im Vordergrund und die nackten Zahlen, die man nicht schönreden kann.

Nimms nicht persönlich, mir geht es nicht um Deine Person. Die beworbenen Werte stehen hier im Vordergrund und die nackten Zahlen, die man nicht schönreden kann.

Antwort auf Beitrag Nr.: 43.138.263 von boersenbrieflemming am 08.05.12 22:19:17Gegen Profis, die auf Ihrer Dropboxseite Cardero-Nachrichten bereitstellen und Präsentationen zum Download anbieten, ist ein 'Laie' als Forumsteilnehmer mit seinen Argumenten wohl machtlos.

Viel Glück mit Deinem Depot. Doll schauts nicht aus.

Hier eine von vielen Werbungen:

http://www.facebook.com/permalink.php?story_fbid=16282629378…

Viel Glück mit Deinem Depot. Doll schauts nicht aus.

Hier eine von vielen Werbungen:

http://www.facebook.com/permalink.php?story_fbid=16282629378…

Der Link interessiert mich, da ich mir gerne einen Überblick über die verschiedenen Werbeformen und -kanäle mache. Kannst du ihn noch einmal komplett einstellen?

Antwort auf Beitrag Nr.: 43.139.136 von valueinvestor am 09.05.12 08:19:03Du koennstest schon einmal damit anfangen und erklaeren, warum du zum Beispiel den "Zustand" des Musterdepots (Antizyklischer Aktienclub) seit Februar nicht mehr darstellst.

!

Dieser Beitrag wurde von MODernist moderiert. Grund: keine/ausreichende Quellenangabe, ggf. überarbeitet wieder einstellen

Antwort auf Beitrag Nr.: 43.140.003 von boersenbrieflemming am 09.05.12 10:48:27Ich meine mich zu erinnern, dass du an anderer Stelle behauptet hast, in besagtem Forum keine Leserechte zu haben. Was stimmt den nun?

Im übrigen hat es keine Veränderung an der Zusammensetzung gegeben. Mein Anlagehorizont ist auch sehr lange, ich bin kein hektischer Daytrader, viele Werte sind schon seit Jahren in meinem Depot, da muss ich nicht alle Nas lang Aktualisierungen posten.

Im übrigen hat es keine Veränderung an der Zusammensetzung gegeben. Mein Anlagehorizont ist auch sehr lange, ich bin kein hektischer Daytrader, viele Werte sind schon seit Jahren in meinem Depot, da muss ich nicht alle Nas lang Aktualisierungen posten.

Antwort auf Beitrag Nr.: 43.141.707 von valueinvestor am 09.05.12 15:42:01Ich bin kein Mitglied im Antizyklischen Aktienklub und beziehe auch keine Newsletter, Boersenbriefe oder dergleichen. Mir wurden u.a. die Transaktionen von Usern weitergeleitet - das Depot ist schwer nachvollziehbar. Ich komme auf über 50% Minus seit dem 31.12. 2010, exklusive der Transaktionskosten über die letzten 10 Jahre. Deswegen verstehe ich nicht, warum du hier bei einem moderaten Minus mir hier dermassen auf den Senkel gehen musst.

Noch 2 Analystenerwaehnungen zu den Depotwerten CDU und CMK (beide mit einem Target von 3 Dollar):

COVERAGE SUMMARY

Investment Thesis

Cardero Resource Corp. (TSX-CDU) Recommendation: SPECULATIVE BUY Mkt Cap ($mm) $80.0 Previous Close: $0.87 12-Month Target: $3.00 Potential Return 244.8%

???? Canadian-listed play on metallurgical coal – Metallurgical coal is a major input requirement in global steel manufacturing, with global steel demand expected to grow at a 4% CAGR through 2020. The Carbon Creek project could be producing by early 2014, with full production capacity of 2.9 million tonnes per year (mtpy) achievable by 2016.

Positive PEA results – On a 75% basis, the project has a post-tax NPV of $752 million at an 8% discount rate, an IRR of 29.3% and 3-year payback from the production start. The PEA also includes an upgraded resource estimate, with a 46% increase in M&I resources to 167 mt and an 87% increase in Inferred resource to 167 mt.

Well-established metallurgical coal producing region – The Carbon Creek project is located in the Peace River Coalfield in northeast B.C. Other operators/developers in the region include Xstrata (LSE-XTA) (via its recent acquisition of First Coal), Anglo American (LSE-AAL) and Walter Energy (TSX; NYSE-WLT).

Experienced management team – Mr. Michael Hunter, the President of CDU, was also a co-founder of First Coal. CDU also recently appointed a new Chief Operating Officer, Mr. Angus Christie (ex-Anglo Coal).

Near-term catalysts

o Q2/12 – Obtaining the outstanding mining licence.

o Q2-Q3/12 – Terminal access agreement with Ridley Terminals. o Q3/12 – Pre-feasibility study.

o Potential monetization of non-core assets.

Cline Mining Corporation (TSX-CMK) Recommendation: SPECULATIVE BUY Mkt Cap ($mm) $184.0 Previous Close: $0.88 12-Month Target: $3.00 Potential Return 240.9%#

Investment Thesis

Near-term, fully-financed production potential – We believe CMK should be able to reach its target production rate of 3.0 mtpy in 2013, without requiring additional equity financing. The Company also recently sold its Lossan coal property for $40 million and issued senior secured notes of US$50 million. CMK’s first commercial shipment (made August 9, 2011) met the full specification grade for steelmaking purposes.

Additional production growth update – Resource could support production of 6.0 million tons/year (May 2011 NI 43-101 estimate Measured & Indicated 388.5 million tons). CMK is evaluating the potential for increasing its production capacity from 3.0 mtpy to 7.0 mtpy via a transition to longwall mining.

Near-term catalysts

o Q1/12 Operational update (early-May 2012) and Q1/12 financial results (mid-May 2012). o H2/12 – Decision on longwall transition opportunity.

o Potential monetization of non-core assets.

Production Guidance

FY 2012 – 1.7 million tonnes; FY 2013 – 3.0 million tonnes.

Quelle: http://www.jenningscapital.com/reports/CoalNotes20120507.pdf (ggf. kostenlose Registrierung notwendig)

Kopie: http://www.dateienohnewert.com/ditunddat/analuesten/CoalNote…

COVERAGE SUMMARY

Investment Thesis

Cardero Resource Corp. (TSX-CDU) Recommendation: SPECULATIVE BUY Mkt Cap ($mm) $80.0 Previous Close: $0.87 12-Month Target: $3.00 Potential Return 244.8%

???? Canadian-listed play on metallurgical coal – Metallurgical coal is a major input requirement in global steel manufacturing, with global steel demand expected to grow at a 4% CAGR through 2020. The Carbon Creek project could be producing by early 2014, with full production capacity of 2.9 million tonnes per year (mtpy) achievable by 2016.

Positive PEA results – On a 75% basis, the project has a post-tax NPV of $752 million at an 8% discount rate, an IRR of 29.3% and 3-year payback from the production start. The PEA also includes an upgraded resource estimate, with a 46% increase in M&I resources to 167 mt and an 87% increase in Inferred resource to 167 mt.

Well-established metallurgical coal producing region – The Carbon Creek project is located in the Peace River Coalfield in northeast B.C. Other operators/developers in the region include Xstrata (LSE-XTA) (via its recent acquisition of First Coal), Anglo American (LSE-AAL) and Walter Energy (TSX; NYSE-WLT).

Experienced management team – Mr. Michael Hunter, the President of CDU, was also a co-founder of First Coal. CDU also recently appointed a new Chief Operating Officer, Mr. Angus Christie (ex-Anglo Coal).

Near-term catalysts

o Q2/12 – Obtaining the outstanding mining licence.

o Q2-Q3/12 – Terminal access agreement with Ridley Terminals. o Q3/12 – Pre-feasibility study.

o Potential monetization of non-core assets.

Cline Mining Corporation (TSX-CMK) Recommendation: SPECULATIVE BUY Mkt Cap ($mm) $184.0 Previous Close: $0.88 12-Month Target: $3.00 Potential Return 240.9%#

Investment Thesis

Near-term, fully-financed production potential – We believe CMK should be able to reach its target production rate of 3.0 mtpy in 2013, without requiring additional equity financing. The Company also recently sold its Lossan coal property for $40 million and issued senior secured notes of US$50 million. CMK’s first commercial shipment (made August 9, 2011) met the full specification grade for steelmaking purposes.

Additional production growth update – Resource could support production of 6.0 million tons/year (May 2011 NI 43-101 estimate Measured & Indicated 388.5 million tons). CMK is evaluating the potential for increasing its production capacity from 3.0 mtpy to 7.0 mtpy via a transition to longwall mining.

Near-term catalysts

o Q1/12 Operational update (early-May 2012) and Q1/12 financial results (mid-May 2012). o H2/12 – Decision on longwall transition opportunity.

o Potential monetization of non-core assets.

Production Guidance

FY 2012 – 1.7 million tonnes; FY 2013 – 3.0 million tonnes.

Quelle: http://www.jenningscapital.com/reports/CoalNotes20120507.pdf (ggf. kostenlose Registrierung notwendig)

Kopie: http://www.dateienohnewert.com/ditunddat/analuesten/CoalNote…

Antwort auf Beitrag Nr.: 43.144.154 von boersenbrieflemming am 09.05.12 22:48:15Wie oft denn noch??

Welch schamlose Versprechungs-Analyse. Kaum sind die "2 Analystenerwaehnungen zu den Depotwerten CDU und CMK" raus, gehts im Depot um über 6% runter:

Die Pennyrutscher:

Cline -13,41% (!)

Cardero -4,71%

Und dafür so ein Thread?

Die Pennyrutscher:

Cline -13,41% (!)

Cardero -4,71%

Und dafür so ein Thread?

Antwort auf Beitrag Nr.: 43.164.775 von DCShoes am 15.05.12 00:26:22Bei Cline stehen die Produktionszahlen (erwarte ich bereits) noch aus, die Finanzzahlen (Q1) kommen wohl morgen. Es gibt da naturgemaess diverse Gerüchte. Mal schauen, bei Cline ist ein Phänomen - das ist der erste (von insgesamt 7-8) vergruetzte Trade mit der Company und ich lag da massiv daneben.

!

Dieser Beitrag wurde von MODernist moderiert. Grund: keine/ausreichende Quellenangabe, ggf. überarbeitet wieder einstellen

Antwort auf Beitrag Nr.: 43.164.806 von boersenbrieflemming am 15.05.12 01:06:21Verlust der aktuellen Depotwerte gegenüber Einstandskurs: -30%

Cline derzeit mit sagenhaften -59% dabei.

Auch ohne Cline liegen die restlichen Depotwerte, nämlich Trevali und die Pennyrutscher Cardero und Abzu rund 20% in den Miesen.

Für ein Musterdepot ist das wirklich vergrüzt. Umso schlimmer, dass vom Depotführer in anderen Boards erfolgreiche Aktien schlechtgemacht werden. Da sind eindeutig die Maßstäbe verrutscht.

Cline derzeit mit sagenhaften -59% dabei.

Auch ohne Cline liegen die restlichen Depotwerte, nämlich Trevali und die Pennyrutscher Cardero und Abzu rund 20% in den Miesen.

Für ein Musterdepot ist das wirklich vergrüzt. Umso schlimmer, dass vom Depotführer in anderen Boards erfolgreiche Aktien schlechtgemacht werden. Da sind eindeutig die Maßstäbe verrutscht.

Da es gemeldet und anschliessend wegen nicht ausreichender Quellenangabe gelöscht wurde - für Cline-Shareholder ist die Absenkung des Kurszieles von Jennings Capital durchaus eine Erwähnung wert.

Kalender-Jahr .... 2012 ............. 2013

Produktion: ....... 0,4 Mio. t ... 1,5 Mio. t

Gewinn/Aktie in C$: -0,07 ......... +0,17

Hier ein kleiner Auszug:

CLINE MINING CORPORATION

(TSX-CMK $0.69)

Previous 12-Month Target: $3.00

New Target: $1.75

Risk Rating: ABOVE AVERAGE

REDUCING TARGET ON GUIDANCE CUT

Kalender-Jahr .... 2012 ............. 2013

Produktion: ....... 0,4 Mio. t ... 1,5 Mio. t

Gewinn/Aktie in C$: -0,07 ......... +0,17

Hier ein kleiner Auszug:

CLINE MINING CORPORATION

(TSX-CMK $0.69)

Previous 12-Month Target: $3.00

New Target: $1.75

Risk Rating: ABOVE AVERAGE

REDUCING TARGET ON GUIDANCE CUT

Antwort auf Beitrag Nr.: 43.219.260 von boersenbrieflemming am 29.05.12 04:01:04Der als angebliche "Quelle" angegebenen Beitrag ist nur eine 1:1-Kopie und bezeichnet keine genauere Herkunft. Den von dir zitierten Artikel gibt es nach eigener Recherche wohl bei Jenningscapital nach Anmeldung zu beziehen.

Ob da in den angesichts der hehren Kurziele wohl auch drinnen steht, dass für das gute Covering satte Prämien bezahlt werden? Man kann es nur vermuten und mangels vollständigen Zitats leider nicht nachprüfen.

Aber auch andere senken das Kurziel merklich in den Penny-Bereich:

16 May 2012 – TO :

Cline Mining Corp : TD Securities cuts to reduce from hold

Cline Mining Corp : TD Securities cuts price target to C$0.65 from C$1.50

https://research.tdwaterhouse.ca/research/public/Stocks/News…

Ob da in den angesichts der hehren Kurziele wohl auch drinnen steht, dass für das gute Covering satte Prämien bezahlt werden? Man kann es nur vermuten und mangels vollständigen Zitats leider nicht nachprüfen.

Aber auch andere senken das Kurziel merklich in den Penny-Bereich:

16 May 2012 – TO :

Cline Mining Corp : TD Securities cuts to reduce from hold

Cline Mining Corp : TD Securities cuts price target to C$0.65 from C$1.50

https://research.tdwaterhouse.ca/research/public/Stocks/News…

Antwort auf Beitrag Nr.: 43.222.445 von DCShoes am 29.05.12 18:20:14Mein lieber Stalker, Unter deinem Link können die von dir genannten Kursziele nicht gefunden werden. Das hast du dir dann wohl ausgedacht, das wäre auch nicht ungewöhnlich.

http://research.tdwaterhouse.ca/research/public/Stocks/NewsA…

http://research.tdwaterhouse.ca/research/public/Stocks/NewsA…

Antwort auf Beitrag Nr.: 43.222.754 von boersenbrieflemming am 29.05.12 19:20:50Stalker ist aber eine wüste Beschimpfung. Darf ich Dich im Gegenzug Pusher nennen?

Hier wird der Link zur Quelle nachgereicht. Da obiger Link nicht mehr funktioniert:

http://www.chicagotribune.com/sns-rt-canadaresearchl4e8gg7v5…

Hier wird der Link zur Quelle nachgereicht. Da obiger Link nicht mehr funktioniert:

http://www.chicagotribune.com/sns-rt-canadaresearchl4e8gg7v5…

Antwort auf Beitrag Nr.: 43.222.884 von DCShoes am 29.05.12 19:46:15Das Niveau in Deinem Depot sinkt merklich, wenn Du sogar anfängst, die Leser zu beschimpfen.

Antwort auf Beitrag Nr.: 43.222.884 von DCShoes am 29.05.12 19:46:15Stalker ist aber eine wüste Beschimpfung.

Denk mal darüber nach.

Denk mal darüber nach.

Van Sun says Cline sues B.C. for $500-million

Cline Mining Corp (C:CMK)

Shares Issued 208,626,977

Last Close 5/29/2012 $0.95

Wednesday May 30 2012 - In the News

The Vancouver Sun reports in its Wednesday edition that Cline Mining has filed a $500-million lawsuit against the B.C. government after losing a series of mining claims in the Flathead Valley in the southeast. The Sun's Scott Simpson writes that Cline's action comes 27 months after the province yielded to pressure from environmentalists and the U.S. government to halt mining activity on the Canadian side of the environmentally sensitive Flathead, which is within Glacier National Park in Montana. Cline announced Tuesday it has filed a notice of civil claim in B.C. Supreme Court, seeking a declaration that its mineral rights under its coal licences and coal-licence applications, for the Lodgpole, Sage Creek and Cabin Creek properties, "were expropriated, taken or injuriously affect by the province's passing of the [Flathead Watershed Conservation] Act. "Cline is also seeking compensation including, but not limited to, the loss of the value of the licenses and applications for licenses for these properties, estimated at in excess of $500-million on a net present value basis over the expected lives of the mines. Cline has retained Fraser Milner Casgrain LLP. Its shares closed at 95 cents, up four cents.

Cline Mining Corp (C:CMK)

Shares Issued 208,626,977

Last Close 5/29/2012 $0.95

Wednesday May 30 2012 - In the News

The Vancouver Sun reports in its Wednesday edition that Cline Mining has filed a $500-million lawsuit against the B.C. government after losing a series of mining claims in the Flathead Valley in the southeast. The Sun's Scott Simpson writes that Cline's action comes 27 months after the province yielded to pressure from environmentalists and the U.S. government to halt mining activity on the Canadian side of the environmentally sensitive Flathead, which is within Glacier National Park in Montana. Cline announced Tuesday it has filed a notice of civil claim in B.C. Supreme Court, seeking a declaration that its mineral rights under its coal licences and coal-licence applications, for the Lodgpole, Sage Creek and Cabin Creek properties, "were expropriated, taken or injuriously affect by the province's passing of the [Flathead Watershed Conservation] Act. "Cline is also seeking compensation including, but not limited to, the loss of the value of the licenses and applications for licenses for these properties, estimated at in excess of $500-million on a net present value basis over the expected lives of the mines. Cline has retained Fraser Milner Casgrain LLP. Its shares closed at 95 cents, up four cents.

Antwort auf Beitrag Nr.: 43.227.173 von boersenbrieflemming am 30.05.12 15:23:05Die Klage reisst Cline heute bisher über 7% in die Tiefe. Wie Du ja selbst im Seabridge-Thread oft betonst, sind Rechtsstreitigkeiten meist langwierig und mit hohen Risiken verbunden. Der Markt reagiert sofort.

Noch erschreckender ist, wie es Deinen Depotwert ABZU heute herumgewirbelt wird. -11% bisher. Was ist da los? Ausverkauf? Das wird bald einstelliger Pennybereich.

Immerhin hält Trevali das Depot (-30% seit Einstandskursen) noch etwas oben.

Ist sicherlich auch ein schwieriger Markt und ein wenig diversifiziertes Depot. Hast Du gedankliche Stopp-Kurse für die einzelnen Werte festgelegt?

Noch erschreckender ist, wie es Deinen Depotwert ABZU heute herumgewirbelt wird. -11% bisher. Was ist da los? Ausverkauf? Das wird bald einstelliger Pennybereich.

Immerhin hält Trevali das Depot (-30% seit Einstandskursen) noch etwas oben.

Ist sicherlich auch ein schwieriger Markt und ein wenig diversifiziertes Depot. Hast Du gedankliche Stopp-Kurse für die einzelnen Werte festgelegt?

Antwort auf Beitrag Nr.: 43.227.860 von DCShoes am 30.05.12 17:00:20ABS ist derzeit im Plus - hier fehlen noch der ein oder andere Parameter, die dem Kurs auf die Beine helfen koennen.

Da du SEA erwaehnst - hier sehe ich zusaetzlich Parallelen zum Flathead Valley. Die Story ist empfehlenswert.

Zu Explorer-Depot nach ein Update:

Portfolio Value Summary as of 15:14:23 Wed 30 May 2012 ($cad)

Total $Bought cad$ 16,529

Total $Sold $ 7,066

Total Equity Cost $ 9,463

Current Equity Value $ 7,223

Your Net Return $ -2,240 -13.55%

Net Cash From Trades $ -9,463

Total Cash Deposits $ 0

Total Cash Dividends $ 0

Total Cash Withdrawls $ 0

Fixed Cash Balance in Cdn$ $ 10,000

Total Cash Balance $ 537

Current Equity Value $ 7,223

Total Portfolio Value $ 7,760

--

wenig diversifiziertes Depot

Hier geht es nicht um einen Millionenbetrag, sondern um 10.000 CAD - da muss man mehr Risiko eingehen und kann nicht gross diversifizieren.

gedankliche Stopp-Kurse

Nein. Auch Cline bleibt im Depot, weil ich hier einen Betrag von 1 CAD/Share (+/- 25%) ohne weiteres als Unterbewertung ansehe.