Deutsche Small Caps - Basisinvestments eines Langfristdepots (Seite 5797)

eröffnet am 18.12.04 19:37:36 von

neuester Beitrag 23.05.24 08:46:49 von

neuester Beitrag 23.05.24 08:46:49 von

Beiträge: 69.791

ID: 937.146

ID: 937.146

Aufrufe heute: 334

Gesamt: 12.716.775

Gesamt: 12.716.775

Aktive User: 12

Top-Diskussionen

| Titel | letzter Beitrag | Aufrufe |

|---|---|---|

| vor 5 Minuten | 1298 | |

| vor 25 Minuten | 1215 | |

| vor 30 Minuten | 992 | |

| gestern 21:23 | 689 | |

| gestern 23:17 | 658 | |

| vor 1 Stunde | 601 | |

| vor 9 Minuten | 416 | |

| vor 15 Minuten | 396 |

Meistdiskutierte Wertpapiere

| Platz | vorher | Wertpapier | Kurs | Perf. % | Anzahl | ||

|---|---|---|---|---|---|---|---|

| 1. | 1. | 18.704,09 | +0,28 | 92 | |||

| 2. | 2. | 10,240 | -0,58 | 72 | |||

| 3. | 4. | 166,92 | +0,22 | 54 | |||

| 4. | 6. | 15,036 | +3,53 | 50 | |||

| 5. | 5. | 6,3920 | +0,50 | 50 | |||

| 6. | 7. | 92,60 | -1,96 | 48 | |||

| 7. | 3. | 9,5750 | +0,95 | 43 | |||

| 8. | 8. | 2.364,42 | -0,61 | 39 |

Beitrag zu dieser Diskussion schreiben

Antwort auf Beitrag Nr.: 48.757.808 von katjuscha-research am 12.01.15 22:27:45Hi Katjuscha. du suchst doch immer günstige Aktien. ist da in Deutschland eigentlich nicht VW mittlerweile am günstigsten. viel Cash und ein grosser Profiteur von der Euro Schwäche plus guter Dividende. allein der Euro müsste 20 % Gewinnsteigerung bringen.

Antwort auf Beitrag Nr.: 48.749.408 von trustone am 12.01.15 07:36:11

Das klingt wirklich wunderbar.

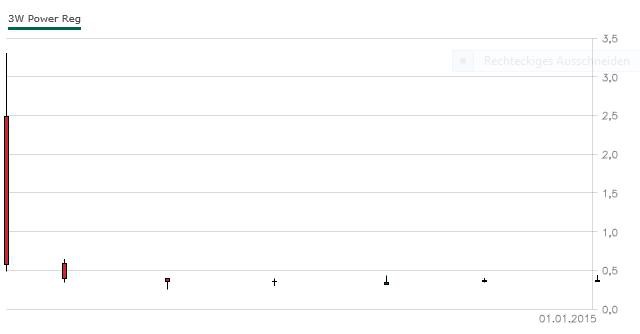

Im Dreijahreschart von WO sehe ich leider keinen einzigen Versuch, das letzte Verkaufssignal bei 50 Cent auch nur zu berühren.

Gibt es noch einen anderen detaillierteren Chart ? Oder hat tatsächlich noch niemand die positiven Aussichten wahrgenommen und gekauft ?

Zitat von wiener9: in 2012 z.b machte ein Fonds ein Übernahmeangebot für die 3W Power,

man wollte damals rund 200 Mio für die Firma bezahlen, heute notiert die 3W also um einen Bruchteil davon an der Börse, (die Übernahme kam damals aus ofiziell Formalfehlern nicht zustande)

http://www.aktiencheck.de/analysen/Artikel-3W_Power_Uebernah…

und genauch auch daraus besteht ein weiter möglicher Hebel aus meiner Sicht,

dieses neue Management hat das auch schon bei Elexis usw. gemacht/geschafft

erst Sanieren, den Wert für die Aktionäre steigern und dann das Unternehmen zu deutlich höheren Kursen von einem Mitbewerber übernehmen lassen,

3W Power hat in einigen Bereichen ordentliche Marktanteile und sehr langfristige Verträge mit großen Kunden, auch hier ist mein Ansatz folgender,

die Firma könnte in 1-2 Jahren zu diesen Schnäppchen Preisen längst übernommen worden sein oder sich der Kurs eben nach oben angepasst haben,

ich sah die Chance als ich die Position bei einem Kurs von etwa 0,36 einging eben deutlich höher dass sich der Kurs eher verdoppeln würde als vielleicht nochmals 50% zu fallen,

und dass man anstatt in mein wikifolio direkt in 3W Power investieren sollte ist reine Ansichtssache, ich habe ja auch aktuell 3 Werte im Depot und nicht nur 3W,(macht diese Aussage ja schon mal obsolet) auch habe ich nur einen Bruchteil meiner Performance im wikifolio mit 3W Power erzielt, der Rest kam und kommt mit andere Werten zustande,

Das klingt wirklich wunderbar.

Im Dreijahreschart von WO sehe ich leider keinen einzigen Versuch, das letzte Verkaufssignal bei 50 Cent auch nur zu berühren.

Gibt es noch einen anderen detaillierteren Chart ? Oder hat tatsächlich noch niemand die positiven Aussichten wahrgenommen und gekauft ?

Antwort auf Beitrag Nr.: 48.756.704 von HK12 am 12.01.15 20:28:13okay, aber selbst bei diesen 16% Umsatzanstieg und 33% Gewinnanstieg in 2015 und 2016 hätte man bei 19 € erst für 2016 ein KGV von 18-20.

das heißt, dieses starke Wachstum preist man bei 19 € bereits ein. 25-30% Kurschance bis 2016, und auch nur dann wenn die H&A Schätzungen stimmen?

weiß nich, ...

das heißt, dieses starke Wachstum preist man bei 19 € bereits ein. 25-30% Kurschance bis 2016, und auch nur dann wenn die H&A Schätzungen stimmen?

weiß nich, ...

Antwort auf Beitrag Nr.: 48.747.554 von Kleiner Chef am 11.01.15 17:21:08

kann das irgendwer in verständliche deutsche Worte zusammen fassen?

Zitat von Kleiner Chef: Prodware and its 47% BV growth rate selling for 6.5x earnings and 70% of book, why?

I received a text recently from Dave Waters saying he was convinced France is the best place in the developed world for a value investor to hunt for bargains. Armed with a screener I went to work to proving his point. I ran a number of screens on France looking for companies trading below book value with high returns on equity, and what I've found has been interested. Interesting enough that I'd wholeheartedly agree with his statement. If you feel the well is dry in terms of investment ideas I'd recommend looking at France.

One French company that appeared in my screening result was Prodware (ALPRO.France) an IT integrator that was founded in 1989 and is listed in Paris. The company has three main business segments, business solutions, network and security solutions and integration solutions. Their business solutions division creates custom software solutions as well as proprietary solutions that they resell to clients. Network and integration solutions are implementation experts, they build networks or integrated disparate systems.

Prodware is a fairly large company with 1,500 employees spread across Europe, Africa and the Middle East. They're the leading Microsoft partner in EMEA with over 20,000 clients. The company has no operations in the US, but that's not an issue as the US IT consulting market is already saturated.

Technical consulting is a very straight-forward business model. A consulting company places a consultant at a client and bills them out at an hourly rate. The consulting company takes a large cut and pays the remainder to the consultant. As long as a consultant is billing a client both the employee and consulting company are earning money. If a client cancels a contract often a consulting company will let the employee go saving the ongoing expense.

The company screened well, it is trading for about 70% of book value and 6.5x earnings. They earned about 9% on their equity in 2013. They've had returns as high as 30% in 2004, and recently 21% in 2011. On the basis of the company's initial stats alone this had the making of a great investment. It's not often that 'good' companies trade for such a discount.

If the company's current stats weren't impressive enough then one could look at their growth. The company had €2m in equity in 2004, and in the last ten years has grown it to €95.5m for a annual growth rate of 47% a year. They've grown revenue from €22m in 2005 to €176m in 2013, an eight fold increase in the past nine years. The company's net income also followed a similar path, from almost nothing in 2005 to €7.7m in 2013.

A picture of the company's revenue is shown below:

Everything about this company seemed great when I first start to research them, their valuation, their growth, the modest executive income. Prodware seemed like a slam dunk investment. Unfortunately the veneer fell off quickly.

Prodware the company itself has a great growth story, unfortunately for investors it's a different situation. The company has financed itself in the past with convertible bonds and share issuance. At the end of 2013 they had €7m in convertible bonds outstanding, which converted would result in 798k shares being issued. This is on top of the 2m shares issued since 2011. If one looks at their equity statement it becomes clear that issuing shares isn't a one-off event, but rather something that happens yearly.

Here's a picture of the share issuance, and potential dilution from their bonds since 2012:

Many growth companies continually re-invest for more growth, Prodware is no different. The company earned €7.7m in 2013 but generated €22m in operating cash flow. They then spent €21m on software and development costs. This should result in the company having free cash flow of €1m, except that they had debt coming due which was paid off with equity issuance. This seems to be common from what I've seen. The company generates considerable cash, but then consumes all of the cash generated for re-investment. They're left in a situation where they can't pay their financing costs and have been issuing shares.

Investors are continually being diluted by management's financing decisions. Cost control on projects appears non-existent with shortfalls being made up via equity issuance. If management were able to reign in costs and repay debt out of cash flow shareholders would be duly rewarded. For example, if the company hadn't issued shares in 2012 and 2013 their 2013 EPS would have been €1.66 per share instead of €1.09 per share. While shareholders pat their backs for the company's €1.09 in earnings they could have had 50% more if management hadn't been issuing shares. In 2006 the company had 2.8m shares outstanding, as of their last fiscal year they had 7.3m shares outstanding, and 8.4m fully diluted shares.

In 2006 the company earned €14.47 per share in revenue on a gross €46m in revenue. In 2013 the company's per share revenue was €24.30 against €176m in revenue. Revenue increased 3.8x, but on a per share basis it didn't even double. It might seem like I'm overstating the company's dilution, but to investors who are purchasing shares on an open market this is the biggest issue facing the company. If the company's revenue and earnings triple, but the company dilutes shareholders it's possible they might not see any of the gains.

The ultimate endgame for a company like Prodware is unknown, but I believe we have some hints. One of their largest investors is a venture capital firm, and venture capital loves growth. The company has been growing like a weed, and at some point maybe they'll sell out to a larger consulting firm. The venture capital backers and executives will probably do well for themselves, how shareholders will do is unknown. It seems the longer it takes for the company to sell the more shareholders will be diluted. Even though the company is experiencing great growth it's unlikely that shareholders will get to e

http://www.oddballstocks.com/2014/08/prodware-and-its-47-bv-…

kann das irgendwer in verständliche deutsche Worte zusammen fassen?

Antwort auf Beitrag Nr.: 48.755.888 von Kleiner Chef am 12.01.15 19:05:17ich vermute das die US-Tochter Aspera Aufträge bekommen hat..

Die Analysten von Hauck & Aufhäuser sagen für 2014 bis 2016 einen durchschnittlichen Umsatzanstieg von 16 Prozent voraus, der Gewinn soll sogar jährlich um etwa 33 Prozent vorankommen. Der überproportionale Ergebnisanstieg basiert auf dem Ausbau des margenstarken Produktgeschäfts.

Hauck & Aufhäuser sieht den fairen Wert der Aktie bei 16,50 Euro..

Erhöhung der Dividende steht auch noch im Raum..

Die Analysten von Hauck & Aufhäuser sagen für 2014 bis 2016 einen durchschnittlichen Umsatzanstieg von 16 Prozent voraus, der Gewinn soll sogar jährlich um etwa 33 Prozent vorankommen. Der überproportionale Ergebnisanstieg basiert auf dem Ausbau des margenstarken Produktgeschäfts.

Hauck & Aufhäuser sieht den fairen Wert der Aktie bei 16,50 Euro..

Erhöhung der Dividende steht auch noch im Raum..

Zitat von Kleiner Chef:Zitat von katjuscha-research: Was stand zu USU denn im Aktionär? Gabs da was genaueres?

Auf den ersten Blick ja mit dem 20fachen Ebit recht teuer, und dazu kurz vorm harten Widerstand bei 15-16 €. Wirkt jetzt nicht sofort sexy, aber immerhin in einem mittelfristigen, steilen Aufwärtstrend. Wenn der weiterläuft super, aber wie gesagt fundamental schon ziemlich hoch bewertet, es sei denn DerAktionär erwartet hohes Umsatzwachstum bei steigenden Margen.

Auch H. Pröbst hat in der EAS getrommelt. Tenor: Umsatz 2014 unterhalb der Erwartungen, daß Projekte in 2015 verschoben. Starkes Wachstum in den USA mit positiven Währungseffekten.

Perspektivisch werden 100 Mill. Euro angestrebt mit Verdoppelung des Ergebnisses. Ansatz: 20er KGV rechtfertigt Kursregionen von 19 Euro!.

Mein Fazit war: Die Aktie scheint nach Jahren des Stillstands tatsächlich den Wachstumsmodus anzuwerfen. Die Aktie enthält aber schon einiges an Zukunftslorbeeren.

Gruß

Trading Spotlight

Antwort auf Beitrag Nr.: 48.755.273 von katjuscha-research am 12.01.15 18:08:39

Auch H. Pröbst hat in der EAS getrommelt. Tenor: Umsatz 2014 unterhalb der Erwartungen, daß Projekte in 2015 verschoben. Starkes Wachstum in den USA mit positiven Währungseffekten.

Perspektivisch werden 100 Mill. Euro angestrebt mit Verdoppelung des Ergebnisses. Ansatz: 20er KGV rechtfertigt Kursregionen von 19 Euro!.

Mein Fazit war: Die Aktie scheint nach Jahren des Stillstands tatsächlich den Wachstumsmodus anzuwerfen. Die Aktie enthält aber schon einiges an Zukunftslorbeeren.

Gruß

USU Software mit Doppelpack am Wochenende!

Zitat von katjuscha-research: Was stand zu USU denn im Aktionär? Gabs da was genaueres?

Auf den ersten Blick ja mit dem 20fachen Ebit recht teuer, und dazu kurz vorm harten Widerstand bei 15-16 €. Wirkt jetzt nicht sofort sexy, aber immerhin in einem mittelfristigen, steilen Aufwärtstrend. Wenn der weiterläuft super, aber wie gesagt fundamental schon ziemlich hoch bewertet, es sei denn DerAktionär erwartet hohes Umsatzwachstum bei steigenden Margen.

Auch H. Pröbst hat in der EAS getrommelt. Tenor: Umsatz 2014 unterhalb der Erwartungen, daß Projekte in 2015 verschoben. Starkes Wachstum in den USA mit positiven Währungseffekten.

Perspektivisch werden 100 Mill. Euro angestrebt mit Verdoppelung des Ergebnisses. Ansatz: 20er KGV rechtfertigt Kursregionen von 19 Euro!.

Mein Fazit war: Die Aktie scheint nach Jahren des Stillstands tatsächlich den Wachstumsmodus anzuwerfen. Die Aktie enthält aber schon einiges an Zukunftslorbeeren.

Gruß

Antwort auf Beitrag Nr.: 48.753.389 von HK12 am 12.01.15 15:32:26Was stand zu USU denn im Aktionär? Gabs da was genaueres?

Auf den ersten Blick ja mit dem 20fachen Ebit recht teuer, und dazu kurz vorm harten Widerstand bei 15-16 €. Wirkt jetzt nicht sofort sexy, aber immerhin in einem mittelfristigen, steilen Aufwärtstrend. Wenn der weiterläuft super, aber wie gesagt fundamental schon ziemlich hoch bewertet, es sei denn DerAktionär erwartet hohes Umsatzwachstum bei steigenden Margen.

Auf den ersten Blick ja mit dem 20fachen Ebit recht teuer, und dazu kurz vorm harten Widerstand bei 15-16 €. Wirkt jetzt nicht sofort sexy, aber immerhin in einem mittelfristigen, steilen Aufwärtstrend. Wenn der weiterläuft super, aber wie gesagt fundamental schon ziemlich hoch bewertet, es sei denn DerAktionär erwartet hohes Umsatzwachstum bei steigenden Margen.

Antwort auf Beitrag Nr.: 48.754.790 von upanddown1 am 12.01.15 17:32:26

Wir haben bei 90 Dollar/Barrel von Amortisationszeiten von 10 Monaten gesprochen. Diese Zeiten sind vorbei und die sehe ich auch so schnell nicht widerkommen. Deshalb sehe ich keinen Grund in Öl- Gasstocks zu investieren.

Gruß

DRAG: Mir fehlt derzeit völlig die Fantasie in Öl/Gasstocks zu investieren!

Zitat von upanddown1: Einer meiner 2015er Favoriten.

hab gerade einen sehr ausführlichen Bericht über die Deutsche Rohstoff verfasst den Wgerade gefressen hat.. so´n Sch...

Es geht um die News, dass neue Flächen und damit neue Bohrungen im Wattenbergfeld veröffentlicht wurden..

Leider keine Zeit mehr, alles neu zu schreiben.

Zusammenfassung: Viel Cash, neue Flächen, Gewinn schon ab Ölpreis um die 40$.

http://www.goldinvest.de/index.php/deutsche-rohstoff-tochter…

und vom 22.12.14:

http://www.be24.at/blog/entry/695986/deutsche-rohstoff-ag-wi…

mehr info:

http://www.wallstreet-online.de/diskussion/1160352-11271-112…

Leider keine Info über die erwarteten Förderquoten.

Gruß

up

Wir haben bei 90 Dollar/Barrel von Amortisationszeiten von 10 Monaten gesprochen. Diese Zeiten sind vorbei und die sehe ich auch so schnell nicht widerkommen. Deshalb sehe ich keinen Grund in Öl- Gasstocks zu investieren.

Gruß

DRAG .. ein Favorit für 2015 ?

Einer meiner 2015er Favoriten.hab gerade einen sehr ausführlichen Bericht über die Deutsche Rohstoff verfasst den W

gerade gefressen hat.. so´n Sch...

gerade gefressen hat.. so´n Sch...Es geht um die News, dass neue Flächen und damit neue Bohrungen im Wattenbergfeld veröffentlicht wurden..

Leider keine Zeit mehr, alles neu zu schreiben.

Zusammenfassung: Viel Cash, neue Flächen, Gewinn schon ab Ölpreis um die 40$.

http://www.goldinvest.de/index.php/deutsche-rohstoff-tochter…

und vom 22.12.14:

http://www.be24.at/blog/entry/695986/deutsche-rohstoff-ag-wi…

mehr info:

http://www.wallstreet-online.de/diskussion/1160352-11271-112…

Leider keine Info über die erwarteten Förderquoten.

Gruß

up

Antwort auf Beitrag Nr.: 48.753.389 von HK12 am 12.01.15 15:32:26Sehr große Umsätze heute. Iceberg Order auf der Geldseite bei 14,74.

Außer Mainfirst ist noch kein Fonds beteiligt.

Außer Mainfirst ist noch kein Fonds beteiligt.