Biotech Depot - verschiede Werte und Strategien - 500 Beiträge pro Seite

eröffnet am 06.04.12 20:55:15 von

neuester Beitrag 15.12.21 20:44:42 von

neuester Beitrag 15.12.21 20:44:42 von

Beiträge: 2.765

ID: 1.173.523

ID: 1.173.523

Aufrufe heute: 0

Gesamt: 306.557

Gesamt: 306.557

Aktive User: 0

Top-Diskussionen

| Titel | letzter Beitrag | Aufrufe |

|---|---|---|

| 20.04.24, 12:11 | 328 | |

| vor 1 Stunde | 178 | |

| gestern 18:31 | 111 | |

| 22.06.20, 20:50 | 86 | |

| gestern 15:11 | 70 | |

| vor 1 Stunde | 61 | |

| vor 1 Stunde | 49 | |

| gestern 11:20 | 46 |

Meistdiskutierte Wertpapiere

| Platz | vorher | Wertpapier | Kurs | Perf. % | Anzahl | ||

|---|---|---|---|---|---|---|---|

| 1. | 1. | 18.161,01 | +1,36 | 217 | |||

| 2. | 3. | 0,1885 | -0,26 | 90 | |||

| 3. | 2. | 1,1800 | -14,49 | 77 | |||

| 4. | 5. | 9,3500 | +1,14 | 60 | |||

| 5. | 4. | 168,29 | -1,11 | 50 | |||

| 6. | Neu! | 0,4400 | +3,53 | 36 | |||

| 7. | Neu! | 4,7950 | +6,91 | 34 | |||

| 8. | Neu! | 11,905 | +14,97 | 31 |

Im Spätherbst letzten Jahres habe ich angefangen mein Depot vollständig mit Biotech-Aktien auszustatten. Jedem Fond-Manager würde es vermutlich nächtens den Schlaf rauben, hätte er auch nur einen geringen Teil seines ihm zur Verfügung stehenden Anlagevolumens so investiert…aber jeder ist ja selbst seines Erfolges Schmied – oder Knecht – wie es immer schon so schön hieß…

Sowohl das Zinsniveau welches auf Einlagen gezahlt wird, als auch die Performance die mit DAX- und anderen Standardwerten - selbst bei guter Entwicklung erzielbar erschien konnten mich nicht aus der Reserve locken in selbige zu investieren. Ich habe mich daher für die sicherlich risikoreiche Variante des Biotechinvestments entschieden – wenngleich mir bewußt ist, daß gerade in diesem Bereich zeitaufwändige Recherche, sowie sorgfältiges Abwägen der Pro und Contras unerläßlich sind…vermutlich auch immer bleiben werden.

Klar ist eines – selbst die Profis, die mit absoluten Brancheninsidern auf „du und du“ sind – also über beste Infoquellen verfügen - stranden manchmal fürchterlich mit ihrer Anlageentscheidung. Biotech ist und bleibt extrem risikoreich – aber nirgendwo dürften ähnliche Renditen zu erzielen sein wie eben genau in dieser Branche…und das entschädigt auch bei gelegentlich mal sich als falsch herausstellenden Spekulationen.

In diesem Sinne…

Anbei mal was sich neben ein paar kleineren Beigaben derzeit in meinem Depot befindet:

DVAX – Dynavax Technologies

ACAD – Acadia Pharmaceuticals

GTXI – GTX Inc.

HZNP – Horizon Pharmaceuticals

Ich investiere nicht in OTC-Werte - zu hoch ist das Risiko hier bei nur teilweise sehr dünnen Umsätzen ohne gröbere Verluste rauszukommen wenn man raus muß. Meine verfolgte Strategie ist eine andere...

Leider findet sich auf w:o außer zu DVAX kaum mehr ein aktueller Thread der noch gepflegt wird.

Ehemalige Threads zu ACAD und GTXI scheinen in der Versenkung zu ruhen – was absolut unverständlich erscheint , da beiden Unternehmen noch dieses Jahr der „große Wurf“ gelingen könnte. HZNP dürfte hierzulande kaum bekannt sein, weil die Aktie an keiner deutschen Börse handelbar ist. DVAX wird wohl in den kommenden Wochen die bisher in den letzten Monaten erzielte Performance noch massiv ausbauen – hier rücken mehrere Kurstreiber wie Zulassungsanträge für den europäischen, sowie für den amerikanischen Markt immer näher, treffen zudem auf Übernahmespekulationen – und das bei gut 17 Mio. geshorteten Anteilen – das nenne ich wahrhaft explosives Potenzial.

Nicht jede Spekulation auf eine Zulassung durch die FDA ging in den vergangenen Wochen wirklich auf. Das haben zuletzt Unternehmen wie AEZS, KERX und CHTP – vor allem aber deren Aktionäre deutlich zu spüren bekommen. Selbst DSCO, die zumindest eine Zulassung erhielten - wenngleich auch für ein Produkt, welches kaum jemals nennenswerte Umsätze erzielen wird. Auch hier haben die erwarteten Kursgewinne gefloppt.

…habe es mir aber verkniffen dort investiert zu sein – da gab es in meinen Augen bessere Optionen.

Ich würde mich freuen wenn der gemischte Thread Resonanz findet und der eine oder andere was beizusteuern hat. Zu den von mir angesprochen Werten beabsichtige ich noch nähere Infos einzustellen, eine Art Watchlist zu führen, ein paar charttechnische Begebenheiten bei Besonderheiten einzustreuen - Meinungen, Wissenswertes oder Anregungen dazu von euch – immer her damit.

Sowohl das Zinsniveau welches auf Einlagen gezahlt wird, als auch die Performance die mit DAX- und anderen Standardwerten - selbst bei guter Entwicklung erzielbar erschien konnten mich nicht aus der Reserve locken in selbige zu investieren. Ich habe mich daher für die sicherlich risikoreiche Variante des Biotechinvestments entschieden – wenngleich mir bewußt ist, daß gerade in diesem Bereich zeitaufwändige Recherche, sowie sorgfältiges Abwägen der Pro und Contras unerläßlich sind…vermutlich auch immer bleiben werden.

Klar ist eines – selbst die Profis, die mit absoluten Brancheninsidern auf „du und du“ sind – also über beste Infoquellen verfügen - stranden manchmal fürchterlich mit ihrer Anlageentscheidung. Biotech ist und bleibt extrem risikoreich – aber nirgendwo dürften ähnliche Renditen zu erzielen sein wie eben genau in dieser Branche…und das entschädigt auch bei gelegentlich mal sich als falsch herausstellenden Spekulationen.

In diesem Sinne…

Anbei mal was sich neben ein paar kleineren Beigaben derzeit in meinem Depot befindet:

DVAX – Dynavax Technologies

ACAD – Acadia Pharmaceuticals

GTXI – GTX Inc.

HZNP – Horizon Pharmaceuticals

Ich investiere nicht in OTC-Werte - zu hoch ist das Risiko hier bei nur teilweise sehr dünnen Umsätzen ohne gröbere Verluste rauszukommen wenn man raus muß. Meine verfolgte Strategie ist eine andere...

Leider findet sich auf w:o außer zu DVAX kaum mehr ein aktueller Thread der noch gepflegt wird.

Ehemalige Threads zu ACAD und GTXI scheinen in der Versenkung zu ruhen – was absolut unverständlich erscheint , da beiden Unternehmen noch dieses Jahr der „große Wurf“ gelingen könnte. HZNP dürfte hierzulande kaum bekannt sein, weil die Aktie an keiner deutschen Börse handelbar ist. DVAX wird wohl in den kommenden Wochen die bisher in den letzten Monaten erzielte Performance noch massiv ausbauen – hier rücken mehrere Kurstreiber wie Zulassungsanträge für den europäischen, sowie für den amerikanischen Markt immer näher, treffen zudem auf Übernahmespekulationen – und das bei gut 17 Mio. geshorteten Anteilen – das nenne ich wahrhaft explosives Potenzial.

Nicht jede Spekulation auf eine Zulassung durch die FDA ging in den vergangenen Wochen wirklich auf. Das haben zuletzt Unternehmen wie AEZS, KERX und CHTP – vor allem aber deren Aktionäre deutlich zu spüren bekommen. Selbst DSCO, die zumindest eine Zulassung erhielten - wenngleich auch für ein Produkt, welches kaum jemals nennenswerte Umsätze erzielen wird. Auch hier haben die erwarteten Kursgewinne gefloppt.

…habe es mir aber verkniffen dort investiert zu sein – da gab es in meinen Augen bessere Optionen.

Ich würde mich freuen wenn der gemischte Thread Resonanz findet und der eine oder andere was beizusteuern hat. Zu den von mir angesprochen Werten beabsichtige ich noch nähere Infos einzustellen, eine Art Watchlist zu führen, ein paar charttechnische Begebenheiten bei Besonderheiten einzustreuen - Meinungen, Wissenswertes oder Anregungen dazu von euch – immer her damit.

Man merkt, das Du Dich mit der Materie auseinandergesetzt hast.

Von den 4 erwähnten Werten hab ich auch 2 auf der Watchlist.

Allerdings unter ca. 40 anderen.

Warum Du grad diese 4 gewählt hast, wirst Du uns sicher auch noch wissen lassen.

Was DSCO anbetrifft bin ich nicht ganz Deiner Meinung.

Ich vermute aber mal, das Deine Auswahl schon einen etwas spekulativen Charakter hat und Du damit relativ schnell satte Kursgewinne mit den 4 Werten erwartest.

Ich hab momentan von den Ami-Bios XOMA, DSCO und den Rohrkrepierer EPCT.

Auf jeden Fall schon mal viel Erfolg mit Deinem Depot.

Von den 4 erwähnten Werten hab ich auch 2 auf der Watchlist.

Allerdings unter ca. 40 anderen.

Warum Du grad diese 4 gewählt hast, wirst Du uns sicher auch noch wissen lassen.

Was DSCO anbetrifft bin ich nicht ganz Deiner Meinung.

Ich vermute aber mal, das Deine Auswahl schon einen etwas spekulativen Charakter hat und Du damit relativ schnell satte Kursgewinne mit den 4 Werten erwartest.

Ich hab momentan von den Ami-Bios XOMA, DSCO und den Rohrkrepierer EPCT.

Auf jeden Fall schon mal viel Erfolg mit Deinem Depot.

Antwort auf Beitrag Nr.: 43.012.084 von zwitscherton am 06.04.12 23:57:55@ zwitscherton

...eigentlich dachte ich ja daß um diese Zeit keiner mehr so wie ich vor dem PC sitzt und sich ausgerechnet mit Aktien beschäftigt...aber falsch gedacht..

Danke dir schon mal für deine nette Resonanz - und ich bin mir fast sicher daß wir uns hier wieder treffen

XOMA hatte ja in den letzten Wochen auch schon einen guten Lauf - der sicherlich in nicht unerheblicher Weise mit seinem Mega-Anteilseigner (Felix Baker) zu tun hat...

Meiner Ansicht nach ist er derzeit einer der Jungs, die in der Branche die Nase ganz weit vorne haben - aber bei deinen eigenen Recherchen zu XOMA bist du da sicher längst schon selbst drauf gestoßen

EPCT.PK gehört zu den Werten die ich eingangs schon ansprach keinesfalls zu kaufen. Ist ja ein Wert aus den "pinkies" - die könnten Hühner züchten die goldene Eier legen und ich würde sie immer noch nicht anfassen....irgendwo liegt da immer ein Hund begraben und genau nach dem zu suchen geht für mich in die falsche Richtung.

DSCO können wir ja nochmal bei Gelegenheit aufgreifen und ein bißchen fachsimpeln...

...........................................................................

Zu DVAX stell ich morgen nochmal was rein - da rührt sich in den letzten Handelstagen ziemlich was....

...eigentlich dachte ich ja daß um diese Zeit keiner mehr so wie ich vor dem PC sitzt und sich ausgerechnet mit Aktien beschäftigt...aber falsch gedacht..

Danke dir schon mal für deine nette Resonanz - und ich bin mir fast sicher daß wir uns hier wieder treffen

XOMA hatte ja in den letzten Wochen auch schon einen guten Lauf - der sicherlich in nicht unerheblicher Weise mit seinem Mega-Anteilseigner (Felix Baker) zu tun hat...

Meiner Ansicht nach ist er derzeit einer der Jungs, die in der Branche die Nase ganz weit vorne haben - aber bei deinen eigenen Recherchen zu XOMA bist du da sicher längst schon selbst drauf gestoßen

EPCT.PK gehört zu den Werten die ich eingangs schon ansprach keinesfalls zu kaufen. Ist ja ein Wert aus den "pinkies" - die könnten Hühner züchten die goldene Eier legen und ich würde sie immer noch nicht anfassen....irgendwo liegt da immer ein Hund begraben und genau nach dem zu suchen geht für mich in die falsche Richtung.

DSCO können wir ja nochmal bei Gelegenheit aufgreifen und ein bißchen fachsimpeln...

...........................................................................

Zu DVAX stell ich morgen nochmal was rein - da rührt sich in den letzten Handelstagen ziemlich was....

warum gibt es in deinem depot keine europäischen biotech unternehmen?

in Q1 2012 war kursmässig für viele europäischen aktien sehr gut.

in Q1 2012 war kursmässig für viele europäischen aktien sehr gut.

Antwort auf Beitrag Nr.: 43.011.834 von Freizeitspekulant am 06.04.12 20:55:15DVAX gefält mir auch!

ACADIA war 2008 bei über 15 USD und im märz bei 1,5 USD. der akt. börsenwert liegt bei unter 80 mio €

was ist da so spannend? erscheint mir eine sehr riskante angelegenheit mit viel zockern

HZNP in 2011 war der kurs bei 11 jetzt bei 4 usd , börsenwert bei 60 miop € . kein überzeugendes verhalten an der börse...

GTXI war 2008 bei über 20 USD, 2012 zwischen 2,5 und 6,75 und aktuell bei 3,8 USD. immerhin ein börsenwert von 220 mio €. was ist an der firma spannend?

mein fazit:

ausser dvax sehr sehr riskante firmen die an der börse massiv enttäuschten.

ACADIA war 2008 bei über 15 USD und im märz bei 1,5 USD. der akt. börsenwert liegt bei unter 80 mio €

was ist da so spannend? erscheint mir eine sehr riskante angelegenheit mit viel zockern

HZNP in 2011 war der kurs bei 11 jetzt bei 4 usd , börsenwert bei 60 miop € . kein überzeugendes verhalten an der börse...

GTXI war 2008 bei über 20 USD, 2012 zwischen 2,5 und 6,75 und aktuell bei 3,8 USD. immerhin ein börsenwert von 220 mio €. was ist an der firma spannend?

mein fazit:

ausser dvax sehr sehr riskante firmen die an der börse massiv enttäuschten.

Trading Spotlight

Antwort auf Beitrag Nr.: 43.011.834 von Freizeitspekulant am 06.04.12 20:55:15Hallo!

Ich wollte mich noch für die Thread Eröffnung bedanken! Ein Daumen stammt von mir.

Das ist ein Sektor, in dem ich leider sehr untergewichtet bin, da ich irgendwie hier nie so richtig "reinkomme" Ich hatte nur mal eine Weile relativ konservative Werte, wie z.B. HITK. Ansonsten spiele ich maximal die News (erfolgreicher Phase III Test) und gehe dann wieder raus.

Ich würde mich aber schon intensiver mit dem Sektor befassen wollen. Mich würde da interessieren, wie Ihr das so handhabt? Nach welchen Kriterien findet man so einen Titel? Es gibt ja Leute, die kennen einen Haufen Termine im Schlaf - bei welcher Firma welche Tests wie weit fortgeschritten sind... Ich habe auch die Links z.B. zu der US-Seite, wo alle Tests dokumentiert sind. Habe das aber irgendwie noch nicht in Anlageentscheidungen umsetzen können.

Die eine oder andere Firma, die ich eigentlich sehr interessant finde, die läuft dann aber doch nicht so richtig. Z.B. ein Unternehmen aus Skandinavien ist wohl an einem Mittel dran, gegen Alkoholismus. Das müsste doch eigentlich ein Blockbuster sein, wenns funktioniert. Aber in der Zeit, wo ich die Firma beobachtete, war das eher ein Mauerblümchen...

Also, mich würden da immer mal auch Eure Erfahrungen interessieren, wenn Ihr Zeit und Lust habt, und wie Ihr da recherchiert und auswählt.

Wenn der eine oder andere Mediziner ist, dann schadet das auch nicht unbedingt, habe ich aus früheren Zeiten gelernt.

Viele Grüße + Schöne Ostern

s.

Ich wollte mich noch für die Thread Eröffnung bedanken! Ein Daumen stammt von mir.

Das ist ein Sektor, in dem ich leider sehr untergewichtet bin, da ich irgendwie hier nie so richtig "reinkomme" Ich hatte nur mal eine Weile relativ konservative Werte, wie z.B. HITK. Ansonsten spiele ich maximal die News (erfolgreicher Phase III Test) und gehe dann wieder raus.

Ich würde mich aber schon intensiver mit dem Sektor befassen wollen. Mich würde da interessieren, wie Ihr das so handhabt? Nach welchen Kriterien findet man so einen Titel? Es gibt ja Leute, die kennen einen Haufen Termine im Schlaf - bei welcher Firma welche Tests wie weit fortgeschritten sind... Ich habe auch die Links z.B. zu der US-Seite, wo alle Tests dokumentiert sind. Habe das aber irgendwie noch nicht in Anlageentscheidungen umsetzen können.

Die eine oder andere Firma, die ich eigentlich sehr interessant finde, die läuft dann aber doch nicht so richtig. Z.B. ein Unternehmen aus Skandinavien ist wohl an einem Mittel dran, gegen Alkoholismus. Das müsste doch eigentlich ein Blockbuster sein, wenns funktioniert. Aber in der Zeit, wo ich die Firma beobachtete, war das eher ein Mauerblümchen...

Also, mich würden da immer mal auch Eure Erfahrungen interessieren, wenn Ihr Zeit und Lust habt, und wie Ihr da recherchiert und auswählt.

Wenn der eine oder andere Mediziner ist, dann schadet das auch nicht unbedingt, habe ich aus früheren Zeiten gelernt.

Viele Grüße + Schöne Ostern

s.

Antwort auf Beitrag Nr.: 43.012.109 von Freizeitspekulant am 07.04.12 00:43:21Hier also mal ein paar Begebenheiten zum Unternehmen, sowie meine persönliche Betrachtungweise zu meinem Investment in DVAX:

• HEPLISAV

heißt hier das Zauberwort – nach den zuletzt unternehmensseitig berichteten Top-Daten der abschließenden P III-Phase für diese Anwendung gegenüber Engerix von GSK erscheint klar daß HEPLISAV die Ablösung der bisherigen Marktführerschaft von Engerix sein dürfte. Daß GSK hierzu reagieren muß ist klar – vermutlich wird man sich nicht die Butter vom Brot nehmen lassen wollen. Ob dies nun in Form einer Partnerschaft gelöst wird oder kurzerhand ein Angebot zur Übernahme von DVAX erfolgt erscheint im Moment noch offen. Es stellt sich nur noch die Frage wie lange…

• BLA (Biologics License Application) wurde bereits für Mitte Mai angekündigt.

• Kapitalerhöhung

Erfolgreiche Platzierung von 24 Mio zusätzlichen Aktien zu je 2,50 $ pro Anteilsschein Anfang November 2011 an institutionelleAnleger. Die Kapitalerhöhung brachte dem Unternehmen somit 60 Mio. US-$ ein – wurde „kursunschädlich“ umgesetzt und bringt mir als Anleger schon mal die Sicherheit daß das Unternehmen mehr als ausreichende Kapitalreserven hat um seine strukturierte Planung auch entsprechend umsetzen zu können. Weitere Maßnahmen zur Erhöhung des Stammkapitals werden aus o.g. Gründen wohl nicht mehr erforderlich sein.

• Hauptaktionäre

DVAX – Anteile finden sich in sehr großen Mengen (60-70% der ausgegebenen Aktien ) in den Depots institutioneller Anleger, einige haben zuletzt auch ihre Beteiligungen erhöht.

• geshortete Aktien

Derzeit dürften 17-18 Mio. Shares geshortet sein – das ist sehr viel…und bringt hinsichtlich erforderlich werdender Shorteindeckungen enormes Kurspotenzial. Wie die Überlegung der Shorties aussieht ihre Leerverkäufe im Falle eines nicht wirklich überraschenden Übernahmeangebotes einzudecken ist mir etwas schleierhaft – ich würde hier jedenfalls nicht short sein wollen.

• Kursentwicklung und Chart

DVAX ist bisher schon schön gelaufen und hat den Biotech-Index klar outperformed. Dies wohl bislang in erster Linie weil zum einen der letzte Geschäftsbericht die Markterwartung klar übertroffen hatte, zudem haben die mehr als guten Ergebnisse von HEPLISAV sicher ihren Anteil dazu beigetragen daß der Kurs sich gleichermaßen gut entwickeln konnte. Der Chart – eine Augenweide. Derzeit sieht es charttechnisch gesehen nach weiterer Aufbruchstimmung gen Norden aus.

• Die Spekulation

- ein positiver FDA-Bescheid, sowie Zulassung in Europa dürfte in der bisherigen Kursentwicklung weitestgehend eingepreist sein. Die Zugpferde heißen jetzt Verpartnerung bzw. mögliche Übernahme. GSK dürfte hier aus genannten Gründen Hauptanwärter sein. Beim derzeitigen Kurs von 5,15 $ ist DVAX mit 800 Mio US-$ bewertet – mit einem Übernahmeangebot in der Gegend um 10 $ würde ein Bieter für 1,6 Mrd. US-$ noch günstig kaufen wenn man bedenkt sich so die unangefochtene Marktführerschaft für Jahre zu sichern, zudem die Restpipeline von DVAX quasi umsonst zu bekommen. Bei einer angestrebten Verpartnerung müßte ein Zweitinteressent erst mal GSK ausstechen – was sicher auch nicht billig wird. Beabsichtigt GSK eine Verpartnerung wird DVAX sicher eine sehr hohe Upfront-Zahlung plus mindestens 20+X% Beteiligung am Gewinn herausholen können.

• DVAX in meinem Depot

Ich halte meine Anteile derzeit fast schon als „BlueChip“ unter dem Rest was da sonst noch drin ist. Entsprechend hoch ist daher auch die prozentuale Gewichtung in Bezug auf den Gesamtinhalt. Obwohl ja in den letzten Wochen einige Unternehmen mit ihren jeweiligen Zulassungsanträgen teils unerwartet – und mit den in diesem Fall nicht unüblich deftigen Kursverlusten gescheitert sind, beabsichtige ich meine DVAX-Anteile durch die „FDA-Endabnahme“ zu halten.

PS: einen Chart von DVAX hätte ich eigentlich hier auch noch miteinbrngen wollen - hab es aber auf die Schnelle nicht auf die Reihe bekommen - muß mich anscheinend nochmal in die w:o-Technologie einarbeiten

• HEPLISAV

heißt hier das Zauberwort – nach den zuletzt unternehmensseitig berichteten Top-Daten der abschließenden P III-Phase für diese Anwendung gegenüber Engerix von GSK erscheint klar daß HEPLISAV die Ablösung der bisherigen Marktführerschaft von Engerix sein dürfte. Daß GSK hierzu reagieren muß ist klar – vermutlich wird man sich nicht die Butter vom Brot nehmen lassen wollen. Ob dies nun in Form einer Partnerschaft gelöst wird oder kurzerhand ein Angebot zur Übernahme von DVAX erfolgt erscheint im Moment noch offen. Es stellt sich nur noch die Frage wie lange…

• BLA (Biologics License Application) wurde bereits für Mitte Mai angekündigt.

• Kapitalerhöhung

Erfolgreiche Platzierung von 24 Mio zusätzlichen Aktien zu je 2,50 $ pro Anteilsschein Anfang November 2011 an institutionelleAnleger. Die Kapitalerhöhung brachte dem Unternehmen somit 60 Mio. US-$ ein – wurde „kursunschädlich“ umgesetzt und bringt mir als Anleger schon mal die Sicherheit daß das Unternehmen mehr als ausreichende Kapitalreserven hat um seine strukturierte Planung auch entsprechend umsetzen zu können. Weitere Maßnahmen zur Erhöhung des Stammkapitals werden aus o.g. Gründen wohl nicht mehr erforderlich sein.

• Hauptaktionäre

DVAX – Anteile finden sich in sehr großen Mengen (60-70% der ausgegebenen Aktien ) in den Depots institutioneller Anleger, einige haben zuletzt auch ihre Beteiligungen erhöht.

• geshortete Aktien

Derzeit dürften 17-18 Mio. Shares geshortet sein – das ist sehr viel…und bringt hinsichtlich erforderlich werdender Shorteindeckungen enormes Kurspotenzial. Wie die Überlegung der Shorties aussieht ihre Leerverkäufe im Falle eines nicht wirklich überraschenden Übernahmeangebotes einzudecken ist mir etwas schleierhaft – ich würde hier jedenfalls nicht short sein wollen.

• Kursentwicklung und Chart

DVAX ist bisher schon schön gelaufen und hat den Biotech-Index klar outperformed. Dies wohl bislang in erster Linie weil zum einen der letzte Geschäftsbericht die Markterwartung klar übertroffen hatte, zudem haben die mehr als guten Ergebnisse von HEPLISAV sicher ihren Anteil dazu beigetragen daß der Kurs sich gleichermaßen gut entwickeln konnte. Der Chart – eine Augenweide. Derzeit sieht es charttechnisch gesehen nach weiterer Aufbruchstimmung gen Norden aus.

• Die Spekulation

- ein positiver FDA-Bescheid, sowie Zulassung in Europa dürfte in der bisherigen Kursentwicklung weitestgehend eingepreist sein. Die Zugpferde heißen jetzt Verpartnerung bzw. mögliche Übernahme. GSK dürfte hier aus genannten Gründen Hauptanwärter sein. Beim derzeitigen Kurs von 5,15 $ ist DVAX mit 800 Mio US-$ bewertet – mit einem Übernahmeangebot in der Gegend um 10 $ würde ein Bieter für 1,6 Mrd. US-$ noch günstig kaufen wenn man bedenkt sich so die unangefochtene Marktführerschaft für Jahre zu sichern, zudem die Restpipeline von DVAX quasi umsonst zu bekommen. Bei einer angestrebten Verpartnerung müßte ein Zweitinteressent erst mal GSK ausstechen – was sicher auch nicht billig wird. Beabsichtigt GSK eine Verpartnerung wird DVAX sicher eine sehr hohe Upfront-Zahlung plus mindestens 20+X% Beteiligung am Gewinn herausholen können.

• DVAX in meinem Depot

Ich halte meine Anteile derzeit fast schon als „BlueChip“ unter dem Rest was da sonst noch drin ist. Entsprechend hoch ist daher auch die prozentuale Gewichtung in Bezug auf den Gesamtinhalt. Obwohl ja in den letzten Wochen einige Unternehmen mit ihren jeweiligen Zulassungsanträgen teils unerwartet – und mit den in diesem Fall nicht unüblich deftigen Kursverlusten gescheitert sind, beabsichtige ich meine DVAX-Anteile durch die „FDA-Endabnahme“ zu halten.

PS: einen Chart von DVAX hätte ich eigentlich hier auch noch miteinbrngen wollen - hab es aber auf die Schnelle nicht auf die Reihe bekommen - muß mich anscheinend nochmal in die w:o-Technologie einarbeiten

ein allgemeiner Biotech-Thread... sehr schön!

Bin auch seit vielen Jahren hauptsächlich in Biotechs investiert. Dieser Sektor ist in der Tat nicht gerade risikolos. Nach meiner Erfahrung darf man sich nie sicher sein, dass eine Aktie statt eines erwarteten Gewinns nicht plötzlich zur Nullnummer wird... selbst wenn die Story sich so toll und plausibel anhört. D.h. egal worauf du setzt, kalkuliere immer ein, dass es auch komplett schiefgehen kann! Man kann sich niemals sicher sein, dass z.B. eine PIII erfolgreich ist, dass eine Zulassung erfolgt oder dass nach einer Zulassung sich das Produkt auch erfolgreich verkaufen lässt. Oft fällt auch der Kurs, obwohl beispielsweise ein klinische Studie erfolgreich war, weil der Markt doch mehr erwartet oder in der nächsten Zeit nichts besseres erwartet. Von denen, die Erfolg haben, wirst du immer hören, dass sie das doch immer schon wussten und die, die ein Großteil verlieren, verschwinden in der Versenkung und hoffen auf Besserung. Man darf sich da nicht blenden lassen von Leuten, die die tolle Story haben oder sich sehr sicher sind. Die Aussage "Eine Zulassung halte ich für sehr sicher" ist bestenfalls wertlos, oft auch ein Kontraindikator! Dann sollte man sich das ganze umso genauer anschauen und sich nicht davon verleiten lassen!

Wie wählst du denn deine Werte aus? Ich bin kein Mediziner und ich wette, dass auch ein Mediziner nicht einen Erfolg oder einen Kursgewinn voraussehen kann. Es dürfte kaum möglich sein, eine einzelne Aktie so zu durchleuten, dass man alle Fallstricke findet. Also ich habe die Zeit nicht und ich halte dies auch für unnötig. Trotzdem benötigt man Infos... und nach meiner Erfahrung gibt es sehr wenige brauchbare Infos. Viele "Analysen", "Reports" oder "Empfehlungen" sind es überhaupt nicht wert, gelesen zu werden. Ein Kriterium für mich, ob eine Quelle brauchbar ist oder nicht, ist, ob jemand auch kritische Fragen stellt. Eine differenzierte Betrachtung, die sowohl das positive als auch das negative herausarbeitet, ist für mich brauchbar... kritische Stimmen sind oft hilfreich, dass man nicht alles zu rosa und optimistisch sieht.

Hast du gute Quellen? Meine Quellen sind z.B.

http://www.hammerstockblog.com/

http://pharmastrategyblog.com/

brauchbar ist auch...

http://investorshub.advfn.com/boards/board.aspx?board_id=141…

http://www.siliconinvestor.com/home.aspx?forumid=102&sort=5&…

http://www.thestreet.com/author/1352996/adam-feuerstein/all.…

http://www.fiercebiotech.com/

Außerdem bin ich vorsichtig, wenn u.a. ...

- ein Unternehmen nur ein aussichtsreiches Produkt in der Entwicklung hat, von dem alles abhängt

- ein Unternehmen in der Vergangenheit nur schlechte Ergebnisse erzielt hat

- die Marktkapitalisierung sehr klein ist (<200 Mio)

- es kein amerikanisches Unternehmen ist

- der Cash-Bestand gerade so zum Überleben reicht

Inzwischen fühle ich mich wohler, wenn ich das Risiko auf möglichst viele für mich aussichtsreiche Werte verteile. So komme ich meistens auf 20-30 Werte, wodurch ich zwar von positiven Ereignissen relativ wenig profitiere, aber auch locker einige Totalausfälle wegstecken kann.

Momentan sind meine Werte jeweils mit Gewichtung...

10,9% Pharmacyclics http://finance.yahoo.com/q?s=PCYC

10,2% Regeneron http://finance.yahoo.com/q?s=REGN

8,1% Incyte http://finance.yahoo.com/q?s=INCY

6,9% Cubist http://finance.yahoo.com/q?s=CBST

6,6% Onyx http://finance.yahoo.com/q?s=ONXX

6,1% Array http://finance.yahoo.com/q?s=ARRY

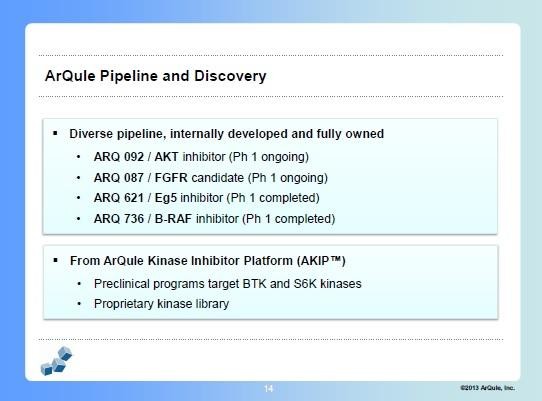

5,3% ArQule http://finance.yahoo.com/q?s=ARQL

4,9% Exelixis http://finance.yahoo.com/q?s=EXEL

3,8% Celldex http://finance.yahoo.com/q?s=CLDX

3,8% Seattle Genetics http://finance.yahoo.com/q?s=SGEN

3,1% Ziopharm http://finance.yahoo.com/q?s=ZIOP

3,1% Isis http://finance.yahoo.com/q?s=ISIS

3,0% AVEO http://finance.yahoo.com/q?s=AVEO

2,8% Threshold http://finance.yahoo.com/q?s=THLD

2,8% Rigel http://finance.yahoo.com/q?s=RIGL

2,7% ViroPharma http://finance.yahoo.com/q?s=VPHM

2,7% Alnylam http://finance.yahoo.com/q?s=ALNY

2,7% Intermune http://finance.yahoo.com/q?s=INTM

2,7% Synta http://finance.yahoo.com/q?s=SNTA

2,1% Genmab http://finance.yahoo.com/q?s=GEN.CO

1,9% YM BioScience http://finance.yahoo.com/q?s=YMI

1,5% Trius http://finance.yahoo.com/q?s=TSRX

1,0% Arena http://finance.yahoo.com/q?s=ARNA

0,9% AMAG http://finance.yahoo.com/q?s=AMAG

0,4% Targacept http://finance.yahoo.com/q?s=TRGT

0,2% NeuroSearch http://finance.yahoo.com/q?s=NEUR.CO

0,1% NeurogesX http://finance.yahoo.com/q?s=NGSX

Unten sammeln sich die Leichen, die ich irgendwann aussortiere.

Von deinen Werten habe ich mir zuletzt mal GTXI angesehen, die vielleicht in Frage kommen könnten. Allerdings beginne ich ein Position meist eher mit einem ca. 2% Anteil. Die anderen schaue ich mir auch nochmal an, sind mir aber bisher wohl nicht weiter aufgefallen.

Viel Erfolg mit deinen Investitionen!

Bin auch seit vielen Jahren hauptsächlich in Biotechs investiert. Dieser Sektor ist in der Tat nicht gerade risikolos. Nach meiner Erfahrung darf man sich nie sicher sein, dass eine Aktie statt eines erwarteten Gewinns nicht plötzlich zur Nullnummer wird... selbst wenn die Story sich so toll und plausibel anhört. D.h. egal worauf du setzt, kalkuliere immer ein, dass es auch komplett schiefgehen kann! Man kann sich niemals sicher sein, dass z.B. eine PIII erfolgreich ist, dass eine Zulassung erfolgt oder dass nach einer Zulassung sich das Produkt auch erfolgreich verkaufen lässt. Oft fällt auch der Kurs, obwohl beispielsweise ein klinische Studie erfolgreich war, weil der Markt doch mehr erwartet oder in der nächsten Zeit nichts besseres erwartet. Von denen, die Erfolg haben, wirst du immer hören, dass sie das doch immer schon wussten und die, die ein Großteil verlieren, verschwinden in der Versenkung und hoffen auf Besserung. Man darf sich da nicht blenden lassen von Leuten, die die tolle Story haben oder sich sehr sicher sind. Die Aussage "Eine Zulassung halte ich für sehr sicher" ist bestenfalls wertlos, oft auch ein Kontraindikator! Dann sollte man sich das ganze umso genauer anschauen und sich nicht davon verleiten lassen!

Wie wählst du denn deine Werte aus? Ich bin kein Mediziner und ich wette, dass auch ein Mediziner nicht einen Erfolg oder einen Kursgewinn voraussehen kann. Es dürfte kaum möglich sein, eine einzelne Aktie so zu durchleuten, dass man alle Fallstricke findet. Also ich habe die Zeit nicht und ich halte dies auch für unnötig. Trotzdem benötigt man Infos... und nach meiner Erfahrung gibt es sehr wenige brauchbare Infos. Viele "Analysen", "Reports" oder "Empfehlungen" sind es überhaupt nicht wert, gelesen zu werden. Ein Kriterium für mich, ob eine Quelle brauchbar ist oder nicht, ist, ob jemand auch kritische Fragen stellt. Eine differenzierte Betrachtung, die sowohl das positive als auch das negative herausarbeitet, ist für mich brauchbar... kritische Stimmen sind oft hilfreich, dass man nicht alles zu rosa und optimistisch sieht.

Hast du gute Quellen? Meine Quellen sind z.B.

http://www.hammerstockblog.com/

http://pharmastrategyblog.com/

brauchbar ist auch...

http://investorshub.advfn.com/boards/board.aspx?board_id=141…

http://www.siliconinvestor.com/home.aspx?forumid=102&sort=5&…

http://www.thestreet.com/author/1352996/adam-feuerstein/all.…

http://www.fiercebiotech.com/

Außerdem bin ich vorsichtig, wenn u.a. ...

- ein Unternehmen nur ein aussichtsreiches Produkt in der Entwicklung hat, von dem alles abhängt

- ein Unternehmen in der Vergangenheit nur schlechte Ergebnisse erzielt hat

- die Marktkapitalisierung sehr klein ist (<200 Mio)

- es kein amerikanisches Unternehmen ist

- der Cash-Bestand gerade so zum Überleben reicht

Inzwischen fühle ich mich wohler, wenn ich das Risiko auf möglichst viele für mich aussichtsreiche Werte verteile. So komme ich meistens auf 20-30 Werte, wodurch ich zwar von positiven Ereignissen relativ wenig profitiere, aber auch locker einige Totalausfälle wegstecken kann.

Momentan sind meine Werte jeweils mit Gewichtung...

10,9% Pharmacyclics http://finance.yahoo.com/q?s=PCYC

10,2% Regeneron http://finance.yahoo.com/q?s=REGN

8,1% Incyte http://finance.yahoo.com/q?s=INCY

6,9% Cubist http://finance.yahoo.com/q?s=CBST

6,6% Onyx http://finance.yahoo.com/q?s=ONXX

6,1% Array http://finance.yahoo.com/q?s=ARRY

5,3% ArQule http://finance.yahoo.com/q?s=ARQL

4,9% Exelixis http://finance.yahoo.com/q?s=EXEL

3,8% Celldex http://finance.yahoo.com/q?s=CLDX

3,8% Seattle Genetics http://finance.yahoo.com/q?s=SGEN

3,1% Ziopharm http://finance.yahoo.com/q?s=ZIOP

3,1% Isis http://finance.yahoo.com/q?s=ISIS

3,0% AVEO http://finance.yahoo.com/q?s=AVEO

2,8% Threshold http://finance.yahoo.com/q?s=THLD

2,8% Rigel http://finance.yahoo.com/q?s=RIGL

2,7% ViroPharma http://finance.yahoo.com/q?s=VPHM

2,7% Alnylam http://finance.yahoo.com/q?s=ALNY

2,7% Intermune http://finance.yahoo.com/q?s=INTM

2,7% Synta http://finance.yahoo.com/q?s=SNTA

2,1% Genmab http://finance.yahoo.com/q?s=GEN.CO

1,9% YM BioScience http://finance.yahoo.com/q?s=YMI

1,5% Trius http://finance.yahoo.com/q?s=TSRX

1,0% Arena http://finance.yahoo.com/q?s=ARNA

0,9% AMAG http://finance.yahoo.com/q?s=AMAG

0,4% Targacept http://finance.yahoo.com/q?s=TRGT

0,2% NeuroSearch http://finance.yahoo.com/q?s=NEUR.CO

0,1% NeurogesX http://finance.yahoo.com/q?s=NGSX

Unten sammeln sich die Leichen, die ich irgendwann aussortiere.

Von deinen Werten habe ich mir zuletzt mal GTXI angesehen, die vielleicht in Frage kommen könnten. Allerdings beginne ich ein Position meist eher mit einem ca. 2% Anteil. Die anderen schaue ich mir auch nochmal an, sind mir aber bisher wohl nicht weiter aufgefallen.

Viel Erfolg mit deinen Investitionen!

Antwort auf Beitrag Nr.: 43.012.332 von pokemon am 07.04.12 09:53:06@pokemon

hast Recht - da sind keine europäischen Unternehmen mit drinnen - außer durch DVAX die vielleicht dir noch bekannte Rhein Biotech...

Ich habe mich auch so gut wie garnicht mit den europäischen Unternehmen beschäftigt. Vermutlich wird auch dort oder da ordentliche Arbeit abgeliefert - wir hängen aber hierzu viel zu sehr (..schon allein aus markttechnischen Gründen) am Tropf des amerikanischen Marktes.

Ein paar Unternehmen aus Kanada hab ich mir mal näher ausgeleuchtet - aber auch dort die Finger weggelassen weil mich die Kanadier mit gelegentlich wenig nachvollziebarem Agieren an der Börse verblüfft hatten - irgendeiner machte da immer gewaltig Kasse wenn irgendwo positive News anstanden.

Klar ist sell the news auch ein Marktinstrument - aber die Markttransparenz konnte mich nicht wirklich begeistern...

Da hab ich eben lieber die US-Werte...

hast Recht - da sind keine europäischen Unternehmen mit drinnen - außer durch DVAX die vielleicht dir noch bekannte Rhein Biotech...

Ich habe mich auch so gut wie garnicht mit den europäischen Unternehmen beschäftigt. Vermutlich wird auch dort oder da ordentliche Arbeit abgeliefert - wir hängen aber hierzu viel zu sehr (..schon allein aus markttechnischen Gründen) am Tropf des amerikanischen Marktes.

Ein paar Unternehmen aus Kanada hab ich mir mal näher ausgeleuchtet - aber auch dort die Finger weggelassen weil mich die Kanadier mit gelegentlich wenig nachvollziebarem Agieren an der Börse verblüfft hatten - irgendeiner machte da immer gewaltig Kasse wenn irgendwo positive News anstanden.

Klar ist sell the news auch ein Marktinstrument - aber die Markttransparenz konnte mich nicht wirklich begeistern...

Da hab ich eben lieber die US-Werte...

Antwort auf Beitrag Nr.: 43.012.375 von pokemon am 07.04.12 10:12:33@pokemon

...so finde ich sollte man es nicht sehen weil Firmen gelegentlich "unter die Räder kommen" - manche auch nicht unberechtigt...aber ein Teil der eigentllich ursprünglichen Börsenspekulation basierte darauf genau solche "platten" Unternehmen aufzustöbern und an ihrer Rehabilitation und/oder dem sich dann abzeichnendem zukünftigen Erfolg mitzuverdienen - und das gehörig.

Ich habe vor einigen Jahren(!!!) Anteile eines Unternehmens mit dem Namen Inhibitex (INHX) für zum Sensationspreis von unter 40 US-Cent gekauft. Das Unternehmen wurde genauso als Rohrkrepierer mit miserabler Kursentwicklung nach einer vergeigten FDA-Zulassung bezeichnet. Vor ein paar Wochen wurden dann im Zuge der Übernahme für die Anteile 26 US-$ bezahlt...

Wie ich sagte - ich versuche mit verschiedenen Strategien Gewinne zu machen - Perlen aufzutun wenn sich noch keiner mit Ihnen befasst ist eine davon - meine Lieblingsstrategie. Du wirst nirgends so viel verdienen können wie mit Perlenfischen. Rauf und runter traden kann schöne Gewinne bringen -aber niemals in dieser Höhe wie "buy cheap - sell high"

Viel wichtiger ist es herauszufinden was hat ein "gestraucheltes" Unternehmen in der Pipeline - was kann man daraus machen - und tun sie es auch? Da spielt es für mich keine Rolle ob - wie du sagst ein Wert der jetzt bei 1,80$ steht vor vier Jahren noch bei 15$ lag - nicht das was hinter mir liegt ist wichtig - was zählt ist das was die Zukunft eventuell mit im Gepäck hat

Auch meine ACADIA-Anteile habe ich schon eingesackt als der Kurs bei exakt bei 1 US-$ lag. Jeder Trader hätte sie sicher schon nach eingefahrenen 20-30% Gewinn wieder versilbert - mir waren sogar die mittlerweile schon bezahlten 2,30 $ zu wenig dafür welches Potenzial in ACAD steckt.

Sobald es mir zeitlich ausgeht stell ich mal Infos zu ACAD, GTXI und HZNP rein.

...so finde ich sollte man es nicht sehen weil Firmen gelegentlich "unter die Räder kommen" - manche auch nicht unberechtigt...aber ein Teil der eigentllich ursprünglichen Börsenspekulation basierte darauf genau solche "platten" Unternehmen aufzustöbern und an ihrer Rehabilitation und/oder dem sich dann abzeichnendem zukünftigen Erfolg mitzuverdienen - und das gehörig.

Ich habe vor einigen Jahren(!!!) Anteile eines Unternehmens mit dem Namen Inhibitex (INHX) für zum Sensationspreis von unter 40 US-Cent gekauft. Das Unternehmen wurde genauso als Rohrkrepierer mit miserabler Kursentwicklung nach einer vergeigten FDA-Zulassung bezeichnet. Vor ein paar Wochen wurden dann im Zuge der Übernahme für die Anteile 26 US-$ bezahlt...

Wie ich sagte - ich versuche mit verschiedenen Strategien Gewinne zu machen - Perlen aufzutun wenn sich noch keiner mit Ihnen befasst ist eine davon - meine Lieblingsstrategie. Du wirst nirgends so viel verdienen können wie mit Perlenfischen. Rauf und runter traden kann schöne Gewinne bringen -aber niemals in dieser Höhe wie "buy cheap - sell high"

Viel wichtiger ist es herauszufinden was hat ein "gestraucheltes" Unternehmen in der Pipeline - was kann man daraus machen - und tun sie es auch? Da spielt es für mich keine Rolle ob - wie du sagst ein Wert der jetzt bei 1,80$ steht vor vier Jahren noch bei 15$ lag - nicht das was hinter mir liegt ist wichtig - was zählt ist das was die Zukunft eventuell mit im Gepäck hat

Auch meine ACADIA-Anteile habe ich schon eingesackt als der Kurs bei exakt bei 1 US-$ lag. Jeder Trader hätte sie sicher schon nach eingefahrenen 20-30% Gewinn wieder versilbert - mir waren sogar die mittlerweile schon bezahlten 2,30 $ zu wenig dafür welches Potenzial in ACAD steckt.

Sobald es mir zeitlich ausgeht stell ich mal Infos zu ACAD, GTXI und HZNP rein.

Antwort auf Beitrag Nr.: 43.012.793 von ipollit am 07.04.12 14:00:42@ipollit

Natürlich bleibt Biotech immer Biotech - soll heißen Risiko bleibt Risiko...es kann in zeitlichen Abständen größer oder kleiner werden, aber das ist in allen Sektoren so - sogar bei den Finanzwerten (oder da zur Zeit vielleicht gerade besonders..wer weis..)

Jeder muß immer selbst wissen vieviel Risiko er und sein Geldbeutel verträgt - war immer so - wird immer so bleiben.

Was mir aber immer wieder besonders auffällt ist daß sich die breite Masse mit Technik befasst - wie z.B. bei Autos. Hauptkriterium für viele ist in möglichst kurzer Zeit schnell von a nach b zu kommen. Ich freu mich auch wenn es sich flüssig fahren läßt - jedoch betrachte ich Technik auch von der Warte her mir zu sagen ich möchte gesund bei Punkt b ankommen und nutze auch die in der Technik mittlerweile involvierte Sicherheit.

Heutzutage ist der Handel gegenüber früher sehr schnell geworden - aber trotzdem bietet er für manches Instrumente die gegen den Totalcrash absichern - nur nicht gegen falsche Denkweise...da gibt es noch nichts... Für ersteres hilft beispielsweise ein Stopp-Loss - auch keine ganz neue Errungenschaft mehr...aber zumindest eine mit der man sich zu vorher durchdachtem Konzept selbst erziehen kann....

Keiner deiner Werte ist mir unbekannt - besonders Cubist (CBST) - welche ja auch schon zum Spottpreis zu haben waren, als kleine extrem spekulative Depotbeimischung im 1-2%-Bereich betitelt wurden - heute mit gut 2,5 Milliarden Marktkap. eher schon eine Hausnummer sind - aber auch THLD - die mir wegen eines zu eng gesetzten Kauflimits von 1,27 $ am Abend vor der ersten Kursexplosion von über 100% durch die Lappen gingen...aber das nur am Rande...

Verursacht deine extrem breite Streuung nicht oftmals das Scenario daß ein paar deiner Werte kräftig zulegen - der Gewinn aber durch rote Vorzeichen bei anderen dutlich geschmälert - wenn nicht sogar komplett verfrühstückt wird?

Mir sind derzeit ca. 150 US-Unternehmen relativ gut bekannt - können auch ein paar mehr sein..ohne OTC-Werte. Habe da schon meist einen guten Überblick wo unternehmensrelevante Dinge am Köcheln sind...informiere mich oft über Wochengeschehen wo es besonder interessant wird. Sehr aufschlußreich ist es auch zu beobachten und zu hinterfragen wo Insider oder große (erfolgreiche) Fonds gerade auf Einkaufstour gehen. Selbst da gibt es Favouriten, die gemessen am Erfolg einfach mehr als nur Glück haben um immer wieder zur richtigen Zeit genau die richtigen Aktien zu kaufen.... Ein Schelm der böses dabei denkt...

Die von dir genannten Boards gelegentlich mal zu durchblättern um sich auch mit Gedanken anderer auseinanderzusetzen kann auch hilfreich sein - allerdings rate ich davon ab sich von dem "Kaufen-Kaufen-Geschrei" oder seinem Gegenteil auf manchen Boards in der eigenen Investmententscheidung drängen zu lassen. Ich gebe auch zu daß es mir in 10 Jahren Börse noch bei keiner Aktie gelungen ist zum historischen Tiefstkurs zu kaufen - ein paar Cent billiger hat es die immer nochmal gegeben...was mich allerdings auch nicht stört wenn hinterher die von mir anvisierte Richtung stimmt.

Was mir besonders bei deinen Werten auffällt sind zwei Dinge: zum einen findet sich darunter kein einziger Wert der regelmäßig von so gewissen kurspushenden Seiten beackert wird um ihn an einem Tag 50% in die Höhe zu treiben - tags darauf wird der dann vom Verfasserkollegen als massive Shortchance wieder 30% nach unten gestampft...mit dem Ergebnis daß der Kurs wieder auf Ausgangsniveau angelangt ist - die meisten Zugestiegenen(außer den Daytradern) jedoch schon mal auf den ersten Minuszeichen sitzen....

Ist es Zufall daß z.B. eine Alexion Pharma fehlt oder ist es der optisch hohe Preis der dich davon abgehalten hat ein Paar Stücke mit einzubeziehen?

.. auch dir Erfolg mit deinem Fonds :-))

Natürlich bleibt Biotech immer Biotech - soll heißen Risiko bleibt Risiko...es kann in zeitlichen Abständen größer oder kleiner werden, aber das ist in allen Sektoren so - sogar bei den Finanzwerten (oder da zur Zeit vielleicht gerade besonders..wer weis..)

Jeder muß immer selbst wissen vieviel Risiko er und sein Geldbeutel verträgt - war immer so - wird immer so bleiben.

Was mir aber immer wieder besonders auffällt ist daß sich die breite Masse mit Technik befasst - wie z.B. bei Autos. Hauptkriterium für viele ist in möglichst kurzer Zeit schnell von a nach b zu kommen. Ich freu mich auch wenn es sich flüssig fahren läßt - jedoch betrachte ich Technik auch von der Warte her mir zu sagen ich möchte gesund bei Punkt b ankommen und nutze auch die in der Technik mittlerweile involvierte Sicherheit.

Heutzutage ist der Handel gegenüber früher sehr schnell geworden - aber trotzdem bietet er für manches Instrumente die gegen den Totalcrash absichern - nur nicht gegen falsche Denkweise...da gibt es noch nichts...

Für ersteres hilft beispielsweise ein Stopp-Loss - auch keine ganz neue Errungenschaft mehr...aber zumindest eine mit der man sich zu vorher durchdachtem Konzept selbst erziehen kann....Keiner deiner Werte ist mir unbekannt - besonders Cubist (CBST) - welche ja auch schon zum Spottpreis zu haben waren, als kleine extrem spekulative Depotbeimischung im 1-2%-Bereich betitelt wurden - heute mit gut 2,5 Milliarden Marktkap. eher schon eine Hausnummer sind - aber auch THLD - die mir wegen eines zu eng gesetzten Kauflimits von 1,27 $ am Abend vor der ersten Kursexplosion von über 100% durch die Lappen gingen...aber das nur am Rande...

Verursacht deine extrem breite Streuung nicht oftmals das Scenario daß ein paar deiner Werte kräftig zulegen - der Gewinn aber durch rote Vorzeichen bei anderen dutlich geschmälert - wenn nicht sogar komplett verfrühstückt wird?

Mir sind derzeit ca. 150 US-Unternehmen relativ gut bekannt - können auch ein paar mehr sein..ohne OTC-Werte. Habe da schon meist einen guten Überblick wo unternehmensrelevante Dinge am Köcheln sind...informiere mich oft über Wochengeschehen wo es besonder interessant wird. Sehr aufschlußreich ist es auch zu beobachten und zu hinterfragen wo Insider oder große (erfolgreiche) Fonds gerade auf Einkaufstour gehen. Selbst da gibt es Favouriten, die gemessen am Erfolg einfach mehr als nur Glück haben um immer wieder zur richtigen Zeit genau die richtigen Aktien zu kaufen.... Ein Schelm der böses dabei denkt...

Die von dir genannten Boards gelegentlich mal zu durchblättern um sich auch mit Gedanken anderer auseinanderzusetzen kann auch hilfreich sein - allerdings rate ich davon ab sich von dem "Kaufen-Kaufen-Geschrei" oder seinem Gegenteil auf manchen Boards in der eigenen Investmententscheidung drängen zu lassen. Ich gebe auch zu daß es mir in 10 Jahren Börse noch bei keiner Aktie gelungen ist zum historischen Tiefstkurs zu kaufen - ein paar Cent billiger hat es die immer nochmal gegeben...was mich allerdings auch nicht stört wenn hinterher die von mir anvisierte Richtung stimmt.

Was mir besonders bei deinen Werten auffällt sind zwei Dinge: zum einen findet sich darunter kein einziger Wert der regelmäßig von so gewissen kurspushenden Seiten beackert wird um ihn an einem Tag 50% in die Höhe zu treiben - tags darauf wird der dann vom Verfasserkollegen als massive Shortchance wieder 30% nach unten gestampft...mit dem Ergebnis daß der Kurs wieder auf Ausgangsniveau angelangt ist - die meisten Zugestiegenen(außer den Daytradern) jedoch schon mal auf den ersten Minuszeichen sitzen....

Ist es Zufall daß z.B. eine Alexion Pharma fehlt oder ist es der optisch hohe Preis der dich davon abgehalten hat ein Paar Stücke mit einzubeziehen?

.. auch dir Erfolg mit deinem Fonds :-))

Antwort auf Beitrag Nr.: 43.012.864 von Freizeitspekulant am 07.04.12 14:48:32bei den us firmen gefallen mir

1. die hohe volatitltät

2. die hohe liquitität auch bei kleinen buden

3. die moegliche hohe bewertung

probleme habe ich

1. mit der teilweisen dreisten bewertung

2. mit der andauernden verwässerung

3. mit den hohen verwaltungskoste/gehältern

schade finde ich dass europ. biotech forschungsunternehmen so gemieden werden, nur weil bei der geringen anzahl die grossen verlierer so leicht auffallen

1. die hohe volatitltät

2. die hohe liquitität auch bei kleinen buden

3. die moegliche hohe bewertung

probleme habe ich

1. mit der teilweisen dreisten bewertung

2. mit der andauernden verwässerung

3. mit den hohen verwaltungskoste/gehältern

schade finde ich dass europ. biotech forschungsunternehmen so gemieden werden, nur weil bei der geringen anzahl die grossen verlierer so leicht auffallen

Antwort auf Beitrag Nr.: 43.012.375 von pokemon am 07.04.12 10:12:33@pokemon

...auf deine Frage was an GTXI so spannend sei...

> einiges ...vor allem wenn du den Zusammenhang zwischen dem was an der Oberläche leicht zu sehen ist und dem etwas tiefer versteckten erkennst und nutzen kannst..

...vor allem wenn du den Zusammenhang zwischen dem was an der Oberläche leicht zu sehen ist und dem etwas tiefer versteckten erkennst und nutzen kannst..

Nachfolgend mal die Übersicht zur Pipeline von GTXI.

Am 21.02.2012 erhielt GTXI von der FDA den Bescheid seine PII-Trials mit CAPESARIS zu stoppen. Infolge dieses Bescheides fiel der Aktienpreis im Panikverkauf wie ein Stein um gut 40%.

Wichtig ist dir darüber klar zu werden daß sich der FDA-geforderte Stopp auf CAPESARIS und nicht das geringste mit den PIII-Trials zu OSTARINE zu tun hat.

Man muß wissen daß sich der vor dem Kurseinbruch erreichte Kurs um 6,5 US-$ allerdings hochgradig auf OSTARINE bezog - CAPESARIS in den PII-Trials hatte da nur geringfügig zur Kursphantasie beigetragen - wie die Analysten der CityGroup wenige Tage zuvor in ihrer Einschätzung so schon formulierten: OSTARINE sei allein 11 US-$ wert - die Restpipeline, also weitere 8 US-$.

Am Tag des Absturzes, sowie in den Folgetagen hat der zweitgrößte Anteilseigner von GTXI - ein gewisser Herr Schuler mal sein Geldbeutelchen geöffnet und satte 2.309.328 Shares zum Durchschnittspreis von 3,47 US-$ für sich und seine Familie gekauft. Der Spaß war ihm immerhin 8.132.016 US-$ wert.

Nun sollte man noch wissen daß dieser Herr Schuler keine unbekannte Person in Pharmakreisen ist - um genau zu sein war er der frühere Vorstandsvorsitzende von Abbott Laboratories...hat also sicher Ahnung von dem was er da tut

Erganzend sei noch hinzugefügt daß GTXI nun am 04.04.2012 die FDA um Wiederaufnahme der gestoppten PII-Trials mit veränderter Dosis ersucht hat.

Die FDA wird sich in den kommenden 3o Tagen ab Antragstellung dazu äußern ob eine Wiederaufnahme erfolgen kann.

Falls dies wider meines Erwartens abgelehnt werden sollte, dürfte das weitestgehend im jetzigen Kursniveau eingepreist sein - im eher positiven Fall der Wiederaufnahmezusage - auch mit eventuellen Regularien - dürfte das Kursniveau von 6 US-$ schnell wieder erreicht sein...

Das dürfte sich der Herr Schuler wohl auch gedacht haben...

...auf deine Frage was an GTXI so spannend sei...

> einiges

...vor allem wenn du den Zusammenhang zwischen dem was an der Oberläche leicht zu sehen ist und dem etwas tiefer versteckten erkennst und nutzen kannst..

...vor allem wenn du den Zusammenhang zwischen dem was an der Oberläche leicht zu sehen ist und dem etwas tiefer versteckten erkennst und nutzen kannst..Nachfolgend mal die Übersicht zur Pipeline von GTXI.

Am 21.02.2012 erhielt GTXI von der FDA den Bescheid seine PII-Trials mit CAPESARIS zu stoppen. Infolge dieses Bescheides fiel der Aktienpreis im Panikverkauf wie ein Stein um gut 40%.

Wichtig ist dir darüber klar zu werden daß sich der FDA-geforderte Stopp auf CAPESARIS und nicht das geringste mit den PIII-Trials zu OSTARINE zu tun hat.

Man muß wissen daß sich der vor dem Kurseinbruch erreichte Kurs um 6,5 US-$ allerdings hochgradig auf OSTARINE bezog - CAPESARIS in den PII-Trials hatte da nur geringfügig zur Kursphantasie beigetragen - wie die Analysten der CityGroup wenige Tage zuvor in ihrer Einschätzung so schon formulierten: OSTARINE sei allein 11 US-$ wert - die Restpipeline, also weitere 8 US-$.

Am Tag des Absturzes, sowie in den Folgetagen hat der zweitgrößte Anteilseigner von GTXI - ein gewisser Herr Schuler mal sein Geldbeutelchen geöffnet und satte 2.309.328 Shares zum Durchschnittspreis von 3,47 US-$ für sich und seine Familie gekauft. Der Spaß war ihm immerhin 8.132.016 US-$ wert.

Nun sollte man noch wissen daß dieser Herr Schuler keine unbekannte Person in Pharmakreisen ist - um genau zu sein war er der frühere Vorstandsvorsitzende von Abbott Laboratories...hat also sicher Ahnung von dem was er da tut

Erganzend sei noch hinzugefügt daß GTXI nun am 04.04.2012 die FDA um Wiederaufnahme der gestoppten PII-Trials mit veränderter Dosis ersucht hat.

Die FDA wird sich in den kommenden 3o Tagen ab Antragstellung dazu äußern ob eine Wiederaufnahme erfolgen kann.

Falls dies wider meines Erwartens abgelehnt werden sollte, dürfte das weitestgehend im jetzigen Kursniveau eingepreist sein - im eher positiven Fall der Wiederaufnahmezusage - auch mit eventuellen Regularien - dürfte das Kursniveau von 6 US-$ schnell wieder erreicht sein...

Das dürfte sich der Herr Schuler wohl auch gedacht haben...

...habe die w:o Technik nun scheinbar besiegt - und nochmal einen Chart von DVAX reingestellt.

Aus charttechnischer Sicht haben wir bei 5,03$ eine kleine Unterstützung, der nächste Widerstand liegt bei 5,50$. Sollte der überwunden werden wär der Weg bis 7,70$ frei.

Aus charttechnischer Sicht haben wir bei 5,03$ eine kleine Unterstützung, der nächste Widerstand liegt bei 5,50$. Sollte der überwunden werden wär der Weg bis 7,70$ frei.

Antwort auf Beitrag Nr.: 43.013.519 von Freizeitspekulant am 07.04.12 21:08:34...auch nachträglich der Chart von GTXI

hier gilt es die 3,90$ zu nehmen - dann wär auch schön viel Platz bis zu den 6,23$

hier gilt es die 3,90$ zu nehmen - dann wär auch schön viel Platz bis zu den 6,23$

Antwort auf Beitrag Nr.: 43.011.834 von Freizeitspekulant am 06.04.12 20:55:15Hallo

Eine kleine Position habe ich in Astex Pharma (früher Supergen) aufgebaut.

Hier scheint auch das Risiko überschaubar.

Marktcap 175 Mio.

Cash 125 Mio, jährliche Lizenzeinnahmen ca. 60 Mio.

4 Phase II Produkte, viele Pharmapartner mit Kooperationen.

Die können gar nichts tun, dann haben Sie in 5 Jahren über 400 Mio. cash.

Buchwert 2,60 $ bei Kurs 1,86 $, das ist kaum zu finden bei einem Biotechwert!

Eine kleine Position habe ich in Astex Pharma (früher Supergen) aufgebaut.

Hier scheint auch das Risiko überschaubar.

Marktcap 175 Mio.

Cash 125 Mio, jährliche Lizenzeinnahmen ca. 60 Mio.

4 Phase II Produkte, viele Pharmapartner mit Kooperationen.

Die können gar nichts tun, dann haben Sie in 5 Jahren über 400 Mio. cash.

Buchwert 2,60 $ bei Kurs 1,86 $, das ist kaum zu finden bei einem Biotechwert!

Was haltet ihr von Biodelivery?

Läuft seit längerem sehr sehr gut und stabil, sollte noch viel Potential nach oben haben

WKN : 766464

BDSI wurde übertrieben runtergeprügelt nachdem ein Phase3 kandidat nicht übrzeugen konnte .

Was die meisten übersehen ist das BDSI bereits ein Produkt(Onsolis) gegen Krebsschmerzen auf den Markt hat .

Onsolis ist bereits in USA und Kanada erhältich EU folgt nächstes Jahr ,Onsolis hat ca 200 Million dollar potential .

In kürze stehen einige News an die BDSI abheben lassen könnte

FDA Zulassung -- REMS (Risk Evaluation and Mitigation Strategies) in Dezember 2011

BEMA® Buprenorphine/Naloxone PK Daten in Dezember 2011

Partnerdeal für BEMA® Buprenorphine 1Q 2012

Die Aktie notiert fast auf Cash niveau und auf Allzeittief was BDSI äusserst attraktiv macht .

Biodelivery Science (BDSI)

Marktkap: 28 M

Cash: 22 M

Kurs: 0.95

Shares Out: 29 M...(Insider + Institutions halten knapp 15 Million zusammen)

Neue Präsentation

http://www.bdsi.com/siteres.aspx?resid=8793c1c0-fd1b-4130-a8…

http://www.dailyfinance.com/quote/nasdaq/biodelivery-science…

Key BDSI Milestones

BEMA® Buprenorphine/Naloxone for opioid dependence

–Data from 2nd PK study in December 2011 (study to ensure proper dosing and blood-levels for pivotal BE study)

–Pivotal bioequivalence study January 2012; Data March 2012

–NDA submission target 1Q 2013

BEMA® Buprenorphine for chronic pain

–Late-stage commercial partnership discussions ongoing

–Initiation of 2nd Phase 3 trial in 1H 2012

ONSOLIS® (transmucosal fentanyl) - approved/marketed product

–Launched in U.S. in October 2009 by Meda Pharmaceuticals

–Launched in Canada August 2011; EU in 2H 2012

Late stage pipeline provides an opportunity for significant growth

–BEMA® Buprenorphine/Naloxone

Pivotal bioequivalence study data March 2012; NDA target 1Q 2013

–BEMA® Buprenorphine chronic pain

Phase 3 study initiation planned for 1H 2012; NDA target 1H 2013

Läuft seit längerem sehr sehr gut und stabil, sollte noch viel Potential nach oben haben

WKN : 766464

BDSI wurde übertrieben runtergeprügelt nachdem ein Phase3 kandidat nicht übrzeugen konnte .

Was die meisten übersehen ist das BDSI bereits ein Produkt(Onsolis) gegen Krebsschmerzen auf den Markt hat .

Onsolis ist bereits in USA und Kanada erhältich EU folgt nächstes Jahr ,Onsolis hat ca 200 Million dollar potential .

In kürze stehen einige News an die BDSI abheben lassen könnte

FDA Zulassung -- REMS (Risk Evaluation and Mitigation Strategies) in Dezember 2011

BEMA® Buprenorphine/Naloxone PK Daten in Dezember 2011

Partnerdeal für BEMA® Buprenorphine 1Q 2012

Die Aktie notiert fast auf Cash niveau und auf Allzeittief was BDSI äusserst attraktiv macht .

Biodelivery Science (BDSI)

Marktkap: 28 M

Cash: 22 M

Kurs: 0.95

Shares Out: 29 M...(Insider + Institutions halten knapp 15 Million zusammen)

Neue Präsentation

http://www.bdsi.com/siteres.aspx?resid=8793c1c0-fd1b-4130-a8…

http://www.dailyfinance.com/quote/nasdaq/biodelivery-science…

Key BDSI Milestones

BEMA® Buprenorphine/Naloxone for opioid dependence

–Data from 2nd PK study in December 2011 (study to ensure proper dosing and blood-levels for pivotal BE study)

–Pivotal bioequivalence study January 2012; Data March 2012

–NDA submission target 1Q 2013

BEMA® Buprenorphine for chronic pain

–Late-stage commercial partnership discussions ongoing

–Initiation of 2nd Phase 3 trial in 1H 2012

ONSOLIS® (transmucosal fentanyl) - approved/marketed product

–Launched in U.S. in October 2009 by Meda Pharmaceuticals

–Launched in Canada August 2011; EU in 2H 2012

Late stage pipeline provides an opportunity for significant growth

–BEMA® Buprenorphine/Naloxone

Pivotal bioequivalence study data March 2012; NDA target 1Q 2013

–BEMA® Buprenorphine chronic pain

Phase 3 study initiation planned for 1H 2012; NDA target 1H 2013

Antwort auf Beitrag Nr.: 43.014.383 von Wohnwunsch am 08.04.12 15:51:59Hi

Warum Allzeittief, 52 Wochentief war 0,77 $, aktuell 2,62 $,

Buchwert ist 0,14 $, haben wohl auch noch ein paar Verbindlichkeiten,

Cash 10,5 Mio, Nettoeinkommen - 25 Mio.

Habe nur grob geschaut, aber ganz richtig sind Deine Angaben wohl nicht.

Warum Allzeittief, 52 Wochentief war 0,77 $, aktuell 2,62 $,

Buchwert ist 0,14 $, haben wohl auch noch ein paar Verbindlichkeiten,

Cash 10,5 Mio, Nettoeinkommen - 25 Mio.

Habe nur grob geschaut, aber ganz richtig sind Deine Angaben wohl nicht.

Mein Post war etwas älter, du hast recht... Sorry

Meinungen zu der Aktie würden mich trotz allem interessieren

Meinungen zu der Aktie würden mich trotz allem interessieren

Antwort auf Beitrag Nr.: 43.012.744 von Freizeitspekulant am 07.04.12 13:29:18Ich will meinen senf zu der hoffnungslos überbewertete Aktie DVAX geben .

DVAX hat mit Heplisav ein vaccine für die behandlung von Hepatitis B entwickelt ,das problem ist das Hepatitis B im gegensatz zu Hepatitis C ein sehr kleiner Markt von nur rund 1.2 Mrd $ ist .

Heplisav mag besser sein als Engerix-B das problem ist das Engerix-B selbst ein rohrkrepierer für Glaxo ist .Der Jahresumsatz war gerade mal 250 Mil$ in 2010 (s.link) solche Zahlen gelten als Flop für Big Pharmas deshalb kann man das mit der Übernahme order Verpartnerung durch/mit GSK getrost vergessen .

http://media.mmm-online.com/documents/26/therapeuticfocus_63…

Die Marktkap von DVAX beträgt aktuell 802 Mil$ was übertrieben teuer ist erst recht wenn man sich die sehr schwache pipeline anschaut .Die restlichen 4 Produkte befinden sich gerade mal in Phase 1 .

Die Aktie wird nur wegen der bevorstehenden Zulassungsanträge hochgepusht und hat rein gar nichts mit der realen bewertung zu tun ein ähnliches beispiel dafür ist KERX das vor den Phase 3 daten genauso in die höhe getrieben wurde nur um danach geschlachtet zu werden .

Das Rückschlagpotential is brutal jede kleine schlechte news würde zum disaster erst recht wenn FDA hepli blocken sollte selbst wenn DVAV die Zulassung erhält ist die Aktie massivst überbewertet das erklärt auch die rekordzahl von über 17 mil aktien short .

Ich würde die Aktie nicht mal der Zange anfassen .

DVAX hat mit Heplisav ein vaccine für die behandlung von Hepatitis B entwickelt ,das problem ist das Hepatitis B im gegensatz zu Hepatitis C ein sehr kleiner Markt von nur rund 1.2 Mrd $ ist .

Heplisav mag besser sein als Engerix-B das problem ist das Engerix-B selbst ein rohrkrepierer für Glaxo ist .Der Jahresumsatz war gerade mal 250 Mil$ in 2010 (s.link) solche Zahlen gelten als Flop für Big Pharmas deshalb kann man das mit der Übernahme order Verpartnerung durch/mit GSK getrost vergessen .

http://media.mmm-online.com/documents/26/therapeuticfocus_63…

Die Marktkap von DVAX beträgt aktuell 802 Mil$ was übertrieben teuer ist erst recht wenn man sich die sehr schwache pipeline anschaut .Die restlichen 4 Produkte befinden sich gerade mal in Phase 1 .

Die Aktie wird nur wegen der bevorstehenden Zulassungsanträge hochgepusht und hat rein gar nichts mit der realen bewertung zu tun ein ähnliches beispiel dafür ist KERX das vor den Phase 3 daten genauso in die höhe getrieben wurde nur um danach geschlachtet zu werden .

Das Rückschlagpotential is brutal jede kleine schlechte news würde zum disaster erst recht wenn FDA hepli blocken sollte selbst wenn DVAV die Zulassung erhält ist die Aktie massivst überbewertet das erklärt auch die rekordzahl von über 17 mil aktien short .

Ich würde die Aktie nicht mal der Zange anfassen .

Antwort auf Beitrag Nr.: 43.014.347 von Kopflaus am 08.04.12 15:14:20@Kopflaus

servus und schöne Ostern

Hab mir deine Zahlen mal angeschaut - in 2011 hatte ASTX laut Jahresbericht vom 15.03.2012 ca. 60 Mio an Revenues - allerdings auch Gesamtausgaben von ca. 64 Mio.

...also mit nix tun wird es wohl nicht reichen in den nächsten fünf Jahren auf 400 Mio Cash zu kommen wie du sagtest...

Von wo ist deine Info daß ASTX aktuell über 125 Mio Cash verfügen soll?

servus und schöne Ostern

Hab mir deine Zahlen mal angeschaut - in 2011 hatte ASTX laut Jahresbericht vom 15.03.2012 ca. 60 Mio an Revenues - allerdings auch Gesamtausgaben von ca. 64 Mio.

...also mit nix tun wird es wohl nicht reichen in den nächsten fünf Jahren auf 400 Mio Cash zu kommen wie du sagtest...

Von wo ist deine Info daß ASTX aktuell über 125 Mio Cash verfügen soll?

Antwort auf Beitrag Nr.: 43.014.383 von Wohnwunsch am 08.04.12 15:51:59@ Wohnwunsch

irgendwie hast du da was versäumt...BDSI steht bei 2,62

trotzdem schöne Ostern...

irgendwie hast du da was versäumt...BDSI steht bei 2,62

trotzdem schöne Ostern...

Antwort auf Beitrag Nr.: 43.014.602 von Biohero am 08.04.12 18:45:47@biohero

..mußt sie ja nicht mit der Zange anfassen..es gibt nicht mal Kaufzwang

..aber vielleicht hast du ja einen Tipp für mich was ich mit meiner Kohle kaufen soll wenn ich DVAX für gut zweistellig verkauft habe

..so nach und nach werden die Shorties der 17 Mio. Shares schon dafür sorgen daß wir hier zweistellig werden. Einer jagt dann den anderen...

..mußt sie ja nicht mit der Zange anfassen..es gibt nicht mal Kaufzwang

..aber vielleicht hast du ja einen Tipp für mich was ich mit meiner Kohle kaufen soll wenn ich DVAX für gut zweistellig verkauft habe

..so nach und nach werden die Shorties der 17 Mio. Shares schon dafür sorgen daß wir hier zweistellig werden. Einer jagt dann den anderen...

Antwort auf Beitrag Nr.: 43.014.602 von Biohero am 08.04.12 18:45:47Der "Markt" für Hep-B-Vaccination ist also deiner Meinung nach nur sehr klein..soso..

Dann sag doch mal konkret was a: sehr klein ist... und b: wie groß der große Markt für Hep-C-Vaccination ist...

Ein "Markt" ist eigentlich überhaupt keine Aussage zum Thema Hep-C, da hier jeglicher Erfahrungsansatz fehlt. Zu sagen es wird eine Menge X mit etwas vacciniert was noch nicht mal fertig in den Regalen von Ärzten und Apothekern liegt - geschweige denn noch niemand konkret sagen kann wie hoch die Kosten der Vaccination for HEP-C sein werden ist nur reine Spekulation - und das weist du genau...

Anders gestaltet es sich bei HEP-A, Hep-B oder die Combi. Hier gibt es klare Zahlen über die Anwendungshäufigkeit sowie die damit verbundenen Kosten - folglich auch für einen Markt..

Das nenne ich einen Markt der nachweisbar vorhanden ist.

Mir sind die Zahlen zur Menge an HEP-B, sowie HEP-C-Häufigkeit/Verbreitung durchaus geläufig - daher frage ich mich wie du die HEP-C-Vaccination im Vergleich zur HEP-B-Vaccination als "sehr großen" Markt bezeichnen kannst ohne Zahlen zu nennen...

Mein Vorschlag dazu: komm doch mal konkret mit den Zahlen hierzu rüber und stell sie uns hier ein...interessiert hier sicher viele...mich besonders..

Freue mich immer über eine angeregte Diskussion

Dann sag doch mal konkret was a: sehr klein ist... und b: wie groß der große Markt für Hep-C-Vaccination ist...

Ein "Markt" ist eigentlich überhaupt keine Aussage zum Thema Hep-C, da hier jeglicher Erfahrungsansatz fehlt. Zu sagen es wird eine Menge X mit etwas vacciniert was noch nicht mal fertig in den Regalen von Ärzten und Apothekern liegt - geschweige denn noch niemand konkret sagen kann wie hoch die Kosten der Vaccination for HEP-C sein werden ist nur reine Spekulation - und das weist du genau...

Anders gestaltet es sich bei HEP-A, Hep-B oder die Combi. Hier gibt es klare Zahlen über die Anwendungshäufigkeit sowie die damit verbundenen Kosten - folglich auch für einen Markt..

Das nenne ich einen Markt der nachweisbar vorhanden ist.

Mir sind die Zahlen zur Menge an HEP-B, sowie HEP-C-Häufigkeit/Verbreitung durchaus geläufig - daher frage ich mich wie du die HEP-C-Vaccination im Vergleich zur HEP-B-Vaccination als "sehr großen" Markt bezeichnen kannst ohne Zahlen zu nennen...

Mein Vorschlag dazu: komm doch mal konkret mit den Zahlen hierzu rüber und stell sie uns hier ein...interessiert hier sicher viele...mich besonders..

Freue mich immer über eine angeregte Diskussion

Antwort auf Beitrag Nr.: 43.014.611 von Freizeitspekulant am 08.04.12 18:53:57Unter anderem von hier

http://seekingalpha.com/article/320652-astex-pharmaceuticals…

Also genau sogar 128,4 Mio. cash,

Lizenzeinnahmen 2011 waren 61,4 Mio.

wobei jährliche Steigerungsraten zu verzeichnen sind.

Die Ausgaben von 64 Mio. waren für Forschung und Entwicklung

um die Pipeline voranzubringen, es wird also kein Geld verbrannt.

Das heist, wenn dieser Bereich eingestellt würde,

hätten Sie jedes Jahr Einnahmen von 61,4 Mio. mit minimalen Ausgaben.

Frage: würdest Du wenn 300 Mio. vorhanden wären eine Firma kaufen die

128 Mio. auf der Bank hat und jedes Jahr 60 Mio. dazukommen kaufen?

Denke das wäre schon nach 5 Jahren ein super Geschäft.

Die Pipeline schreiben wir einfach mal auf 0 ab.

Marktcap der Firma wie gesagt 173 Mio.

Meiner Meinung nach braucht es da nur etwas Geduld.

Schauen wir in einem Jahr nochmal!!

http://seekingalpha.com/article/320652-astex-pharmaceuticals…

Also genau sogar 128,4 Mio. cash,

Lizenzeinnahmen 2011 waren 61,4 Mio.

wobei jährliche Steigerungsraten zu verzeichnen sind.

Die Ausgaben von 64 Mio. waren für Forschung und Entwicklung

um die Pipeline voranzubringen, es wird also kein Geld verbrannt.

Das heist, wenn dieser Bereich eingestellt würde,

hätten Sie jedes Jahr Einnahmen von 61,4 Mio. mit minimalen Ausgaben.

Frage: würdest Du wenn 300 Mio. vorhanden wären eine Firma kaufen die

128 Mio. auf der Bank hat und jedes Jahr 60 Mio. dazukommen kaufen?

Denke das wäre schon nach 5 Jahren ein super Geschäft.

Die Pipeline schreiben wir einfach mal auf 0 ab.

Marktcap der Firma wie gesagt 173 Mio.

Meiner Meinung nach braucht es da nur etwas Geduld.

Schauen wir in einem Jahr nochmal!!

Super Idee - die diskusion!

Vielen Dank für die interessanten Werte und Einblicke.

Investments in Biotech sind ja immer sehr spekulativ. Von daher ist ein Depot mit mehreren Werten m.E. der richtige Weg. Ich maße mir nicht an, den Erfolg oder Misserfolg korrekt einschätzen zu können. Auch Mediziner und Analysten können das ja kaum. Versuche aber das Risiko für mich zu minimieren.

Deshalb achte ich vor allem auf folgende Faktoren

1. Breite Pipeline - ein Flopp ist dann noch kein Vollflop

2. Verpartnerte Programme möglichst an große Player - die werden schon wissen in was sie da investieren (ähm - möchte man zumindest meinen) und können es dann auch verkaufen

3. Attraktive Bewertung/Marktkapitalisierung - es muss halt noch Potenzial da sein

4. Schön ist natürlich immer wenn das Wort blockbuster auftaucht - is klar

Natürlich spielen noch weitere Faktoren wie Cashposition, %-Royalties, Schulden, Kostenkontrolle, newsflow etc. eine Rolle.

Zur Zeit habe ich LGND, ARRY, Astex, Dyax und Paion im Depot:

LGND habe ich schon länger, weil da eigentlich alles zusammenpasst. Dazu hab ich in der entsprechenden Diskussion schon viel geschrieben. Ergänzend vielleicht noch, dass auch LGND ein SARM für Muskelwachstum in der Entwicklung hat. Soll laut LGND natürlich das bessere Profil haben jedoch schaffen die es irgendwie nicht einen Parner zu finden!? Dachte übrigens das von GTX wäre an Merck verpartnert und gefloppt?

ARRY hat alleine 7 verpartnerte Programme in P II darunter Partner wie Amgen, Astra Zeneca, Novartis, Roche, Eli Lilly und das ist längst nicht alles...

Astex wurde hier ja schon vorgestellt. Was mich hier reizt sind die 60 Mio Royalties. Leider haben die ihre Kosten nicht so im Griff wie ich mir das wünschen würde.

Dyax ist vergleichbar mit Morphosys. Hat viele Partnerschaften (17) mit Big Pharma aber auch ein Medikament in eigener Regie am Markt. Und ist dafür einfach viel zu günstig bewertet.

Paion hatte ich mir mal gekauft, weil die nur mit 20 Mio bewertet wurden und ich das bei einer sicher anstehenden verpartnerten P III für Desmopteplase für viel zu billig hielt. Mittlerweile ist da ja einiges passiert. War hier aber Gott sei Dank so schlau durch Gewinnmitnahme aus dem Risiko zu gehen und kann hier also ganz beruhigt mit meiner Restposition abwarten. Empfehlen würde ich Paion aktuell nicht.

Das wäre im Übrigen auch eine Strategie, die ich empfehlen kann. Wenn ein Wert gut gelaufen ist ruhig mal Gewinne mitnehmen und aus dem Risiko gehen.

An europäischen Werten fällt mir noch Morphosys ein, die ich auf der watch habe, da breite Pipeline etc. aber auch Übernahmekandidat.

So einen guten Link für alle biotech interessierten habe ich noch:

http://www.nektar.com/pdf/RD_Directions_MARCH08Edition.pdf

Ist zwar schon ein bischen älter aber doch interessant, wie ich finde.

Vielen Dank für die interessanten Werte und Einblicke.

Investments in Biotech sind ja immer sehr spekulativ. Von daher ist ein Depot mit mehreren Werten m.E. der richtige Weg. Ich maße mir nicht an, den Erfolg oder Misserfolg korrekt einschätzen zu können. Auch Mediziner und Analysten können das ja kaum. Versuche aber das Risiko für mich zu minimieren.

Deshalb achte ich vor allem auf folgende Faktoren

1. Breite Pipeline - ein Flopp ist dann noch kein Vollflop

2. Verpartnerte Programme möglichst an große Player - die werden schon wissen in was sie da investieren (ähm - möchte man zumindest meinen) und können es dann auch verkaufen

3. Attraktive Bewertung/Marktkapitalisierung - es muss halt noch Potenzial da sein

4. Schön ist natürlich immer wenn das Wort blockbuster auftaucht - is klar

Natürlich spielen noch weitere Faktoren wie Cashposition, %-Royalties, Schulden, Kostenkontrolle, newsflow etc. eine Rolle.

Zur Zeit habe ich LGND, ARRY, Astex, Dyax und Paion im Depot:

LGND habe ich schon länger, weil da eigentlich alles zusammenpasst. Dazu hab ich in der entsprechenden Diskussion schon viel geschrieben. Ergänzend vielleicht noch, dass auch LGND ein SARM für Muskelwachstum in der Entwicklung hat. Soll laut LGND natürlich das bessere Profil haben jedoch schaffen die es irgendwie nicht einen Parner zu finden!? Dachte übrigens das von GTX wäre an Merck verpartnert und gefloppt?

ARRY hat alleine 7 verpartnerte Programme in P II darunter Partner wie Amgen, Astra Zeneca, Novartis, Roche, Eli Lilly und das ist längst nicht alles...

Astex wurde hier ja schon vorgestellt. Was mich hier reizt sind die 60 Mio Royalties. Leider haben die ihre Kosten nicht so im Griff wie ich mir das wünschen würde.

Dyax ist vergleichbar mit Morphosys. Hat viele Partnerschaften (17) mit Big Pharma aber auch ein Medikament in eigener Regie am Markt. Und ist dafür einfach viel zu günstig bewertet.

Paion hatte ich mir mal gekauft, weil die nur mit 20 Mio bewertet wurden und ich das bei einer sicher anstehenden verpartnerten P III für Desmopteplase für viel zu billig hielt. Mittlerweile ist da ja einiges passiert. War hier aber Gott sei Dank so schlau durch Gewinnmitnahme aus dem Risiko zu gehen und kann hier also ganz beruhigt mit meiner Restposition abwarten. Empfehlen würde ich Paion aktuell nicht.

Das wäre im Übrigen auch eine Strategie, die ich empfehlen kann. Wenn ein Wert gut gelaufen ist ruhig mal Gewinne mitnehmen und aus dem Risiko gehen.

An europäischen Werten fällt mir noch Morphosys ein, die ich auf der watch habe, da breite Pipeline etc. aber auch Übernahmekandidat.

So einen guten Link für alle biotech interessierten habe ich noch:

http://www.nektar.com/pdf/RD_Directions_MARCH08Edition.pdf

Ist zwar schon ein bischen älter aber doch interessant, wie ich finde.

@kmastra

Moin - mit LGND und ARRY hast zwei gut aufgestellte Firmen im Depot, die ich immer wieder mal kurz betrachte...mir dann auch schon mal vorgenommen hab ein paar erste Stücke zu sichern (vor allem von ARRY). Dann hab ich sie aber doch wieder auf meine Watchlist verschoben...irgendwann kralle ich mir doch noch welche...

Mit DYAX hab ich mich eigentlich noch nicht weiter befaßt - daher kann ich dazu nichts sagen..für Paion konnte ich mich noch nie begeistern.

Bei GTXI hat - wie ja schon in einem Beitrag geschrieben - CAPESARIS (PII) den "Stopp" auferlegt bekommen - Von seitens der FDA erfolgt in den kommenden 30 Tagen ab Antragstellung auf "Wiederaufnahme" ein Bescheid.

Das dürfte nach der massiven Kurskorrektur als erstes "Zugpferd" für die "Kursgenesung" sorgen - dabei aber nicht vergessen daß das eigentliche Ass im Ärmel von GTXI OSTARINE in PIII ist

Zu meine Horizon Pharma-Anteilen (HZNP) stell ich heute noch ein paar Eckdaten rein - soviel schon mal jetzt - Zugpferd hier LODOTRA in PIII

mit PDUFA-Termin am 26.07.2012

Moin - mit LGND und ARRY hast zwei gut aufgestellte Firmen im Depot, die ich immer wieder mal kurz betrachte...mir dann auch schon mal vorgenommen hab ein paar erste Stücke zu sichern (vor allem von ARRY). Dann hab ich sie aber doch wieder auf meine Watchlist verschoben...irgendwann kralle ich mir doch noch welche...

Mit DYAX hab ich mich eigentlich noch nicht weiter befaßt - daher kann ich dazu nichts sagen..für Paion konnte ich mich noch nie begeistern.

Bei GTXI hat - wie ja schon in einem Beitrag geschrieben - CAPESARIS (PII) den "Stopp" auferlegt bekommen - Von seitens der FDA erfolgt in den kommenden 30 Tagen ab Antragstellung auf "Wiederaufnahme" ein Bescheid.

Das dürfte nach der massiven Kurskorrektur als erstes "Zugpferd" für die "Kursgenesung" sorgen - dabei aber nicht vergessen daß das eigentliche Ass im Ärmel von GTXI OSTARINE in PIII ist

Zu meine Horizon Pharma-Anteilen (HZNP) stell ich heute noch ein paar Eckdaten rein - soviel schon mal jetzt - Zugpferd hier LODOTRA in PIII

mit PDUFA-Termin am 26.07.2012

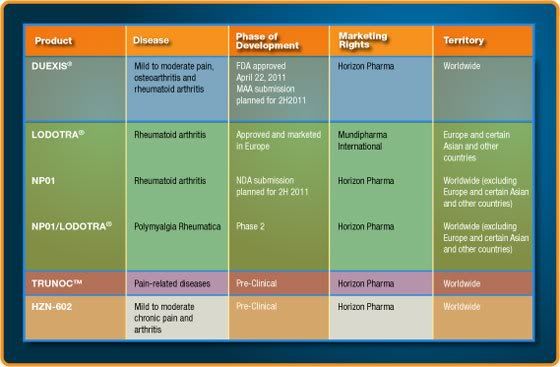

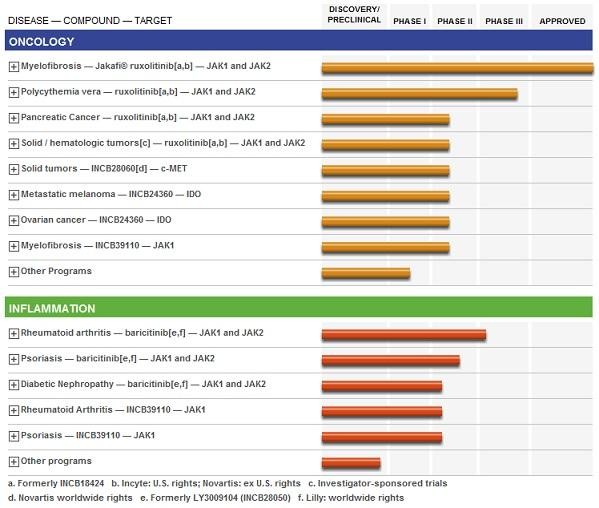

Antwort auf Beitrag Nr.: 43.015.085 von Freizeitspekulant am 09.04.12 09:35:20…wie also schon angedroht mal noch ein paar Eckdaten zu Horizon Pharma ( HZNP)

Das Unternehmen hatte im August letzten Jahres sein IPO, danach wurde der Wert deftig nach unten geprügelt . Eine Bodenbildung, sowie erste Anzeichen dafür daß der Kurs nun wieder gen Norden laufen dürfte ist im angehängten Chart erkennbar.

Nachdem man mit DUEXIS seine erste Product-Launch erreichen konnte steht nun der nächste große Termin am 26.07.2012 bevor – PDUFA von LODOTRA. Die Gesamtpipeline hab ich auch mal mit drangehängt – zur besseren Veranschaulichung.

Ende Februar hat man eine Kapitalerhöhung durchgeführt – 14 Mio. zusätzliche Shares zu 3,62 $ ausgegeben – so round about 50 Mio. US-$ eingesammelt. HZNP hat also Kapitalreserven um seine Programme durchzuziehen.

Insider und Institutionelle haben hier immer wieder mal heftig zugeschlagen und beachtliche Mengen an Anteilen gekauft . Gemäß dem Motto daß es zwar viele Gründe geben mag eigene Aktien zu verkaufen – wohl aber nur einen wenn in diesem Ausmaß eingekauft wird.

Zu beachten ist, daß die Aktie nur über einen geringen Float verfügt – daher können Preisschwankungen hier schon mitunter etwas intensiver ausfallen…natürlich in beide Richtungen!!

HZNP ist an deutschen Börsen nicht handelbar !!!

Das Unternehmen hatte im August letzten Jahres sein IPO, danach wurde der Wert deftig nach unten geprügelt . Eine Bodenbildung, sowie erste Anzeichen dafür daß der Kurs nun wieder gen Norden laufen dürfte ist im angehängten Chart erkennbar.

Nachdem man mit DUEXIS seine erste Product-Launch erreichen konnte steht nun der nächste große Termin am 26.07.2012 bevor – PDUFA von LODOTRA. Die Gesamtpipeline hab ich auch mal mit drangehängt – zur besseren Veranschaulichung.

Ende Februar hat man eine Kapitalerhöhung durchgeführt – 14 Mio. zusätzliche Shares zu 3,62 $ ausgegeben – so round about 50 Mio. US-$ eingesammelt. HZNP hat also Kapitalreserven um seine Programme durchzuziehen.

Insider und Institutionelle haben hier immer wieder mal heftig zugeschlagen und beachtliche Mengen an Anteilen gekauft . Gemäß dem Motto daß es zwar viele Gründe geben mag eigene Aktien zu verkaufen – wohl aber nur einen wenn in diesem Ausmaß eingekauft wird.