Portfoliotheorie (portfolio theory) (Seite 10)

eröffnet am 10.04.23 20:50:00 von

neuester Beitrag 09.02.24 00:10:12 von

neuester Beitrag 09.02.24 00:10:12 von

Beiträge: 95

ID: 1.368.155

ID: 1.368.155

Aufrufe heute: 1

Gesamt: 2.589

Gesamt: 2.589

Aktive User: 0

Top-Diskussionen

| Titel | letzter Beitrag | Aufrufe |

|---|---|---|

| gestern 18:41 | 191 | |

| 22.06.20, 20:50 | 148 | |

| heute 00:26 | 142 | |

| gestern 23:55 | 125 | |

| gestern 22:49 | 86 | |

| 04.02.24, 15:01 | 74 | |

| vor 1 Stunde | 70 | |

| gestern 23:37 | 64 |

Meistdiskutierte Wertpapiere

| Platz | vorher | Wertpapier | Kurs | Perf. % | Anzahl | ||

|---|---|---|---|---|---|---|---|

| 1. | 1. | 18.002,02 | -1,44 | 264 | |||

| 2. | 2. | 26,58 | -0,63 | 137 | |||

| 3. | 3. | 178,01 | -2,44 | 77 | |||

| 4. | Neu! | 479,00 | -5,71 | 69 | |||

| 5. | 6. | 0,1855 | -1,85 | 67 | |||

| 6. | 15. | 17,550 | -4,10 | 63 | |||

| 7. | 5. | 131,88 | +1,75 | 48 | |||

| 8. | 18. | 5,2900 | -1,89 | 43 |

Beitrag zu dieser Diskussion schreiben

Hallo FC

schön, dass es bei dir weder um Markowitz noch Buffett geht.

Was ist der Sinn und Zweck von diesem Thread - suchst du die Diskussion von Papers die ausserhalb der Community unbekannt sind?

schön, dass es bei dir weder um Markowitz noch Buffett geht.

Was ist der Sinn und Zweck von diesem Thread - suchst du die Diskussion von Papers die ausserhalb der Community unbekannt sind?

Antwort auf Beitrag Nr.: 73.645.313 von faultcode am 10.04.23 21:10:02Linkage:

aus oben: 2011, Jochen Papenbrock:

aus oben: 2011, Jochen Papenbrock:

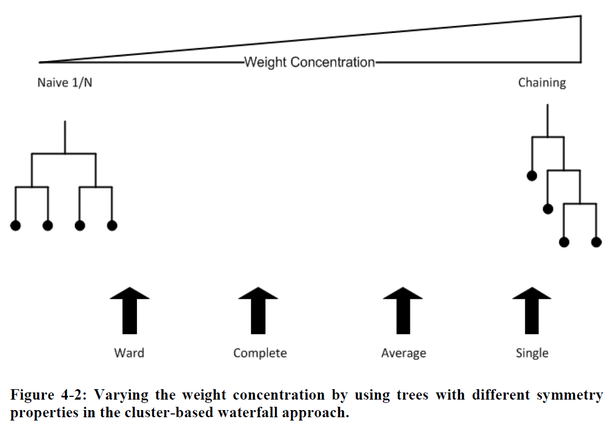

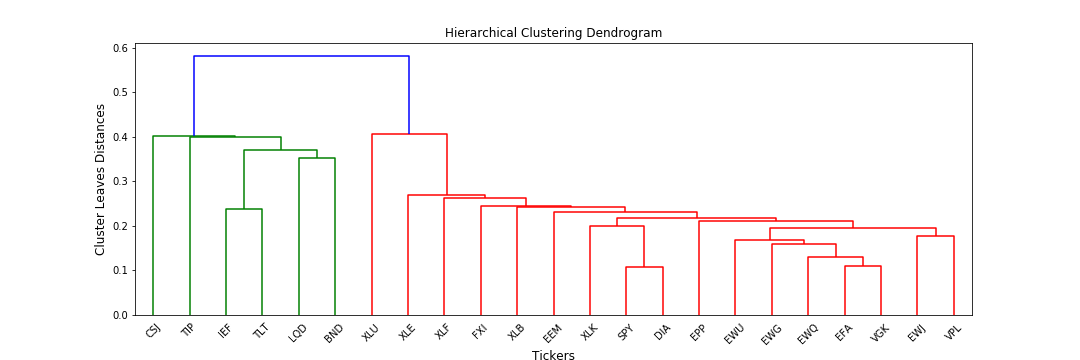

Antwort auf Beitrag Nr.: 73.645.307 von faultcode am 10.04.23 21:07:12Dendrogram = Hierarchical clustering:

aus:

Beyond Risk Parity: The Hierarchical Equal Risk Contribution Algorithm

https://hudsonthames.org/beyond-risk-parity-the-hierarchical…

aus:

Beyond Risk Parity: The Hierarchical Equal Risk Contribution Algorithm

https://hudsonthames.org/beyond-risk-parity-the-hierarchical…

Multilevel Risk Optimization

weg von Quadratic optimizers und Markowitz’s CLA (critical line algorithm) --> Multilevel Risk Optimizationwie oft: Deutschland hat's erfunden, die anderen machen das Geschäft: 2011, PhD thesis by Jochen Papenbrock: Asset Clusters and Asset Networks in Financial Risk Management and Portfolio Optimization --> PDF: https://publikationen.bibliothek.kit.edu/1000025469

Marcos López de Prado, 2016: Building Diversified Portfolios that Outperform Out of Sample --> PDF: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2708678

HRP = Hierarchical Risk Parity

1. Tree Clustering: Group similar investments into clusters, based on a proper distance metric

2. Quasi-diagonalization: Reorganize the rows and columns of the covariance matrix, so that the largest values lie along the diagonal

3. Recursive bisection: Split allocations through recursive bisection of the reordered covariance matrix

Thomas Raffinot, 2017: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2840729 --> PDF: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2840729

HCAA = Hierarchical Clustering based Asset Allocation

1. Hierarchical tree clustering

2. Selecting optimal number of clusters

3. Allocation of capital across clusters

4. Allocation of capital within clusters

HRP + HCAA =>

Thomas Raffinot, 2018: The Hierarchical Equal Risk Contribution Portfolio --> https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3237540

HERC = Hierarchical Equal Risk Contribution:

1. Hierarchical tree clustering

2. Selecting optimal number of clusters

3. Top-down recursive bisection

4. Naive risk parity within the clusters