CASTLE GOLD Corp. -- Produzent und Explorer - 500 Beiträge pro Seite

eröffnet am 19.11.07 11:40:13 von

neuester Beitrag 15.11.09 16:55:08 von

neuester Beitrag 15.11.09 16:55:08 von

Beiträge: 585

ID: 1.135.412

ID: 1.135.412

Aufrufe heute: 0

Gesamt: 32.791

Gesamt: 32.791

Aktive User: 0

Top-Diskussionen

| Titel | letzter Beitrag | Aufrufe |

|---|---|---|

| 06.03.17, 11:10 | 162 | |

| gestern 07:52 | 160 | |

| gestern 23:22 | 147 | |

| heute 00:57 | 117 | |

| 29.01.15, 14:48 | 111 | |

| gestern 23:16 | 110 | |

| heute 00:37 | 108 | |

| 28.09.06, 14:49 | 100 |

Meistdiskutierte Wertpapiere

| Platz | vorher | Wertpapier | Kurs | Perf. % | Anzahl | ||

|---|---|---|---|---|---|---|---|

| 1. | 1. | 18.740,00 | -0,01 | 103 | |||

| 2. | 2. | 6,3980 | -1,31 | 82 | |||

| 3. | 3. | 186,60 | +6,66 | 50 | |||

| 4. | 4. | 10,310 | -4,27 | 45 | |||

| 5. | 5. | 5,6300 | -1,12 | 32 | |||

| 6. | 6. | 97,63 | -11,41 | 31 | |||

| 7. | 7. | 70.083,08 | -1,41 | 30 | |||

| 8. | 9. | 0,1570 | +2,95 | 28 |

Hallo allerseits !

Habe diese Fa. gefunden, die bereits aus dem Explorer - Stadium heraus ist und seit einigen Monaten selbst produziert (eine Mine zu 100% im Eigentum, eine zweite zu 50%). Es wurde bereits das erste selbst produzierte Gold verkauft.

Damit erschöpfen sich aber meine Erkenntnisse.

Weiß jemand mehr über diese Co.?

Hörte sich interessant an, weil sie im Vergleich zu vielen anderen - in dieser "interessanten" Zeit - bereits produzieren.

Habe diese Fa. gefunden, die bereits aus dem Explorer - Stadium heraus ist und seit einigen Monaten selbst produziert (eine Mine zu 100% im Eigentum, eine zweite zu 50%). Es wurde bereits das erste selbst produzierte Gold verkauft.

Damit erschöpfen sich aber meine Erkenntnisse.

Weiß jemand mehr über diese Co.?

Hörte sich interessant an, weil sie im Vergleich zu vielen anderen - in dieser "interessanten" Zeit - bereits produzieren.

Antwort auf Beitrag Nr.: 32.478.254 von VeuveClicquot am 19.11.07 12:17:59Ja, danke für die Adresse.

Allerdings geht die Frage natürlich auch in die Richtung, ob das, was die dort machen zukunftsträchtig ist, ob es sich lohnt, dort "einzusteigen", etc.

Welche Kriterien sprechen dafür, dagegen, usw.

Anfang des Monats hat wohl der Präsident Guatemalas verkündet, dass Guatemala (dort liegt eine der gerade von Castle Gold betriebenen Minen) allen Firmen, die zwar Claims halten (ist wohl sehr billig) aber bis heute nicht explorieren und/oder nicht produzieren, die Rechte entzieht. Das spräche ja durchaus FÜR Castle Gold...!?!?

Ich bin unsicher, was meine Meinungsbildung angeht und bitte daher um ein paar mehr Details.

Allerdings geht die Frage natürlich auch in die Richtung, ob das, was die dort machen zukunftsträchtig ist, ob es sich lohnt, dort "einzusteigen", etc.

Welche Kriterien sprechen dafür, dagegen, usw.

Anfang des Monats hat wohl der Präsident Guatemalas verkündet, dass Guatemala (dort liegt eine der gerade von Castle Gold betriebenen Minen) allen Firmen, die zwar Claims halten (ist wohl sehr billig) aber bis heute nicht explorieren und/oder nicht produzieren, die Rechte entzieht. Das spräche ja durchaus FÜR Castle Gold...!?!?

Ich bin unsicher, was meine Meinungsbildung angeht und bitte daher um ein paar mehr Details.

Wert hält sich in Can. (und auch hier, obwohl ihn keiner zu kenn scheint)min. genauso gut wie andere Rohstoffwerte.

Habe dann doch ein paar shares gekauft. Viel falsch machen kann man - denke ich - ja nicht.

Allerdings ginge es mir besser, wenn mir ein "Wissender" mehr Bewertungsgrundlagen geben könnte...

Habe dann doch ein paar shares gekauft. Viel falsch machen kann man - denke ich - ja nicht.

Allerdings ginge es mir besser, wenn mir ein "Wissender" mehr Bewertungsgrundlagen geben könnte...

Guten Tag,

wie es scheint, hält sich - zumindest in Can. - die Castle Gold Corp. (CSG) gar nicht 'mal so schlecht.

Immerhin leicht gestiegen.

Scheint in D nicht sehr bekannt zu sein, deshalb gibt es hier auch keinen wirklichen Umsatz/Handel mit dieser Aktie.

Wer weiß, möglicherweise hat das auch was damit zu tun, dass bei dieser Fa. produziert und auch verkauft wird (Gold nämlich)...?!?

wie es scheint, hält sich - zumindest in Can. - die Castle Gold Corp. (CSG) gar nicht 'mal so schlecht.

Immerhin leicht gestiegen.

Scheint in D nicht sehr bekannt zu sein, deshalb gibt es hier auch keinen wirklichen Umsatz/Handel mit dieser Aktie.

Wer weiß, möglicherweise hat das auch was damit zu tun, dass bei dieser Fa. produziert und auch verkauft wird (Gold nämlich)...?!?

Trading Spotlight

Endlich mal ein Thread zu diesem Top-Wert.

Ich bin schon seit ~2 Wochen dabei. Wenn das erzkonservative Management (O-Ton aus SH) seine Prognosen einhält hätten wir zum Jahresende 27500 Unzen Produktion aus 2 (!) Minen zu sehr niedrigen Abbaukosten.

Für 2008 würde der Abbau auf deutlich über 40000 Unzen ansteigen.

Oder anders: bei 500 USD Gewinn pro Unze läge CSG bei 20Mio Gewinn, und er Kurs sollte bei 70Mio Aktien bei über 2,50 stehen.

Sehr beachtlich sind auch die beachtlichen P+P Reserves (~500TSd) und die Inferred Res. (~500Tsd) mit Potenzial auf weitere Erhöhung.

Der eigentliche Witz ist aber die derzeitige MK bei 2 produzierenden Minen: 50 Mio CAD. Bin sehr zuversichtlich, dass CSG spätestens nach Bekanntgabe des Status zur zweiten Mine zum Jahresende einen gewaltigen Satz nach oben machen wird.

Ich bin schon seit ~2 Wochen dabei. Wenn das erzkonservative Management (O-Ton aus SH) seine Prognosen einhält hätten wir zum Jahresende 27500 Unzen Produktion aus 2 (!) Minen zu sehr niedrigen Abbaukosten.

Für 2008 würde der Abbau auf deutlich über 40000 Unzen ansteigen.

Oder anders: bei 500 USD Gewinn pro Unze läge CSG bei 20Mio Gewinn, und er Kurs sollte bei 70Mio Aktien bei über 2,50 stehen.

Sehr beachtlich sind auch die beachtlichen P+P Reserves (~500TSd) und die Inferred Res. (~500Tsd) mit Potenzial auf weitere Erhöhung.

Der eigentliche Witz ist aber die derzeitige MK bei 2 produzierenden Minen: 50 Mio CAD. Bin sehr zuversichtlich, dass CSG spätestens nach Bekanntgabe des Status zur zweiten Mine zum Jahresende einen gewaltigen Satz nach oben machen wird.

Duie nEws war z.B. wichtig von ende September:

Castle Gold Corp

Castle Gold Sells First El Castillo Gold at US $715 Per Ounce

9/27/2007

TORONTO, ONTARIO, Sep 27, 2007 (MARKET WIRE via COMTEX News Network) --

Castle Gold Corporation ("Castle Gold" or the "Company") (TSX VENTURE: CSG) announces the first gold sale from its 100% owned El Castillo mine in Durango, Mexico. The Company capitalized on the recent increase in the price of gold by selling 450 ounces at an average realized price of US$715 per ounce. This first sale of El Castillo gold represents production from the first month-and-a-half of pre-production leaching that began in July.

Production at El Castillo is ramping up to the initial operating rate of 200,000 tonnes of ore and waste per month. Ore is currently being placed on the leach pad at a rate of 75,000 tonnes per month and will increase to 100,000 tonnes per month over the next two months as the pit is developed. Further increases to Castillo's production rate are planned for 2008.

The El Castillo mine is expected to be producing at a rate of 15,000 ounces of gold per year by year end. The gold production rate is forecast to increase to 30,000 ounces per year during 2008. Consideration will also be given to expanding the production rates beyond 30,000 ounces of gold per year through one or two additional expansions.

"I am very pleased that our mine building team has successfully built a second mine in less than two years," stated Christopher Babcock, President and CEO of Castle Gold. "This tremendous achievement epitomizes our mining objectives of focusing on the fundamentals, enhancing efficiencies, growing production rates, and thereby profitability, at our two producing gold mines. We could not be more excited about the timing of these events with the price of gold extending to new highs coincident with the ramp-up of the gold production at El Castillo."

Darren Koningen (P. Eng.), Vice-President - Operations, is the Qualified Person under National Instrument 43-101 for the El Castillo Mine.

Castle Gold is a growth oriented gold producer focused on expanding gold production within the Americas. Castle Gold owns a 100% interest in the El Castillo gold mine in Mexico and a 50% interest in the El Sastre gold mine in Guatemala. Castle Gold is also advancing exploration and development work at its La Fortuna gold project in Mexico and at its El Sastre, Bridge and Lupita projects in Guatemala.

Current issued and outstanding share capital: 70,195,647

Castle Gold Corp

Castle Gold Sells First El Castillo Gold at US $715 Per Ounce

9/27/2007

TORONTO, ONTARIO, Sep 27, 2007 (MARKET WIRE via COMTEX News Network) --

Castle Gold Corporation ("Castle Gold" or the "Company") (TSX VENTURE: CSG) announces the first gold sale from its 100% owned El Castillo mine in Durango, Mexico. The Company capitalized on the recent increase in the price of gold by selling 450 ounces at an average realized price of US$715 per ounce. This first sale of El Castillo gold represents production from the first month-and-a-half of pre-production leaching that began in July.

Production at El Castillo is ramping up to the initial operating rate of 200,000 tonnes of ore and waste per month. Ore is currently being placed on the leach pad at a rate of 75,000 tonnes per month and will increase to 100,000 tonnes per month over the next two months as the pit is developed. Further increases to Castillo's production rate are planned for 2008.

The El Castillo mine is expected to be producing at a rate of 15,000 ounces of gold per year by year end. The gold production rate is forecast to increase to 30,000 ounces per year during 2008. Consideration will also be given to expanding the production rates beyond 30,000 ounces of gold per year through one or two additional expansions.

"I am very pleased that our mine building team has successfully built a second mine in less than two years," stated Christopher Babcock, President and CEO of Castle Gold. "This tremendous achievement epitomizes our mining objectives of focusing on the fundamentals, enhancing efficiencies, growing production rates, and thereby profitability, at our two producing gold mines. We could not be more excited about the timing of these events with the price of gold extending to new highs coincident with the ramp-up of the gold production at El Castillo."

Darren Koningen (P. Eng.), Vice-President - Operations, is the Qualified Person under National Instrument 43-101 for the El Castillo Mine.

Castle Gold is a growth oriented gold producer focused on expanding gold production within the Americas. Castle Gold owns a 100% interest in the El Castillo gold mine in Mexico and a 50% interest in the El Sastre gold mine in Guatemala. Castle Gold is also advancing exploration and development work at its La Fortuna gold project in Mexico and at its El Sastre, Bridge and Lupita projects in Guatemala.

Current issued and outstanding share capital: 70,195,647

Antwort auf Beitrag Nr.: 32.547.734 von Rainolaus am 24.11.07 12:24:50> Endlich mal ein Thread zu diesem Top-Wert.

Tja,

da ich - wie gesagt - diese Firma irgendwann einmal gefunden hatte, dachte ich mir, dass es ja seltsam ist, dass hier niemand etwas dazu geschrieben hatte...

Deshalb habe ich den Thread gestartet.

Die "Verlautbarungen" der Gesellschaft selbst hatte ich natürlich dann auch gelesen, wollte aber gerne andere Meinungen hören...

In Can. haben sie auch die letzten Tage wieder etwas zugelegt.

Allerdings scheint es mir auch so, dass Castle Gold doch ziemlich unterbewertet ist (auch in Hinblick auf die geänderte Lage in Guatemala). Schließlich ist das hier ein Produzent und keiner der vielen Explorer, die Produzent werden wollen. (Es gibt natürlich auch sehr vielversprechende Werte, die ganz kurz vor der Produktion stehen - die wollen wir ja 'mal nicht vergessen...)

...

Wenn jetzt nicht wieder irgendeine (neue?) Krise dazwischen kommt, die das Vertrauen vieler Leute reduzieren könnte, sollte sich eigentlich eine nette Steigerung ergeben können. Das ist jedenfalls meine persönliche Meinung...

Tja,

da ich - wie gesagt - diese Firma irgendwann einmal gefunden hatte, dachte ich mir, dass es ja seltsam ist, dass hier niemand etwas dazu geschrieben hatte...

Deshalb habe ich den Thread gestartet.

Die "Verlautbarungen" der Gesellschaft selbst hatte ich natürlich dann auch gelesen, wollte aber gerne andere Meinungen hören...

In Can. haben sie auch die letzten Tage wieder etwas zugelegt.

Allerdings scheint es mir auch so, dass Castle Gold doch ziemlich unterbewertet ist (auch in Hinblick auf die geänderte Lage in Guatemala). Schließlich ist das hier ein Produzent und keiner der vielen Explorer, die Produzent werden wollen. (Es gibt natürlich auch sehr vielversprechende Werte, die ganz kurz vor der Produktion stehen - die wollen wir ja 'mal nicht vergessen...)

...

Wenn jetzt nicht wieder irgendeine (neue?) Krise dazwischen kommt, die das Vertrauen vieler Leute reduzieren könnte, sollte sich eigentlich eine nette Steigerung ergeben können. Das ist jedenfalls meine persönliche Meinung...

Antwort auf Beitrag Nr.: 32.549.702 von VeuveClicquot am 24.11.07 18:01:34MACD mit positiver Divergenz und könnte nächste Woche ein Kaufsignal generieren. Stochastic auf Wochenbasis dürfte auch in Kürze nach oben drehen; unabhängig davon sind die Zahlen (in 2 Wochen?) sehr wichtig sowie ein Status Quo zur neuen Mine natürlich:

aus Stockhouse:

SUBJECT: RE: .67 to .67 Posted By: TheRock07

Post Time: 11/25/2007 08:43

Other factors include the recent market swoon which took down all stocks, including gold stocks.

The lack of development news has also been a factor, as no news has been provided since Sept 27.

The next financial report should provide a significant development update, especially re the El Castillo mine which is expected to hit 15,000 oz by exit 2007.

This mine is still in ramp-up, and would appear to be still in the capitalization stage of commissioning , so that its costs and sales will not appear in the top or bottom lines ( I believe that commercialization begins once a mine hits 75 % capacity ).

What will be significant is the leaching capacity achieved,as 100,000 tons is the predicted rate by exit 2007, enroute to 200,000 tons in 2008.

Other issues would be the exploration plans for 2008, including La Fortuna where only a minor exploration costs are required to bring it to 43-101 compliancy. Current plans are to have this completed by Q2/08 , prior to a scoping study.

My understanding for El Sastre is that they wont invest in an early exploration program unless they are convinced that CSG can acquire the remaining 15,000 oz of production.

Then there is the Lone Mountain PM property, and also the updated 43-101 for El Castillo, whose current 43-101 is based on a POG less than half of current levels ......implying that the cut-off grade could be much lower, bringing significant more ore into the 43-101 estimates.

As ppp stated, in the final analyses, it will be what how much gold they have in the ground and how cheap they can get it out and advance cash flows............

SUBJECT: RE: .67 to .67 Posted By: TheRock07

Post Time: 11/25/2007 08:43

Other factors include the recent market swoon which took down all stocks, including gold stocks.

The lack of development news has also been a factor, as no news has been provided since Sept 27.

The next financial report should provide a significant development update, especially re the El Castillo mine which is expected to hit 15,000 oz by exit 2007.

This mine is still in ramp-up, and would appear to be still in the capitalization stage of commissioning , so that its costs and sales will not appear in the top or bottom lines ( I believe that commercialization begins once a mine hits 75 % capacity ).

What will be significant is the leaching capacity achieved,as 100,000 tons is the predicted rate by exit 2007, enroute to 200,000 tons in 2008.

Other issues would be the exploration plans for 2008, including La Fortuna where only a minor exploration costs are required to bring it to 43-101 compliancy. Current plans are to have this completed by Q2/08 , prior to a scoping study.

My understanding for El Sastre is that they wont invest in an early exploration program unless they are convinced that CSG can acquire the remaining 15,000 oz of production.

Then there is the Lone Mountain PM property, and also the updated 43-101 for El Castillo, whose current 43-101 is based on a POG less than half of current levels ......implying that the cut-off grade could be much lower, bringing significant more ore into the 43-101 estimates.

As ppp stated, in the final analyses, it will be what how much gold they have in the ground and how cheap they can get it out and advance cash flows............

Scheint ja ein sehr interessanter Wert zu sein, werde mich mal genauer informieren...

Meint ihr, dass beim Kauf Eile geboten ist oder erstmal abwarten?

Übrigens, wem Castle Gold gefällt, dem könnte vom Business-Modell auch Vane Minerals gefallen (eigener Thread bei w:o), die haben ebenfalls bereits eine produzierende (Gold/Silber) Mine und bizarrst niedrige MK, Schwerpunkt ist eher die Uran-Exploration. Das aber nur am Rande, sorry für die "Eigenwerbung".

Meint ihr, dass beim Kauf Eile geboten ist oder erstmal abwarten?

Übrigens, wem Castle Gold gefällt, dem könnte vom Business-Modell auch Vane Minerals gefallen (eigener Thread bei w:o), die haben ebenfalls bereits eine produzierende (Gold/Silber) Mine und bizarrst niedrige MK, Schwerpunkt ist eher die Uran-Exploration. Das aber nur am Rande, sorry für die "Eigenwerbung".

Antwort auf Beitrag Nr.: 32.580.919 von heddog am 27.11.07 13:25:43nichts für ungut aber Castle Gold hat ZWEI produzierende Minen.

Gold-Silberminen mit Schwerpunkt Uran-Exploration sind ansonsten nicht ganz nach meinem Geschmack.

Gold-Silberminen mit Schwerpunkt Uran-Exploration sind ansonsten nicht ganz nach meinem Geschmack.

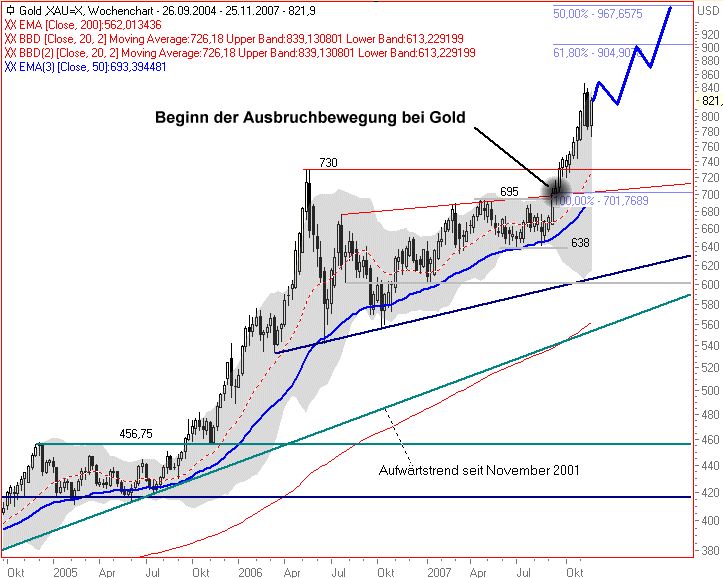

GOLD und SILBER - "Das ist doch erst der Anfang"

Datum

25.11.2007 - Uhrzeit 23:30 (© BörseGo AG 2007, Autor: Weygand Harald, Vorstand BörseGo AG, © GodmodeTrader - http://www.godmode-trader.de/)

WKN: 965515 | ISIN: XC0009655157 | Intradaykurs:

Der US-Dollar in einer brachialen Abwertungsspirale, der Euro gleichzeitig im Aufwertungsmodus, Öl stark steigend und die Edelmetalle stark steigend. So läßt sich die Situation unter den prominenten Vertretern des Währungs- und Rohstoffmarktes kurz zusammenfassen.

Besonders stark ist die gegenläufige Korrelation zwischen US-Dollar und Ölpreis. Immer wenn der US-Dollar fällt, steigt Öl. So plakativ läßt sich die Korrelation beschreiben.

Im Rahmen dieser Weekend Edtion möchte ich ein paar Worte zur charttechnischen Verfassung von Gold und Silber verlieren. Das Interesse an diesen beiden Edelmetallen ist außergewöhnlich groß. Und natürlich stellen sich die Anleger die Frage, ob der Anstieg so weitergehen kann oder nicht.

Gold aktuell 821 $ pro Feinunze.

Silber aktuell 14,69 $ pro Feinunze.

Anbei die Wochencharts (log.) seit September 2004 (1 Kerze = 1 Woche).

Gold

Im September dieses Jahres brach Gold über die charttechnisch entscheidende BUY Triggerzone bei 695 - 700 $ regelkonform nach oben aus. Dadurch wurde der über einjährige Seitwärtskorrekturprozess beendet. Dadurch wurde das nächste große Kaufsignal ausgelöst. Und ich kann die Gold-Bullen beruigen. Der Ausbruch befindet sich erst im ersten Drittel. Die Aufwärtsbewegung dürfte in den kommenden Wochen und Monaten anhalten. Wir erwarten Ziele von 1.000 $ und anschließend 1.230 $. Letzteres ist eine neue Zielmarke. Bei 730 $ hat Gold ab jetzt eine starke Kreuzunterstützung (Support Cluster). Sollte es wider Erwarten nochmals zu einem so starken Rücksetzer kommen, wäre Gold hier ein MUST Trading BUY. Eine weitere zu nennende Unterstützung hat Gold bei 767 $.

Silber

Während Gold bereits im September seine Ausbruchbewegung über das entscheidende BUY Triggerniveau gestartet hat, hinkt Silber dieser Entwicklung noch hinterher, was allerdings typisch ist. Silber springt in der Regel später als Gold an. Erst in den vergangenen Wochen konnte Silber über sein charttechnisch relevantes BUY Triggerniveau bei 14,00 $ ausbrechen. Es gab auch schon recht schnell einen Pullback (Rückkehrbewegung). Maximal bis 14,00 $ sollte diese verlaufen, dann muß der Kurs wieder anspringen! Bisher paßt das soweit. Die Kursziele, die sich aus dem aufgeknackten Rounding Bottom und dem riesigen steigenden Dreieck ergeben, liegen bei 21,50 und 25,00 $ pro Feinunze im mittelfristigen Zeitfenster. Bleiben Sie also dabei. Es lohnt sich.

Datum

25.11.2007 - Uhrzeit 23:30 (© BörseGo AG 2007, Autor: Weygand Harald, Vorstand BörseGo AG, © GodmodeTrader - http://www.godmode-trader.de/)

WKN: 965515 | ISIN: XC0009655157 | Intradaykurs:

Der US-Dollar in einer brachialen Abwertungsspirale, der Euro gleichzeitig im Aufwertungsmodus, Öl stark steigend und die Edelmetalle stark steigend. So läßt sich die Situation unter den prominenten Vertretern des Währungs- und Rohstoffmarktes kurz zusammenfassen.

Besonders stark ist die gegenläufige Korrelation zwischen US-Dollar und Ölpreis. Immer wenn der US-Dollar fällt, steigt Öl. So plakativ läßt sich die Korrelation beschreiben.

Im Rahmen dieser Weekend Edtion möchte ich ein paar Worte zur charttechnischen Verfassung von Gold und Silber verlieren. Das Interesse an diesen beiden Edelmetallen ist außergewöhnlich groß. Und natürlich stellen sich die Anleger die Frage, ob der Anstieg so weitergehen kann oder nicht.

Gold aktuell 821 $ pro Feinunze.

Silber aktuell 14,69 $ pro Feinunze.

Anbei die Wochencharts (log.) seit September 2004 (1 Kerze = 1 Woche).

Gold

Im September dieses Jahres brach Gold über die charttechnisch entscheidende BUY Triggerzone bei 695 - 700 $ regelkonform nach oben aus. Dadurch wurde der über einjährige Seitwärtskorrekturprozess beendet. Dadurch wurde das nächste große Kaufsignal ausgelöst. Und ich kann die Gold-Bullen beruigen. Der Ausbruch befindet sich erst im ersten Drittel. Die Aufwärtsbewegung dürfte in den kommenden Wochen und Monaten anhalten. Wir erwarten Ziele von 1.000 $ und anschließend 1.230 $. Letzteres ist eine neue Zielmarke. Bei 730 $ hat Gold ab jetzt eine starke Kreuzunterstützung (Support Cluster). Sollte es wider Erwarten nochmals zu einem so starken Rücksetzer kommen, wäre Gold hier ein MUST Trading BUY. Eine weitere zu nennende Unterstützung hat Gold bei 767 $.

Silber

Während Gold bereits im September seine Ausbruchbewegung über das entscheidende BUY Triggerniveau gestartet hat, hinkt Silber dieser Entwicklung noch hinterher, was allerdings typisch ist. Silber springt in der Regel später als Gold an. Erst in den vergangenen Wochen konnte Silber über sein charttechnisch relevantes BUY Triggerniveau bei 14,00 $ ausbrechen. Es gab auch schon recht schnell einen Pullback (Rückkehrbewegung). Maximal bis 14,00 $ sollte diese verlaufen, dann muß der Kurs wieder anspringen! Bisher paßt das soweit. Die Kursziele, die sich aus dem aufgeknackten Rounding Bottom und dem riesigen steigenden Dreieck ergeben, liegen bei 21,50 und 25,00 $ pro Feinunze im mittelfristigen Zeitfenster. Bleiben Sie also dabei. Es lohnt sich.

Man hier im Thread ist aber auch sowas von tote Hose.

Moment, ich mach erstmal das Licht an, ah jetzt isses besser.

Moment, ich mach erstmal das Licht an, ah jetzt isses besser.

Antwort auf Beitrag Nr.: 32.601.303 von testlauf am 28.11.07 17:22:55lieber tote Hose und irgendjemand der am Lichtschalter rumspielt als ein wildes Rumgebrülle von "Der letzte macht das Licht aus"

dat wird schon

dat wird schon

haste recht. licht bleibt an!

was ich bisher gelesen habe ist ganz respektierlich. die ganzen labertaschen sind auch noch nicht hier angekommen, das ist auch gut. Rainolaus macht den Informator, auch gut.

Alles prima soweit.

stehen irgendwelche infos an (2 wochen?)

was ich bisher gelesen habe ist ganz respektierlich. die ganzen labertaschen sind auch noch nicht hier angekommen, das ist auch gut. Rainolaus macht den Informator, auch gut.

Alles prima soweit.

stehen irgendwelche infos an (2 wochen?)

Antwort auf Beitrag Nr.: 32.602.010 von testlauf am 28.11.07 17:54:12> ...haste recht. licht bleibt an!

<-- Das sehe ich auch so!

> was ich bisher gelesen habe ist ganz respektierlich. ...

<-- So hatte ich das auch gesehen und deshalb diesen Thread angefangen.

Ich freu mich, dass es hier auch noch einige andere Interessierte für diesen Wert gibt...

Schön, dass es "eine Versorgung mit Basisinformationen" - durch rainolaus - gibt!

Danke.

Dann auf ein fröhliches WEITER so!

[gemeint ist: Thread und Aktie!]

<-- Das sehe ich auch so!

> was ich bisher gelesen habe ist ganz respektierlich. ...

<-- So hatte ich das auch gesehen und deshalb diesen Thread angefangen.

Ich freu mich, dass es hier auch noch einige andere Interessierte für diesen Wert gibt...

Schön, dass es "eine Versorgung mit Basisinformationen" - durch rainolaus - gibt!

Danke.

Dann auf ein fröhliches WEITER so!

[gemeint ist: Thread und Aktie!]

Castle Gold Corp

Onsino Capital Corporation Announces New Director

11/29/2007

TORONTO, Nov. 29, 2007 (Canada NewsWire via COMTEX News Network) --

Onsino Capital Corporation (TSX Venture: OS.P) is pleased to announce that John Paterson has joined the board of directors of Onsino Capital Corporation. Mr. Paterson has a diversity of experience gained with major and junior mining companies. He is a professional engineer and currently serves on the boards of several mining and exploration companies. Most recently he joined the board of Castel Gold Corp. (TSX.V:CSG), which has producing gold mines in Guatemala and Mexico. Mr. Paterson was President and CEO of Aurogin Resources for five years, from 2002 to 2007, which developed the El Sastre gold mine prior to the merger with Morgain Minerals (which formed Castel Gold). Before joining Aurogin, Mr. Paterson was President and CEO of Geomaque Exploration Ltd. from 1991 to 2001, where he directed the development of two heap leach gold mines, the San Francisco gold mine located in Sonora, Mexico and the Vueltas Del Rio gold mine located in Honduras. Mr. Paterson also currently serves on the boards of Plato Gold Corp (TSX.V:PGC), Everton Resources Ltd. (TSX.V:EVR) and Columbia Metals Corporation Limited (TSX.V:COL). Mr. Paterson received his P. Eng. and M. Sc. from Queen's University in Kingston.

The TSX Venture Exchange Inc. has in no way passed upon the merits of the

Onsino Capital Corporation Announces New Director

11/29/2007

TORONTO, Nov. 29, 2007 (Canada NewsWire via COMTEX News Network) --

Onsino Capital Corporation (TSX Venture: OS.P) is pleased to announce that John Paterson has joined the board of directors of Onsino Capital Corporation. Mr. Paterson has a diversity of experience gained with major and junior mining companies. He is a professional engineer and currently serves on the boards of several mining and exploration companies. Most recently he joined the board of Castel Gold Corp. (TSX.V:CSG), which has producing gold mines in Guatemala and Mexico. Mr. Paterson was President and CEO of Aurogin Resources for five years, from 2002 to 2007, which developed the El Sastre gold mine prior to the merger with Morgain Minerals (which formed Castel Gold). Before joining Aurogin, Mr. Paterson was President and CEO of Geomaque Exploration Ltd. from 1991 to 2001, where he directed the development of two heap leach gold mines, the San Francisco gold mine located in Sonora, Mexico and the Vueltas Del Rio gold mine located in Honduras. Mr. Paterson also currently serves on the boards of Plato Gold Corp (TSX.V:PGC), Everton Resources Ltd. (TSX.V:EVR) and Columbia Metals Corporation Limited (TSX.V:COL). Mr. Paterson received his P. Eng. and M. Sc. from Queen's University in Kingston.

The TSX Venture Exchange Inc. has in no way passed upon the merits of the

Antwort auf Beitrag Nr.: 32.618.519 von Rainolaus am 29.11.07 20:12:36grrrr wieder nur sowas...

immer wenn da neben dem Symbol "NEWS" blinkt bin ich ganz aufgeregt und dann sinds nur options oder Personalveränderungen.

ich will, dass ich da draufklicke und mich nur noch die headline

"Castle Gold is proud to announce high productionrates and achievement of MOL productioncosts at El Castillo " anlächelt

finds übrigens nicht so toll, dass Castle mir auf drei mal mailen in 2 Wochen nicht antwortet.

immer wenn da neben dem Symbol "NEWS" blinkt bin ich ganz aufgeregt und dann sinds nur options oder Personalveränderungen.

ich will, dass ich da draufklicke und mich nur noch die headline

"Castle Gold is proud to announce high productionrates and achievement of MOL productioncosts at El Castillo " anlächelt

finds übrigens nicht so toll, dass Castle mir auf drei mal mailen in 2 Wochen nicht antwortet.

Antwort auf Beitrag Nr.: 32.619.068 von Wiewel2005 am 29.11.07 20:38:41> ...finds übrigens nicht so toll, dass Castle mir auf drei mal mailen in 2 Wochen nicht antwortet.

<-- Nicht schön...aber wenn sie deswegen um so emsiger produzieren und einen guten Jahresabschluss "hinlegen"!?!!!?

Wär' mir auch recht.

<-- Nicht schön...aber wenn sie deswegen um so emsiger produzieren und einen guten Jahresabschluss "hinlegen"!?!!!?

Wär' mir auch recht.

Antwort auf Beitrag Nr.: 32.620.266 von james_mg11 am 29.11.07 21:26:19> ...

> Onsino Capital Corporation (TSX Venture: OS.P) is pleased to announce that John Paterson has joined the board of directors of Onsino Capital Corporation. Mr. Paterson has a diversity of experience gained with major and junior mining companies. He is a professional engineer and currently serves on the boards of several mining and exploration companies. Most recently he joined the board of Castle Gold Corp. (TSX.V:CSG), which has producing gold mines in ...

<-- Was bedeutet es, dass Mr. Paterson zuerst das "Board" von Castle Gold und anschließend das board dieser Kapital-Gesellschaft "beglückt"?

Bedeutet es: Es interessiert sich ein (weiterer?) finanzkräftiger "Partner" für Castle Gold oder bedeutet es mehr/weniger?

Wer könnte sich eine mögliche Antwort denken?

> Onsino Capital Corporation (TSX Venture: OS.P) is pleased to announce that John Paterson has joined the board of directors of Onsino Capital Corporation. Mr. Paterson has a diversity of experience gained with major and junior mining companies. He is a professional engineer and currently serves on the boards of several mining and exploration companies. Most recently he joined the board of Castle Gold Corp. (TSX.V:CSG), which has producing gold mines in ...

<-- Was bedeutet es, dass Mr. Paterson zuerst das "Board" von Castle Gold und anschließend das board dieser Kapital-Gesellschaft "beglückt"?

Bedeutet es: Es interessiert sich ein (weiterer?) finanzkräftiger "Partner" für Castle Gold oder bedeutet es mehr/weniger?

Wer könnte sich eine mögliche Antwort denken?

Antwort auf Beitrag Nr.: 32.619.068 von Wiewel2005 am 29.11.07 20:38:41

mangelnde Kommunikation stört mich tendenziell auch immer. Waren denn Deine Fragen sehr direkt nach dem Stand bei Castello ausgerichtet, sodass sie vielleicht nichts dazu sagen dürfen?

mangelnde Kommunikation stört mich tendenziell auch immer. Waren denn Deine Fragen sehr direkt nach dem Stand bei Castello ausgerichtet, sodass sie vielleicht nichts dazu sagen dürfen?

immer wieder fette bids bei 0,64 seit Tagen...

BID Orders Volume Price Range

10 123,500 0.600-0.640

ASK Price Range Volume Orders

0.650-0.690 64,000 10

BID Orders Volume Price Range

10 123,500 0.600-0.640

ASK Price Range Volume Orders

0.650-0.690 64,000 10

Antwort auf Beitrag Nr.: 32.632.760 von Rainolaus am 30.11.07 20:59:17

Werde auch nächste Woche den Verlauf bischen (genauer) ansehen.

Scheint, als ob jemand die Ünterstützungslinie / den Aufwärtstrend stabilisieren möchte, rein charttechnisch betrachtet.

Werde auch nächste Woche den Verlauf bischen (genauer) ansehen.

Scheint, als ob jemand die Ünterstützungslinie / den Aufwärtstrend stabilisieren möchte, rein charttechnisch betrachtet.

Antwort auf Beitrag Nr.: 32.637.125 von VeuveClicquot am 01.12.07 13:04:27gut möglich. Ob sie gestützt wird oder für die meisten hier die Chancen den Risiken überwiegen sei mal dahin gestellt.

Sieht jedenfalls schwer nach bOdenbildung aus. Ich habe nochmal aufgestockt heute.

Die ZAhlen können nicht mehr allzu lange dauern.

Sieht jedenfalls schwer nach bOdenbildung aus. Ich habe nochmal aufgestockt heute.

Die ZAhlen können nicht mehr allzu lange dauern.

wird immer extremer auf der Käuferseite:

BID Orders Volume Price Range

14 202,000 0.580-0.640

ASK Price Range Volume Orders

0.650-0.720 75,500 8

ein Prodzuent mit 2 Minen zu ~45Mio CAD... bin mal gespannt wie das hier weiter geht...

BID Orders Volume Price Range

14 202,000 0.580-0.640

ASK Price Range Volume Orders

0.650-0.720 75,500 8

ein Prodzuent mit 2 Minen zu ~45Mio CAD... bin mal gespannt wie das hier weiter geht...

Zahlen sind raus.

wobei diese natürlich nur bis einschl. September gehen. Spannend wird es natürlich erst ab September.

Ich hoffe auf ein Produktions-Update von Castello heute bzw. diese woche.

wobei diese natürlich nur bis einschl. September gehen. Spannend wird es natürlich erst ab September.

Ich hoffe auf ein Produktions-Update von Castello heute bzw. diese woche.

During the third quarter 2007, the Company sold 400 ounces at $715 per ounce from its El Castillo gold mine in Mexico. The

resulting revenue has been netted against the carrying value of El Castillo in mineral properties. This will continue until the El

Castillo mine reaches commercial production which is expected to be by the end of 2007.

resulting revenue has been netted against the carrying value of El Castillo in mineral properties. This will continue until the El

Castillo mine reaches commercial production which is expected to be by the end of 2007.

Antwort auf Beitrag Nr.: 32.658.564 von Rainolaus am 04.12.07 13:49:49Ja, da gab es schon eine Meldung auf der HP von CSG...

"September 27, 2007

Castle Gold Sells First El Castillo Gold At Us $715 Per Ounce

TORONTO, ON, September 27, 2007 -- Castle Gold Corporation ("Castle Gold" or the "Company") (TSX-V: CSG) announces the first gold sale from its 100% owned El Castillo mine in Durango, Mexico. The Company capitalized on the recent increase in the price of gold by selling 450 ounces at an average realized price of US$715 per ounce. This first sale of El Castillo gold represents production from the first month-and-a-half of pre-production leaching that began in July. Production at El Castillo..."

Heißt:

Am 27. September 2007 hatte CSG schon 450 oz. zu je $715 verkauft, die aus den Erzen der seit Juli laufenden (Vor-) Produktion gewonnen wurden!

Das bedeutet (wenn ich richtig interpretiere), dass

a) das erst einmal "nicht so viel" war, was verkauft wurde,

b) zur "Kapitalisierung"(Kapitalbeschaffung) dieses Gold verkauft wurde,

c) der Weg von der Mine zum "fertigen"/verkaufbaren Gold durchgehend funktioniert

d) die Produktion bis dahin (Sept.) "getestet" wurde,

e) jetzt - nach den vorher ausgegebenen Planzahlen - mit mehr Output zu rechnen ist (schließlich liegen diese Minen in einem klimatisch anderen Gebiet als z. B. D oder US

Da lassen wir uns einmal überraschen...

"September 27, 2007

Castle Gold Sells First El Castillo Gold At Us $715 Per Ounce

TORONTO, ON, September 27, 2007 -- Castle Gold Corporation ("Castle Gold" or the "Company") (TSX-V: CSG) announces the first gold sale from its 100% owned El Castillo mine in Durango, Mexico. The Company capitalized on the recent increase in the price of gold by selling 450 ounces at an average realized price of US$715 per ounce. This first sale of El Castillo gold represents production from the first month-and-a-half of pre-production leaching that began in July. Production at El Castillo..."

Heißt:

Am 27. September 2007 hatte CSG schon 450 oz. zu je $715 verkauft, die aus den Erzen der seit Juli laufenden (Vor-) Produktion gewonnen wurden!

Das bedeutet (wenn ich richtig interpretiere), dass

a) das erst einmal "nicht so viel" war, was verkauft wurde,

b) zur "Kapitalisierung"(Kapitalbeschaffung) dieses Gold verkauft wurde,

c) der Weg von der Mine zum "fertigen"/verkaufbaren Gold durchgehend funktioniert

d) die Produktion bis dahin (Sept.) "getestet" wurde,

e) jetzt - nach den vorher ausgegebenen Planzahlen - mit mehr Output zu rechnen ist (schließlich liegen diese Minen in einem klimatisch anderen Gebiet als z. B. D oder US

Da lassen wir uns einmal überraschen...

Antwort auf Beitrag Nr.: 32.659.510 von james_mg11 am 04.12.07 15:00:07Consolidated Financial and Operating Highlights(b)

Three months ended

September 30, 2007

Nine months ended

September 30, 2007

2007 2006 2007 2006

Gold ounces – produced (c) 3,116 - 8,568 -

Gold ounces – sold (c) 3,251 - 8,053 -

Metal sales (c) $2,318,088 - $5,521,561 -

Cost of sales (a) $621,534 - $1,623,934 -

Accretion, depreciation, depletion

and amortization $266,810 - $682,630 -

Mine operating earnings $1,429,744 - $3,214,997 -

Net (loss) earnings ($200,314) ($113,914) $43,317 ($246,306)

Basic and diluted earnings (loss) per share ($0.01) ($0.00) $0.00 ($0.00)

Cash flow provided by (used in)

operating activities $847,754 $448 $1,779,499 ($28,517)

Average realized gold price per ounce $713 - $686 -

Cost of sales per ounce sold $191 - $202 -

(a) Cost of sales excludes accretion, depreciation, depletion and amortization.

(b) As a result of having to fully consolidate the results from the Company’s 50% owned El Sastre gold mine, the

amounts above represent 100% of the gold ounces produced and sold, metal sales, cost of sales and depreciation,

depletion and amortization.

(c) Does not include sale of 400 ounces at $715 per ounce from the El Castillo mine currently in pre-production

Three months ended

September 30, 2007

Nine months ended

September 30, 2007

2007 2006 2007 2006

Gold ounces – produced (c) 3,116 - 8,568 -

Gold ounces – sold (c) 3,251 - 8,053 -

Metal sales (c) $2,318,088 - $5,521,561 -

Cost of sales (a) $621,534 - $1,623,934 -

Accretion, depreciation, depletion

and amortization $266,810 - $682,630 -

Mine operating earnings $1,429,744 - $3,214,997 -

Net (loss) earnings ($200,314) ($113,914) $43,317 ($246,306)

Basic and diluted earnings (loss) per share ($0.01) ($0.00) $0.00 ($0.00)

Cash flow provided by (used in)

operating activities $847,754 $448 $1,779,499 ($28,517)

Average realized gold price per ounce $713 - $686 -

Cost of sales per ounce sold $191 - $202 -

(a) Cost of sales excludes accretion, depreciation, depletion and amortization.

(b) As a result of having to fully consolidate the results from the Company’s 50% owned El Sastre gold mine, the

amounts above represent 100% of the gold ounces produced and sold, metal sales, cost of sales and depreciation,

depletion and amortization.

(c) Does not include sale of 400 ounces at $715 per ounce from the El Castillo mine currently in pre-production

Antwort auf Beitrag Nr.: 32.659.874 von Rainolaus am 04.12.07 15:23:14Wie auch immer - wir werden uns doch jetzt nicht um 50 Unzen streiten...

CASTLE GOLD CORPORATION

(Formerly Aurogin Resources Ltd.)

Management’s Discussion and Analysis

For the three and nine months ended September 30, 2007

This Management’s Discussion and Analysis (“MD&A”) relates to the financial condition and results of operations

of Castle Gold Corporation (formerly Aurogin Resources Ltd.(“Aurogin”)) (“Castle Gold” or the “Company”)

together with its Guatemalan subsidiary as of November 29, 2007, and is intended to supplement and complement

the Company’s interim consolidated financial statements for the period ended September 30, 2007. Readers are

cautioned that the MD&A contains forward-looking statements and that actual events may vary from management’s

expectations. Readers are encouraged to consult Aurogin’s audited consolidated financial statements and

corresponding notes to the financial statements for the year ended December 31, 2006, for additional details, which

are available on the Company’s website www.castlegoldcorp.com and on www.sedar.com. The interim

consolidated financial statements and MD&A are presented in United States dollars and have been prepared in

accordance with Canadian generally accepted accounting principles (“Canadian GAAP”). This discussion

addresses matters we consider important for an understanding of our financial condition and results of operations

as of and for the three and nine months ended September 30, 2007.

This section contains forward-looking statements and should be read in conjunction with the risk factors described

in “Risk Analysis” and the “Cautionary Statement on Forward-Looking Information” at the end of this MD&A.

1. Description of the Business

Castle Gold is engaged in gold mining and related activities, including acquisition, exploration and

development of gold-bearing mineral properties in the Americas. Castle Gold’s gold production activities

are carried on in Guatemala and Mexico, which is in the process of ramping up to commercial production

levels, while exploration activities are carried out in Mexico, Guatemala, the United States and Canada.

At present, gold is produced in carbon in Guatemala and Mexico, shipped to a custom carbon stripper in

the United States where it is processed into doré and then shipped to a refiner for final processing. The

Company is in the process of installing gold stripping capabilities at each of its two operations.

Consolidated Financial and Operating Highlights(b)

Three months ended

September 30, 2007

Nine months ended

September 30, 2007

2007 2006 2007 2006

Gold ounces – produced (c) 3,116 - 8,568 -

Gold ounces – sold (c) 3,251 - 8,053 -

Metal sales (c) $2,318,088 - $5,521,561 -

Cost of sales (a) $621,534 - $1,623,934 -

Accretion, depreciation, depletion

and amortization $266,810 - $682,630 -

Mine operating earnings $1,429,744 - $3,214,997 -

Net (loss) earnings ($200,314) ($113,914) $43,317 ($246,306)

Basic and diluted earnings (loss) per share ($0.01) ($0.00) $0.00 ($0.00)

Cash flow provided by (used in)

operating activities $847,754 $448 $1,779,499 ($28,517)

Average realized gold price per ounce $713 - $686 -

Cost of sales per ounce sold $191 - $202 -

(a) Cost of sales excludes accretion, depreciation, depletion and amortization.

(b) As a result of having to fully consolidate the results from the Company’s 50% owned El Sastre gold mine, the

amounts above represent 100% of the gold ounces produced and sold, metal sales, cost of sales and depreciation,

depletion and amortization.

(c) Does not include sale of 400 ounces at $715 per ounce from the El Castillo mine currently in pre-production.

The profitability and operating cash flow of the Company is affected by various factors, including the

amount of gold produced and sold, the market price of gold, operating costs, interest rates, regulatory and

environmental compliance, general and administrative costs, the level of exploration and development

expenditures and other discretionary costs. Castle Gold is also exposed to fluctuations in foreign currency

exchange rates that can impact profitability and cash flow. The Company’s assets located outside of

North America are subject to foreign investment risk, including increases in taxes and royalties,

renegotiation of contracts and political uncertainty. While Castle Gold seeks to manage the level of risk

associated with its business, many of the factors affecting these risks are beyond the Company’s control.

2. Impact of Key Economic Trends

Castle Gold’s (formerly Aurogin’s) 2006 annual MD&A contains a discussion of the key economic trends

that affect the Company and its financial statements. Included in this MD&A is an update that reflects

any significant changes since the preparation of the 2006 Annual MD&A.

Price of gold

The price of gold is the largest single factor in determining profitability and cash flow from the

Company’s operation. The average market price of gold during the third quarter 2007 was $680 per

ounce and $666 per ounce for the first nine months of 2007. Prices in the first nine months of 2007

ranged from a low of $608 per ounce to a high of $743 per ounce. These prices compare with an average

of $622 per ounce during the third quarter of 2006 and $601 in the first nine months of 2006. The

Company realized an average price of $713 per ounce on its sales of gold during the third quarter of 2007,

$33 per ounce better than the average for the quarter and $686 per ounce in the nine months of 2007 or

$20 per ounce better than the average for the first nine months of 2007.

Foreign Currencies

Castle Gold receives its revenues through the sale of gold in U.S. dollars. However, the Company has its

operations in Guatemala and Mexico where a portion of the operating costs and capital expenditures are

denominated in the local currency (Guatemalan Quetzal and Mexican Peso respectively) and its head

office in Canada where substantially all of its expenses are denominated in Canadian dollars. In addition,

the Company’s long-term debt, assumed in the acquisition of Morgain Minerals Inc. (“Morgain”), is

denominated in Canadian dollars. Therefore, movements in the exchange rate between these currencies

and the U.S. dollar have an impact on the Company’s profitability and cash flow. Both the Guatemalan

Quetzal and the Mexican Peso remained fairly stable relative to the U.S. dollar during the third quarter

and first nine months of 2007 compared to similar periods in 2006. On the other hand, the Canadian

dollar appreciated 14% during the first nine month of 2007 compared with 4% in 2006 and 6% in the

third quarter of 2007 compared with no change during the third quarter of 2006. This rapid appreciation

of the Canadian dollar relative to the U.S. dollar has had a significant negative impact on the earnings of

the Company during the third quarter of 2007 in U.S. dollars, as a result of a large foreign exchange loss

associated with the translation of the Company’s Canadian dollar denominated long-term debt. The

Company does not currently actively manage foreign currency exposures.

3. Outlook

The Company had stated, as its goals for 2007, to produce 20,000 to 30,000 ounces from the El Sastre

Main Zone Gold Mine, expand the Guatemalan project resource base to greater than one million ounces

of gold mineral resource and complete phase one test drilling at its Lone Mountain property in Nevada,

United States.

During the first quarter of 2007, the Company’s mining rate at the El Sastre gold mine was not yet at full

capacity and the majority of mining activity in January 2007 involved waste removal. This resulted in

lower than planned annualized production. However, in May 2007 the Company exceeded its planned

mining rate of 25,000 tonnes per month to be placed on the leach pad and began crushing parts of the ore

body that had been by-passed during the initial stages of mining. Mining above planned rates during July

and August allowed the Company to achieve its target for third quarter of 2007 despite lower rates in

September due to heavy rains. The Company added 77,000 tonnes of ore to the leach pad during the third

quarter to bring year-to-date totals to 195,000 tonnes placed on the pad having an average grade of

approximately 3.0 grams per tonne gold (“g/t Au”). While the Company expects to place ore containing

between 20,000 and 30,000 ounces on the leach pad during 2007, actual 2007 production and gold sales

will lag slightly behind due to the continuation of the leach cycle into 2008 on ore placed in the latter half

of the fourth quarter and to ultimately achieve an 80% recovery rate on the ore placed during 2007. By

the end of November 2007, gold recovered and fully refined during 2007 was approaching 11,000 ounces

with a full year 2007 target of approximately 15,000 ounces. Cash operating costs per ounce of gold sold

during the quarter average $191 per ounce which continued to reduce operating costs per ounce of gold

sold for the nine months ended September 30, 2007 to $202 per ounce. The mine added $1.4 million in

operating earnings, bringing year-to-date mine operating earnings to $3.2 million.

During the third quarter, the Company released the results of a five hold drill program on its whollyowned

Lone Mountain property in Nevada, United States. While the Company did intersect high grade

lead and zinc values in one hole (4.56 m of 40.1% lead and 4.56 m of 41.3% zinc), discussions are still

ongoing as to the next steps with respect to the Lone Mountain project.

Following the successful August 28, 2007 amalgamation with Morgain to form Castle Gold, the

Company revised its outlook to incorporate the newly acquired assets. The Company continues to set

2008 objectives for its El Sastre mine to produce 25,000 ounces of gold. The Company sold its first gold

from the El Castillo gold mine in Mexico in September 2007. El Castillo is currently ramping up mining

rates to commercial production levels. The Company expects the mine to reach this targeted annualized

mining rate of 15,000 ounces by the end of the year. For 2008, it remains the Company’s objective to

further increase mining rates to an annualized rate of 29,000 ounces by the end of 2008. The Company is

also in the process of updating its technical report on the property which will include and update of the NI

43-101 mineral reserves and resources.

The Company plans to establish a NI 43-101 compliant mineral resource on its La Fortuna property in

Mexico by the end of the second quarter of 2008 by spending approximately $200,000.

During the third quarter of 2007, the Company also negotiated one year extensions in order to meet its

expenditure requirements on the Bridge and Lupita properties in Guatemala. Amounts previously due to

be expended by September 30, 2007 may now be expended by September 30, 2008.

General and administrative expenses during the remainder of 2007 and continuing into 2008, are to rise

following the amalgamation with Morgain.

During the month of October 2007, the Company raised $1.1 million through the early exercise of

1,919,635 warrants otherwise due to expire in April 2008. The Company lowered the exercise price on

these warrants from CDN$0.72 to CDN$0.58 for a limited period of time to facilitate the early exercise.

The Company expects to fund its near-term initiatives through cash flow from its El Sastre gold mine and

from continued warrant exercises.

4. Developments

Amalgamation with Morgain Minerals Inc. (“Morgain”)

On March 5, 2007, Aurogin and Morgain announced that they had entered into a letter of intent to

amalgamate the two companies (the “Amalgamation”). On July 18, 2007, the two companies announced

that they had signed a formal amalgamation agreement. A Joint Information Circular dated July 18, 2007

(the “Circular”) was subsequently mailed to shareholders of both Aurogin and Morgain. On August 17,

2007, the shareholders of Aurogin and Morgain, at respective special meetings of the shareholders,

approved the Amalgamation as described in the Circular by way of special resolution. On August 28,

2007, by Certificate of Amalgamation, Aurogin and Morgain were amalgamated to form Castle Gold

Corporation.

The effective date for completion of the amalgamation was August 28, 2007, proceeding on the following

basis:

1. Shareholders of Aurogin received one (1) common share of Castle Gold for each two (2) Aurogin

shares held; and

2. Shareholders of Morgain received one (1) common share of Castle Gold for each two (2) Morgain

shares held.

In addition, the holders of outstanding options and warrants to acquire common shares of Aurogin and

Morgain are entitled to purchase Castle Gold common shares on the basis of one Castle Gold common

share for every two shares for which the options and warrants to acquire common shares were previously

exercisable at an exercise price per Castle Gold common share equal to twice the previous exercise price.

The term of all outstanding options and warrants to acquire common shares will remain unchanged.

The common shares of Castle Gold began trading, effective at the opening on August 30, 2007, on the

TSX Venture Exchange under the trading symbol “CSG”. Upon the opening, there were 70,195,647

common shares of Castle Gold issued and outstanding. The effect of completing of the amalgamation

was to effect a two for one share consolidation of the previously outstanding shares of Aurogin. As a

result, all comparative share data in this MD&A has been restated to give effect to this share

consolidation.

Castle Gold has accounted for the acquisition of Morgain by Aurogin as the acquisition of an asset using

the purchase method with Aurogin identified as the acquirer and the business acquired recorded at

estimated fair value. The allocation of the purchase price was based on net assets acquired at assigned

values as at August 28, 2007. Severance, in the amount of CDN$120,000, became payable to one director

and officer of Aurogin upon the completion of the amalgamation. CDN$20,000 was paid on October 1,

2007 with the remaining CDN$100,000 payable in instalments of $10,000 a month commencing

November 1, 2007. CDN$90,000 currently remains outstanding under this agreement.

El Sastre Exploitation Licence, Guatemala

The Company is presently preparing a 2008 exploration program for the El Sastre Exploitation License in

Guatemala. The program will address recommendations from the independent technical report titled

“March 2007 Update Report, El Sastre Exploitation Licence, Guatemala” dated March 30, 2007 (the

“Report”) which was announced on May 9, 2007. Exploration will include both drilling and trenching

and will be funded from cash flow from mining operations. In addition, an end-of-year reconciliation is

presently underway in order to compare the extracted mineral quantities and grades from the 2007 mining

operations with the totals contained in the reserve model included in the March 2007 technical report.

El Castillo Project, Mexico

The Company initiated “pre-production” mining operations at the Castillo project in July 2007. Limited

leaching was performed on ore removed during waste stripping operations by utilizing the existing test

leach facilities that were present at the site. Construction of the new leach pad area was completed in

September 2007. Work continues on installing new processing facilities which are expected to be

completed prior to the end of 2007.

The first gold sale from the “pre-production” leaching activities at Castillo was completed on September

27, 2007. The initial gold production rate of 15,000 ounces per year is scheduled to be achieved during

the last quarter of 2007. Gold production will be ramped up during 2008 to an annualized rate of 29,000

ounces.

The El Castillo Project is fully permitted for construction and operation.

La Fortuna Gold Project, Mexico

In May 15, 2007 an Independent Technical Report for the La Fortuna Gold Project (“La Fortuna) in

Mexico was prepared by Toren K. Olson, P.Geol., the independent Qualified Person, to the standard of

the National Instrument 43-101 (NI 43-101). This report contained a number of recommendations

including updating the existing site survey information and drilling 750 meters of “twin” holes to confirm

the existing drill information summarized in the Technical Report.

The Company has initiated a follow-up program for the La Fortuna deposit based on the

recommendations contained in the May 15, 2007 Technical Report. Plans are in place to re-open the

existing site roads following the termination of the rainy season and to complete the updated site survey

and recommended drilling program. This work is scheduled for last quarter 2007 with a full review of the

new drill data in the first quarter of 2008.

On August 13, 2007, Morgain signed an agreement to purchase an additional 8 mineral concessions

totaling 9,851 hectares and surface rights covering 20 hectares that surround and adjoin the Company’s

existing La Fortuna concessions. The agreement called for the issue of 1,000,000 shares of Morgain

(completed pre-amalgamation) and requires payments totaling $300,000. $50,000 was paid prior to the

amalgamation with the remaining three installments totaling $250,000, due over a period ending June 27,

2009.

Bridge Deposit, Guatemala

The Company is presently preparing a detailed exploration plan for the Bridge deposit in Guatemala as

part of its ongoing expenditure commitments. In addition to completing drilling, intended to expand the

areas of known mineralization, a program of soil/sediment sampling will be initiated in presently

unexplored areas of the concession. It is anticipated that the new work program will begin in first quarter

of 2008 following the end of the rainy season in Guatemala. Expenditures will be funded from cash flow

from the Company’s Guatemalan operations. In preparing for the larger exploration program, four

advance holes (total 220m) were completed at the Bridge property in September 2007 in order to test new

drilling equipment. Management is currently reviewing the data from these holes and the results will be

announced as soon as all of the data is available.

Lupita Deposit, Guatemala

The Company is presently preparing a detailed exploration plan for the Lupita deposit in Guatemala as

part of its ongoing expenditure commitments. In addition to drilling intended to expand the areas of

known mineralization a program will also be initiated in presently unexplored areas of the concession. It

is planned that the new work program will begin in Q2 of 2008 following the completion of new access

roads into the property in Q1 of 2008. Ongoing metallurgical work continues on samples of Lupita ore

from previous drill programs.

Lone Mountain drilling

Assay results from a five hole drilling program at the Company’s Lone Mountain property were

announced on July 25, 2007 and July 31, 2007 and included zinc mineralization of 41.3% over a 4.56

metre interval and 40.1% lead over another 4.56 metre interval. Management is continuing to evaluate its

alternatives with respect to Lone Mountain. No additional exploration was completed in the third quarter

of 2007.

5. Consolidated Results of Operations

Operating Highlights(b) Three months ended

September 30,

Nine months ended

September 30,

2007 2006 2007 2006

Gold ounces – produced 3,116 - 8,568 -

Gold ounces – sold 3,251 - 8,053 -

Metal sales $2,318,088 - $5,521,561 -

Cost of sales (a) $621,534 - $1,623,934 -

Depreciation, depletion and amortization $264,446 - $675,536 -

Accretion $2,364 $7,094

Mine operating earnings $1,429,744 - $3,214,997 -

Net earnings (loss) ($200,314) ($113,914) $43,317 ($246,306)

(a) Cost of sales excludes accretion, depreciation, depletion and amortization.

(b) As a result of having to fully consolidate the results from the Company’s 50% owned El Sastre gold mine, the amounts above

represent 100% of the gold ounces produced and sold, metal sales, cost of sales and depreciation, depletion and amortization.

(c) During the third quarter 2007, the Company sold 400 ounces at $715 per ounce from its El Castillo gold mine in Mexico. The

resulting revenue has been netted against the carrying value of El Castillo in mineral properties. This will continue until the El

Castillo mine reaches commercial production which is expected to be by the end of 2007.

Third quarter 2007 vs. third quarter 2006

?? During the third quarter of 2007, the El Sastre Main Zone gold mine produced 3,116 ounces of

gold. There was no production for the comparative period as commercial production did not

commence until December 2006.

?? Gold sales during the third quarter of 2007 were 3,251 ounces at an average gold price of $713

per ounce for metal sales revenue of $2,318,088 compared with no metal sales revenue for the

third quarter of 2006.

?? Mine operating earnings were $1,429,744 for the third quarter of 2007. After deducting general

and administrative, exploration and income tax expenses, removing the 50% of mine operating

earnings attributable to the non-controlling interest and recording an unrealized foreign exchange

loss of $446,572 on the Company’s Canadian dollar denominated long-term debt, the Company

had a net loss for the third quarter of 2007 of $200,314. This compares to a net loss of $113,314

for the third quarter of 2006.

?? Cost of sales of $621,534 represented cash operating costs at the El Sastre Main Zone gold mine

for the third quarter of 2007 or $191 per ounce of gold sold with no amount for the comparative

period.

?? Depreciation, depletion and amortization of $264,446 resulted primarily from property, plant and

equipment associated with the El Sastre Main Zone gold mine compared with no amount for the

comparative period. The majority of the depreciation expense is calculated on a unit-ofproduction

basis.

?? General and administrative costs were $271,936 for the quarter ended September 30, 2007

compared to $117,291 during the quarter ended September 30, 2006. The increase related

primarily to personnel, travel and general office costs, much of which were capitalized during the

construction of the El Sastre Main Zone gold mine in 2006 but are now expensed as well as an

increased accrual for audit fees. This increase was partially offset by significantly lower stock

based compensation expense during the quarter ended September 30, 2007 compared to the

quarter ended September 30, 2006. 2006 saw more stock option grants associated with new

employees or consultants.

?? Exploration costs of $186,345 for the third quarter of 2007 compared to none during the

comparative period, were primarily the result of exploration drilling and related work performed

on the El Arenal Zone on the El Sastre Exploitation licence in Guatemala.

?? Income tax expense of $115,904 related to income tax paid or payable in Guatemala at a rate of

5% of metal sales revenue compared to none for the comparative period.

?? Non-controlling interest of $559,865 represents the share of net earnings from the El Sastre Main

Zone gold mine attributable to the 50% interest not owned by Castle Gold compared to no

amount for the comparative period.

First nine months 2007 vs. first nine months 2006

?? During the first nine months of 2007, the El Sastre Main Zone gold mine produced 8,568 ounces

of gold. There was no production for the comparative period as commercial production did not

commence until December 2006.

?? Gold sales during the first nine months of 2007 were 8,053 ounces at an average gold price of

$686 per ounce for metal sales revenue of $5,521,561 compared with no metal sales revenue for

the first nine months of 2006.

?? Mine operating earnings were $3,214,997 for the first nine months of 2007. After deducting

general and administrative, exploration and income tax expenses, removing the 50% of mine

operating earnings attributable to the non-controlling interest and recording an unrealized foreign

exchange loss of $446,572 on the Company’s Canadian dollar denominated long-term debt, the

Company had net earnings for the first nine months of 2007 of $43,317. This compares to a net

loss of $246,306 for the first nine months of 2006.

?? Cost of sales of $1,623,934 represented cash operating costs at the El Sastre Main Zone gold

mine for the first nine months of 2007 or $202 per ounce of gold sold with no amount for the

comparative period.

?? Depreciation, depletion and amortization of $675,536 resulted primarily from property, plant and

equipment associated with the El Sastre Main Zone gold mine compared with no amount for the

comparative period. The majority of the depreciation expense is calculated on a unit-ofproduction

basis.

?? General and administrative costs were $739,029 for the nine months ended September 30, 2007

compared to $273,214 during the first nine months ended September 30, 2006. The increase

related primarily to personnel, travel and general office costs, much of which were capitalized

during the construction of the El Sastre Main Zone gold mine in 2006 but are now expensed as

well as an increased accrual for audit fees. This increase was partially offset by lower stock

based compensation expense during the nine months ended September 30, 2007 compared to the

nine months ended September 30, 2006. 2006 saw more stock option grants associated with new

employees or consultants.

?? Exploration costs of $316,746 for the first nine months of 2007 compared to a recovery of

$15,720 during the comparative period were primarily the result of exploration drilling and

related work performed at El Arenal and elsewhere on the El Sastre property in Guatemala and

work performed in producing the technical reports on the Guatemalan properties filed during the

second quarter of 2007.

?? Income tax expense of $276,078 related to income tax paid or payable in Guatemala at a rate of

5% of metal sales revenue compared to none for the comparative period.

?? Non-controlling interest of $1,318,178 represents the share of net earnings from the El Sastre

Main Zone gold mine attributable to the 50% interest not owned by Castle Gold compared to no

amount for the comparative period.

Results of Mining Operations

El Sastre Main Zone gold mine (50% ownership)

Amounts presented in the table below are at 100%

Three months ended

September 30,

Nine months ended

September 30,

2007 2006 2007 2006

Operating Statistics

Tonnes mined

Waste

Ore – direct to leach pad

Ore – crushed and placed

Tonnes ore place on leach pad

Grade (grams/tonne)

Gold ounces – produced

Gold ounces – sold

226,725

149,812

57,554

19,359

76,913

2.74

3,116

3,251

-

-

-

-

-

-

-

-

619,856

424,426

160,758

34,672

195,430

2.96

8,568

8,053

-

-

-

-

-

-

-

-

Financial Data

Metal sales

Cost of sales

Depreciation, depletion and amortization

Accretion

Exploration

Other expense

Earnings before income taxes

Income taxes

Net segment earnings

Capital expenditures

$ 2,318,088

621,534

245,878

2,364

1,448,312

163,083

(2,786)

1,288,015

115,904

$ 1,172,111

$ 225,744

$ -

-

-

-____

-

-

-____

-

-____

$ -____

$ -____

$ 5,521,561

1,623,934

652,456

7,094

3,238,077

251,980

(4,937)

2,991,034

276,078

$ 2,714,956

$ 443,057

$ -

-

-

-____

-

-

-____

-

-____

$ -____

$ -____

Three months ended September 30, 2007

The Company mined 226,725 tonnes during the three months ended September 30, 2007 of which 76,913

tonnes of ore, having an average grade of 2.74 g/t Au were placed on the leach pad. This was comprised

of 57,554 tonnes of run of mine ore grading 3.06 g/t Au and 19,359 tonnes or ore requiring crushing

grading 1.77 g/t Au.

Production for the quarter ended September 30, 2007 was 3,116 ounces. Production increased over the

second quarter of 2007 with the normal resumption of carbon processing after delays experienced in

returning carbon to the mine from the United States were resolved.

Gold sales for the quarter ended September 30, 2007 were 3,251 ounces at an average realized price of

$713 per ounce for gross proceeds of $2,318,088. This compares with the average market price during

the third quarter of 2007 of $680 per ounce.

Operating costs for the quarter ended September 30, 2007 were $621,534 or $191 per ounce of gold sold.

This remained relatively consistent with the cost per ounce of gold sold in the second quarter of 2007. On

a per ounce basis, these costs remain in line with management’s initial estimates outlined in the technical

report on the mine.

Exploration costs for the quarter ended September 30, 2007 were $163,083. These were primarily the

result of exploration drilling and related work performed at El Arenal.

Income taxes for the quarter ended September 30, 2007 were $115,904 representing 5% of gold sales for

the quarter.

Capital expenditures during the third quarter of 2007 were $225,744. Of this amount, approximately

$128,000 was for the construction of the next leach pad with another $78,000 spent towards the

construction of a gold stripping plant at the mine site. The Company expects to spend approximately

$125,000 in total on the construction of the strip plant of which $102,000 has been spent to date. This

will facilitate the production of doré at the mine site which will eliminate the process of shipping carbon

to the United States for stripping.

Nine months ended September 30, 2007

The Company mined 619,856 tonnes during the nine months ended September 30, 2007 of which 195,430

tonnes of ore, having an average grade of 2.96 g/t Au were placed on the leach pad. This represents a

65% utilization of the 300,000 tonne capacity leach pad. The ore placed was comprised of 160,758

tonnes of run of mine ore grading 3.27 g/t Au and 34,672 tonnes or ore requiring crushing grading 1.53

g/t Au. During January 2007, the mine concentrated on waste removal with only 2,574 tonnes of ore

placed on the leach pad. February and March 2007 averaged approximately 17,000 tonnes of ore placed

on the leach pad which represented 68% of target mining levels of 25,000 tonnes per month. In May

2007, the mine exceeded these target mining levels by placing in excess of 27,000 tonnes of ore on the

leach pad excluding additional crushed ore. Mining rates continued at or above target during July and

August, while September rates dropped to approximately 13,700 tonnes due to heavy rains. At current

mining and crushing rates, remaining capacity on the initial leach pad will be utilized by approximately

the end of February 2008. The mine has begun preparation for construction of the next leach pad.

Production for the nine months ended September 30, 2007 was 8,568 ounces. This represents gold

ounces recovered in carbon and shipped to the United States for stripping and final refining. In addition

to this, the Company estimates there to be an additional 7,379 recoverable ounces of gold in solution or

on the leach pad applying a recovery rate of 80% to ore placed on the leach pad. The Company expects to

recover a majority of these ounces over the next two quarters.

Gold sales for the nine months ended September 30, 2007 were 8,053 ounces at an average realized price

of $686 per ounce for gross proceeds of $5,521,561. This compares with the average market price during

the first nine months of 2007 of $666 per ounce.

Operating costs for the nine months ended September 30, 2007 were $1,623,934 or $202 per ounce of

gold sold. The year to date improvement in costs on a per ounce basis is attributable to cost reductions

made in respect of shipping carbon to the United States during the second quarter and the result of

increased mining rates during the second and third quarters.

Exploration costs for the nine months ended September 30, 2007 were $251,980. These were primarily

the result of exploration drilling and related work performed at El Arenal. It is estimated that

approximately $300,000 will be spent on exploration drilling during 2007 to test additional targets on the

El Sastre exploitation license.

Income taxes for the nine months ended September 30, 2007 were $276,078 representing 5% of gold sales

for the nine month period.

Capital expenditures during the first nine months of 2007 were $443,057. Of this amount, approximately

$117,000 was spent completing construction of the 300,000 tonne leach pad in the first quarter. Second

quarter expenditures included approximately $27,000 for the purchase of surface rights at El Arenal.

Year-to-date expenditures on construction of the second leach pad are approximately $129,000 while

another approximately $102,000 has been spent towards the construction of a gold stripping plant at the

mine site. The Company expects to spend approximately $125,000 during the year on the construction of

the stripping plant. This will facilitate the production of doré at the mine site which will eliminate the

process of shipping carbon to the United States for stripping. The Company expects to fund all capital

expenditures from cash flow from operations.

6. Mineral Properties

Mineral properties refer to those properties acquired through an option agreement that requires the

Company to make certain property acquisition option payments over a period of time and meet certain

minimum expenditure thresholds over a period of time. These expenditures are capitalized as they are

regarded as costs to acquire the mineral properties in question. Mineral property expenditures for the

quarter ended three and nine months ended September 30, 2007 were $254,775 and $624,772,

respectively. These expenditures include first and third quarter cash option payments totalling $120,000

and $160,000, respectively, for Bridge and Lupita and $34,163 being the fair value attributed to share

purchase warrants issued as an option payment on Lone Mountain. Additionally, $143,441 was spent on

Lone Mountain, principally on a five-hole drill program completed in the second quarter. Expenditures

also included metallurgical testwork relating to Lupita and road construction and drilling at Bridge. Each

property is discussed in greater detail below.

Bridge Zone, Guatemala

On September 9, 2005, the Company entered into an agreement with its partners on the El Sastre project,

to earn a majority interest in the Bridge property located four kilometres west of the El Sastre Main Zone

gold mine. To earn a 51%, the Company agreed to spend $500,000 on exploration by September 30,

2007. In addition, the Company agreed to pay the vendors a total of $240,000 ($15,000 after signing

(paid), $25,000 - March 31, 2006 (paid), $40,000 - September 30, 2006 (paid), $60,000 - March 31, 2007

(paid) and $100,000 - September 30, 2007(paid). The Company also agreed to issue 100,000 common

shares (50,000 shares of Castle Gold) by December 31, 2005 (issued – valued at $8,969), 100,000

common shares (50,000 shares of Castle Gold) by December 31, 2006 (issued – valued at $64,890) and

50,000 common shares of Castle Gold by December 31, 2007. The value of the shares issued in respect

of property option payments was determined using the quoted market value of the Company’s shares at

the time of issue. The Company can earn an additional 14% by completing a feasibility study by

December 31, 2009 and a further 5% by putting the project into production by December 31, 2011.

The Bridge deposit is comprised of hot-spring related gold mineralization and is hosted in a number of

different rock types. A NI 43-101 Technical Report on the Bridge property, dated April 2, 2007, has

estimated an inferred mineral resource of 1.26 million tonnes grading 1.71 g/t Au for 69,700 ounces of

contained gold. The Bridge deposit is a flat-lying lens oriented WNW-ESE. The deposit is

approximately 600 metres long and up to 200 metres wide. Mineralization is up to 19 metres thick and

averages approximately 9 metres within the existing resource.

As at September 30, 2007, Castle Gold had spent approximately $301,000 of the $500,000 required to be