Rohstoff-Explorer: Research oder Neuvorstellung (Seite 1562)

eröffnet am 13.03.08 13:14:32 von

neuester Beitrag 07.06.24 21:08:42 von

neuester Beitrag 07.06.24 21:08:42 von

Beiträge: 29.544

ID: 1.139.490

ID: 1.139.490

Aufrufe heute: 8

Gesamt: 2.702.935

Gesamt: 2.702.935

Aktive User: 0

Top-Diskussionen

| Titel | letzter Beitrag | Aufrufe |

|---|---|---|

| vor 1 Stunde | 2913 | |

| vor 1 Stunde | 2716 | |

| vor 59 Minuten | 1582 | |

| vor 1 Stunde | 1051 | |

| heute 08:40 | 467 | |

| heute 08:56 | 463 | |

| gestern 21:59 | 454 | |

| vor 59 Minuten | 442 |

Meistdiskutierte Wertpapiere

| Platz | vorher | Wertpapier | Kurs | Perf. % | Anzahl | ||

|---|---|---|---|---|---|---|---|

| 1. | 1. | 18.445,93 | +0,34 | 309 | |||

| 2. | 2. | 27,00 | -5,13 | 153 | |||

| 3. | 3. | 157,88 | -0,65 | 95 | |||

| 4. | 6. | 9,9500 | -1,29 | 44 | |||

| 5. | 4. | 0,1321 | -0,90 | 43 | |||

| 6. | 14. | 4,1830 | +0,10 | 33 | |||

| 7. | 9. | 15,588 | +0,10 | 30 | |||

| 8. | 10. | 3,5050 | -0,14 | 26 |

Beitrag zu dieser Diskussion schreiben

weil ich mal gesagt hatte das Potash in(aus)Brasilien eine etwas spezielle Sache sein dürfte.

Viele Firmen gibt es da ja noch nicht-wenn inzwischen auch schon ein paar-, aber sowas hier sind denk ich welche die man, bei entsprechendem Interesse, in dem Zusammenhang im Blick behalten kann.

Triumph Tin - Acquisition of Brazilian Potash Project - Aug 28, 2014

+ The Company has acquired a 100% interest in the Capela Potash Project, in the Sergipe Alagoas Basin on the east coast of Brazil.

+ The Sergipe-Alagoas Basin hosts significant deposits of sylvinite +carnallitite, associated with evaporitic sub basins.

+ Vale operates the Taquari-Vassouras Potash Mine, which is the only Potash mine currently operating in Brazil, 13km to the south of the Capela Potash Project.

+ Recently completed 3D seismic has confirmed the presence of potential salt layers @relatively shallow depth, within the Capela Potash Project area.

+ The 3D seismic has also confirmed that the Capela Potash Project is the possible northern extension to Vales Taquari-Vassouras Potash Mine to the south.

+ These targets have not been drill tested +the Company is currently planning the drilling of two holes to a depth of 350m to test these targets. ...

www.triumphtin.com.au/pdfs/AcquisitionOfBrazilianPotashProje…

Viele Firmen gibt es da ja noch nicht-wenn inzwischen auch schon ein paar-, aber sowas hier sind denk ich welche die man, bei entsprechendem Interesse, in dem Zusammenhang im Blick behalten kann.

Triumph Tin - Acquisition of Brazilian Potash Project - Aug 28, 2014

+ The Company has acquired a 100% interest in the Capela Potash Project, in the Sergipe Alagoas Basin on the east coast of Brazil.

+ The Sergipe-Alagoas Basin hosts significant deposits of sylvinite +carnallitite, associated with evaporitic sub basins.

+ Vale operates the Taquari-Vassouras Potash Mine, which is the only Potash mine currently operating in Brazil, 13km to the south of the Capela Potash Project.

+ Recently completed 3D seismic has confirmed the presence of potential salt layers @relatively shallow depth, within the Capela Potash Project area.

+ The 3D seismic has also confirmed that the Capela Potash Project is the possible northern extension to Vales Taquari-Vassouras Potash Mine to the south.

+ These targets have not been drill tested +the Company is currently planning the drilling of two holes to a depth of 350m to test these targets. ...

www.triumphtin.com.au/pdfs/AcquisitionOfBrazilianPotashProje…

Antwort auf Beitrag Nr.: 47.628.057 von likeshares am 27.08.14 22:16:27

Wie ich es gesagt hatte -etwas zeitversetzt dürfte das, ein deutlicher Anstieg, so einiges Angebot, wieder, zurück ins Spiel bringen.

Aber, für den beabsichtigten Zweck, hat Stupidgame da ja weiteren Treffer gelandet.

Gruß

P.

Wie ich es gesagt hatte -etwas zeitversetzt dürfte das, ein deutlicher Anstieg, so einiges Angebot, wieder, zurück ins Spiel bringen.

Aber, für den beabsichtigten Zweck, hat Stupidgame da ja weiteren Treffer gelandet.

Gruß

P.

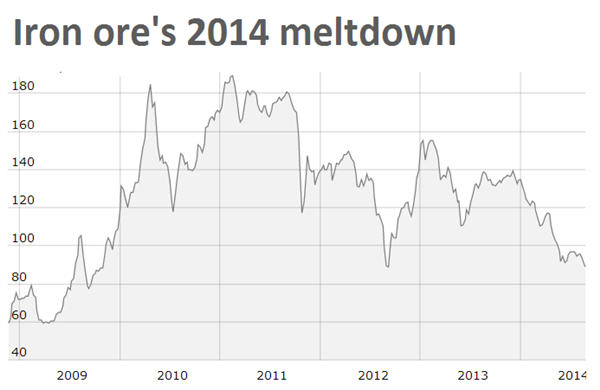

Largest iron ore miners smashing Chinese competitors, There’s a death match among iron ore producers, with the big Australian miners +Brazil's Vale increasing pressure on their high-cost Chinese rivals

www.mining.com/largest-iron-ore-miners-smashing-chinese-comp…

"It may sound odd, but there are a few iron ore producers quite happy with the slump in the commodity price. They are the market’s “big three “ —Rio Tinto (ASX:RIO), BHP Billiton (ASX:BHP) and Vale (NYSE:VALE)— whose vast low-cost mines are driving Chinese higher-cot rivals out of the market.

According to a recent research report by Australian analyst Michael Komesaroff (subs. required), the triumvirate of global iron ore miners have kept supply growth at full tilt even as demand decelerates.

“As long as this state of affairs continues, the ore price will stay below the level dictated by cost-curve fundamentals: probably in the US$95-US$100 per tonne range,” he writes in the paper published by the global research powerhouse Gavekal’s China-based arm Gavekal Dragonomics.

the drop in prices has nothing to do with a lack of demand, but with the fact that Rio Tinto, BHP and Vale continue to ramp supply up.

Komesaroff notes the drop in prices has nothing to do with a lack of demand, but with the fact that Rio Tinto, BHP and Vale continue to ramp supply up. In fact, Australian annual output is now 150 million tonnes, higher than in 2011.

The problem for Chinese producers, which feed 35% of the local demand, is that their ore is lower grade than the foreign imports. At the same time, their production costs are at the upper end of the big three.

The analyst believes the situation is not sustainable for much longer and that once high-cost Chinese miners are driven out of the market, iron ore prices will rise back to around $110.

Collateral damage

Mid-cap Australian iron ore miners will also fall victim of this fight to the death, as the ore price is beginning to reach levels where they will struggle to break even.

According to UBS estimates, published by The Sydney Morning Herald, Australian miners Grange Resources (ASX:GRR) and Gindalbie Metals (ASX:GBG) are facing uneconomic production, with break-even prices of $87 a tonne and $98 a tonne respectively.

Atlas Iron (ASX:AGO) and Arrium (ASX:ARI) are next in the firing line with cash costs over $80 a tonne.

No one is predicting a move back to the early days of the iron ore trade when the price, set during secretive annual contract negotiations, never strayed from $10 a tonne for more than 20 years.

But it is worth noting that back in 2007 the commodity was still trading at $36 a tonne.

And the all time high of $192 in February 2011 now seems like nothing more than an aberration.

"

"

www.mining.com/largest-iron-ore-miners-smashing-chinese-comp…

"It may sound odd, but there are a few iron ore producers quite happy with the slump in the commodity price. They are the market’s “big three “ —Rio Tinto (ASX:RIO), BHP Billiton (ASX:BHP) and Vale (NYSE:VALE)— whose vast low-cost mines are driving Chinese higher-cot rivals out of the market.

According to a recent research report by Australian analyst Michael Komesaroff (subs. required), the triumvirate of global iron ore miners have kept supply growth at full tilt even as demand decelerates.

“As long as this state of affairs continues, the ore price will stay below the level dictated by cost-curve fundamentals: probably in the US$95-US$100 per tonne range,” he writes in the paper published by the global research powerhouse Gavekal’s China-based arm Gavekal Dragonomics.

the drop in prices has nothing to do with a lack of demand, but with the fact that Rio Tinto, BHP and Vale continue to ramp supply up.

Komesaroff notes the drop in prices has nothing to do with a lack of demand, but with the fact that Rio Tinto, BHP and Vale continue to ramp supply up. In fact, Australian annual output is now 150 million tonnes, higher than in 2011.

The problem for Chinese producers, which feed 35% of the local demand, is that their ore is lower grade than the foreign imports. At the same time, their production costs are at the upper end of the big three.

The analyst believes the situation is not sustainable for much longer and that once high-cost Chinese miners are driven out of the market, iron ore prices will rise back to around $110.

Collateral damage

Mid-cap Australian iron ore miners will also fall victim of this fight to the death, as the ore price is beginning to reach levels where they will struggle to break even.

According to UBS estimates, published by The Sydney Morning Herald, Australian miners Grange Resources (ASX:GRR) and Gindalbie Metals (ASX:GBG) are facing uneconomic production, with break-even prices of $87 a tonne and $98 a tonne respectively.

Atlas Iron (ASX:AGO) and Arrium (ASX:ARI) are next in the firing line with cash costs over $80 a tonne.

No one is predicting a move back to the early days of the iron ore trade when the price, set during secretive annual contract negotiations, never strayed from $10 a tonne for more than 20 years.

But it is worth noting that back in 2007 the commodity was still trading at $36 a tonne.

And the all time high of $192 in February 2011 now seems like nothing more than an aberration.

"

Ethanol REX American Resources

gestrige Zahlen:

Second Quarter Diluted EPS Rise 277% to a Record $2.68

Second Quarter Gross Profit More than Triples to $38.8 Million Leading to a 276% Increase In Net Income Attributable to REX Common Shareholders of $21.9 Million

Diluted EPS for the Six Months Ended July 31, 2014 Rise to $5.35

http://finance.yahoo.com/news/rex-american-resources-second-…

gestrige Zahlen:

Second Quarter Diluted EPS Rise 277% to a Record $2.68

Second Quarter Gross Profit More than Triples to $38.8 Million Leading to a 276% Increase In Net Income Attributable to REX Common Shareholders of $21.9 Million

Diluted EPS for the Six Months Ended July 31, 2014 Rise to $5.35

http://finance.yahoo.com/news/rex-american-resources-second-…

Wie beim letzten Mal schon gepostet, für mich gibt es keinen Grund für die EZB mehr für weitere Lockerungen.

Das Geldmengenwachstum M3 hat den Boden gesehen.

Um 10:00 Uhr gemeldet:

M3 Eurozone +1,8% (erwartet +1,5% / Vormonat raufkorrigiert auf +1,6%)

Private Kredite fallen allerdings noch

-1,6% (erwartet -1,5% / Vormonat runterkorrigiert auf -1,8%)

Die Vererrungen nach unten durch die derzeit fallenden Agrarpreise und Energiepreise darf man eh nicht berücksichtigen. Das machen die ZBankler auf dem Weg nach oben sonst auch nicht. Die Kernraten sind aktuell höher.

Das Geldmengenwachstum M3 hat den Boden gesehen.

Um 10:00 Uhr gemeldet:

M3 Eurozone +1,8% (erwartet +1,5% / Vormonat raufkorrigiert auf +1,6%)

Private Kredite fallen allerdings noch

-1,6% (erwartet -1,5% / Vormonat runterkorrigiert auf -1,8%)

Die Vererrungen nach unten durch die derzeit fallenden Agrarpreise und Energiepreise darf man eh nicht berücksichtigen. Das machen die ZBankler auf dem Weg nach oben sonst auch nicht. Die Kernraten sind aktuell höher.

Trading Spotlight

Antwort auf Beitrag Nr.: 47.628.057 von likeshares am 27.08.14 22:16:27Panoramic hat heute annehmbare Q2-Ergebnisse gemeldet. Würde man den Q-Gewinn annualisieren, dann käme man auf schon wieder ein nur moderates KGV. Der Ni-Durchschnittspreis in Q3 ist bislang noch etwas höher. D.h. das laufende Quartal könnte noch besser werden.

Hier muss man sich im wesentlichen die geplante Capex anschauen. Die könnte den Weg des Aktienkurses beeinflussen, wenn das Unternehmen in kurzer Frist zu hohe Investitionen tätigt, und dabei Cashflow und Cashbestand überstrapaziert.

Ansonsten könnte man von der Bewertung her hier schon die Nickelstory etwas mitspielen. Die Aktie ist aber schon ganz nett gelaufen, war aber zuletzt etwas in Konso-Modus.

Hier muss man sich im wesentlichen die geplante Capex anschauen. Die könnte den Weg des Aktienkurses beeinflussen, wenn das Unternehmen in kurzer Frist zu hohe Investitionen tätigt, und dabei Cashflow und Cashbestand überstrapaziert.

Ansonsten könnte man von der Bewertung her hier schon die Nickelstory etwas mitspielen. Die Aktie ist aber schon ganz nett gelaufen, war aber zuletzt etwas in Konso-Modus.

Antwort auf Beitrag Nr.: 47.627.325 von donnerpower am 27.08.14 21:04:54ok, das ist schwerere Kost... die muss ich mir mal am WE genauer ansehen dann !

Antwort auf Beitrag Nr.: 47.628.330 von XIO am 27.08.14 22:43:10nö überhaupt nicht. seit jahresanfang haben wir eine hausse nach wie vor.

mein depot ist seit jahreswechsel mit dem geilen heutigen tag genau 35% gestiegen.

hab 65 werte im depot zu 85% rohstoffaktien.

...eben eine versteckte hausse ...und das sind die besten und stabilsten. keiner redet drüber aber sie ist da

...und das sind die besten und stabilsten. keiner redet drüber aber sie ist da

mein depot ist seit jahreswechsel mit dem geilen heutigen tag genau 35% gestiegen.

hab 65 werte im depot zu 85% rohstoffaktien.

...eben eine versteckte hausse

...und das sind die besten und stabilsten. keiner redet drüber aber sie ist da

...und das sind die besten und stabilsten. keiner redet drüber aber sie ist da

Antwort auf Beitrag Nr.: 47.628.057 von likeshares am 27.08.14 22:16:27Außer Nickel nichts gewesen

Die Rohstoff-Rally ist gescheitert

http://www.teleboerse.de/rohstoffe/Die-Rohstoff-Rally-ist-ge…

Die Rohstoff-Rally ist gescheitert

http://www.teleboerse.de/rohstoffe/Die-Rohstoff-Rally-ist-ge…

Die Nickelstory läuft erwartungsgemäß weiter, nun unterstützt von mehreren Analysten großer Häuser...

http://www.bloomberg.com/news/2014-08-12/nickel-s-56-rally-s…

http://www.bloomberg.com/news/2014-08-12/nickel-s-56-rally-s…